First published March 25, 2022. Updated June 16, 2022.

In this article, Indonesian venture capitalist William Gozali, whose career began when GoTo were still two up-and-coming startups, shares his views on the ecosystem’s rise, what the next chapter will be, and the implications for new companies and more money coming in.

William Gozali is the Head of Indonesia at Insignia Ventures Partners (IVP). Prior to joining Insignia, William was a founding member of two Indonesian corporate venture capital firms, MDI Ventures (by Telkom Indonesia, 2015), and BRI Ventures (by BRI Group, 2019). Working together with Indonesia’s largest telco and largest bank gave him deep knowledge and understanding on how to crack the Indonesian market.

Highlights

- This wave of Indonesian unicorns or decacorns heading to the public markets are certainly massive in their own right, but there are unique needs that the existing, so-called “first generation” tech juggernauts have been unable to fulfill.

- The path to scale isn’t solely dependent on the size of one’s war chest (though it helps to have that in play), but also the “hills” companies choose to make their stand.

- Existing market leaders have also inevitably highlighted the “gaps” they have either been unable to tap or missed entirely…opening the gates for younger companies to take what we’ll call a “counter-position” strategy, effectively doing things differently compared to the market leaders.

A housewife in Surabaya who, in the midst of the pandemic, decided to become an agent for an emerging social commerce platform called Super to supplement her husband’s income and become a “micro-distributor” of essential FMCGs for her community…

A warung owner in a faraway rice field in Mengwi, Bali who four years ago around 2017 learned about this fintech app called Payfazz and became a “digital bank” in their local community, enabling people to access financial services…

A basic food and FMCG wholesaler in Bogor who nearly went bankrupt back in 2014 but later joined the AwanTunai ecosystem and availed of the company’s digitization offerings, improving his inventory management, account receivables system, and usage of online ordering, which all contributed to revenues crossing US$1.5M in September and October 2021…

In the world of startups and venture capital, we often talk about the massive market potential in Indonesia. But it is in these stories of impact on communities across various parts of Indonesia that it becomes clear just how much opportunity there is in the country for digitalization.

When it comes to Indonesia, the more you think you’ve grown, the less you’ve actually captured

Indonesia’s startup ecosystem is writing a new chapter. After much anticipation from the ecosystem and amidst the economic uncertainties, Go-To officially announced its plans to go public on the Indonesia Stock Exchange (IDX) on April 4th, aiming to raise at least USD1.1 billion through the IPO. Its target raise, the nature of the business as a venture-backed tech company, and its role in driving Indonesia’s digital economy make it one of the most significant IPOs to be conducted in the country.

A decade ago, both Tokopedia and Bukalapak, which went public in 2021, were young startups. Back then I was a venture capitalist just beginning my career, and we were in the early days of the ecosystem, with the local corporate venture just beginning to trickle in and most VCs coming from Japan at the time. A combination of capital and user influx over the next ten years propelled these local players to not only become billion-dollar companies but also transition into the public markets (Bukalapak having done so the previous year).

This wave of Indonesian unicorns or decacorns heading to the public markets are certainly massive in their own right, already reaching millions of people and catering to entire ecosystems of needs. But going back to the stories earlier it’s clear that we are just at the tip of the iceberg when it comes to the full potential of Indonesia’s digital economy. From Surabaya to Bogor to Bali, there are unique needs that the existing, so-called “first generation” tech juggernauts have been unable to fulfill.

Perhaps it’s not a competitive landscape where the winner-takes-all, but the winner-takes-some or “the winner takes what they are good at and then some”. We saw this in China with Pinduoduo when the social commerce company went up against Alibaba in the public markets, and both companies have since thus coexisted.

Even amongst the “first generation” giants, there are some competitive advantages that carve out the market in a way that prevents any single company from fully dominating. Bukalapak for example has its specialty working with mitras in rural Indonesia, while Tokopedia is able to leverage synergies with Gojek’s massive distribution, and Shopee has the full force of Sea Group behind it. Companies can try to do everything, but it is unlikely that they will be the best at everything.

If that’s the case, then the path to scale isn’t solely dependent on the size of one’s war chest (though it helps to have that in play), but also the “hills” companies choose to make their stand.

The Counter-Position Strategy: Why compete when you can change the game?

While Indonesia arguably already has “top-of-mind” brand winners in broad mature categories like GoTo, Grab, and Sea dominating the consumer superapp race or Bukalapak, Tokopedia, and Shopee dominating ecommerce, the very emergence of these market leaders has opened up the playing field in terms of categories or market segments. Initially these companies scaled on top of tier-1 cities like Jakarta with high-tech adoption, but in the past five years we’ve seen rapidly increasing adoption beyond these low-hanging fruit segments, like tier-2 and tier-3 cities and rural areas in Indonesia.

In growing to such behemoths, these market leaders have also inevitably highlighted the “gaps” they have either been unable to tap or missed entirely. The floodgates have opened for these companies to take what we’ll call a “counter-position” strategy, effectively doing things differently compared to the market leaders, like tackling a different market segment or different region.

This has become increasingly attractive to regional and global investors because having seen the success of the venture-backed scale with the likes of GoTo and Bukalapak, they’re now scratching their heads thinking, “Where else in Indonesia can we fuel this kind of growth?”

And clearly there are more green pastures that abound, with the “counter-position” strategy manifesting in various ways. The existing competition has forced new players to be creative and compete not on capital or funding intensity only, and some of these moats frequent readers of Insignia Business Review may be familiar with already:

- The Network Counter-Position: Payfazz, with its financial services platform, achieved a competitive advantage in rural Indonesia not just being an early mover but building strong distribution in its agent network.

- The Vertical Counter-Position: Social commerce company Super focused on growing their hyperlocal supply chain (group buying + micro-fulfillment) in East Java, where its founders are from, and focused on FMCG goods, carving out leadership in these areas and using the momentum in these areas to expand further.

- The Value Chain Counter-Position: AwanTunai targeting the lack of digitization in downstream FMCG supply chain (wholesaler + SME) operations to develop innovative financing for retailers, which created a defensible ecosystem which they strengthened by providing software solutions to tackle other pain points beyond financing (e.g. SKU management, online ordering).

- The Geographic Counter-Position: Bakool tackles the lack of egrocery providers in rural Indonesia by providing fresh produce group buying services for tier 2 cities in the country. The startup’s focus on building quick commerce operations outside the Jabodetabek area (the urban areas in and around Jakarta) has allowed them not only to carve out a sspace in the market but also focus on improving household productivity in the country.

The first principle behind the counter-position strategy is to shift the battlefield and build on that focus. The implication of this long-term is that we can expect to see more “category winners” and “regional winners” as more players carve out their niche. Ultimately, the competitive advantage the first generation of tech giants established by size has sparked new opportunities which is a sign of a healthy market overall.

What we’ve learned about executing the “Counter-Position” Strategy (so far)

As an Indonesian venture capitalist seeing these developments in Southeast Asia, now that it’s clear a new wave of startups are coming into the picture and adding new layers to the country’s digital economy, the question is, “how are these companies able to develop effective counter-position strategies?”

From the founders and companies I’ve had the privilege of working with thus far, there are four general approaches I’ve seen (and I include some examples as well):

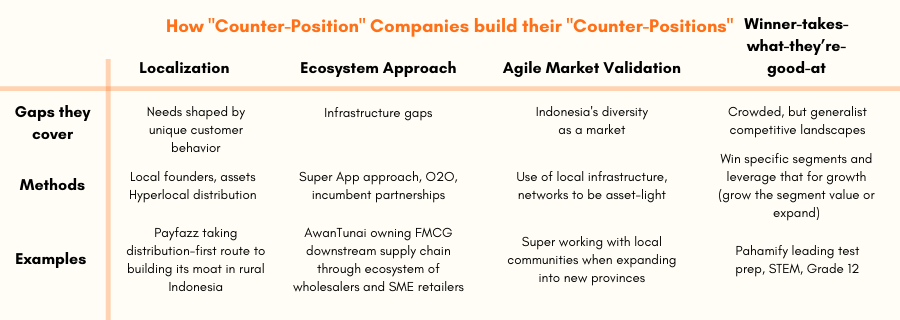

- Localization: We are often compared to other countries in a quantifiable way, e.g. the “we are a [insert number here] years behind China” is an all-too-familiar example, but when it comes to customer behavior, it is much harder to draw lines between similarities and differences that will ultimately define the how exactly a startup will “counter the position” of established players.

- Payfazz understood this and built their agent network / distribution first before expanding their product.

- Flip built its money transfer platform on top of the initial pain point that Indonesia uniquely has, a 6500 rupiah bank transfer fee (worth a bowl of noodles).

- Ecosystem Approach: Infrastructure gaps are a hallmark of an emerging market like Indonesia, and so it can be valuable to be the company that owns the distribution and partnerships that fill in these gaps, be it through O2O presence, networks, etc. And so even as there are “top of mind” super apps in the country already, we can expect more vertical-specific or localized “super apps” where the companies own the distribution and flywheel of their target segment.

- AwanTunai is building this through their financing-first ecosystem of services catering primarily to the downstream FMCG supply chain. To do this they’ve had to build O2O products (POS products) and build partnerships with financial institutions.

- Agile Market Validation: If you go on the ground, you will quickly realize Indonesia is more than just a single homogenous market. Indonesia has many faces, and we’ve seen how critical it is to be agile with market validation before scaling or expanding to a more uncharted territory.

- Super works with local communities and infrastructure to rapidly scale its hyperlocal supply chain and reach more cities across Eastern Indonesia. Their VP of Operations Garret Jeremy Koeswandi shares examples of moving into new provinces with culturally unique demographics on our podcast.

- Winner-takes-what-they’re-good-at: We’ve mentioned this before, but it bears repeating — focus is important especially in a broad market with a lot of leaders. That said, the idea is not to settle for the niche, but to leverage it as a launchpad for growth.

- Pahamify has carved out its niche with its market leadership in test prep, especially for Grade 12 students, and STEM-focused content.

- As a logistics technology platform, Ritase focuses on building scalable Transport Management Software solutions for enterprise and MNC brands, while driving up the value of these solutions through the other end of its platform offering digital solutions for truckers as well.

- In the sea of SaaS and marketplace solutions for SMEs, Credibook leveraged its go-to-market of digital bookkeeping to eventually uncover the massive opportunity in digitizing wholesaler operations and financial management, building the Faire of Indonesia through Credimart.

These approaches are not mutually exclusive, nor are they be-all, end-all of a counter-position strategy and standing out in a growing sea of startups. They’ve proven their worth for many startups on the rise and can be used to kickstart and guide growth.

Change is constant

With these counter-position companies coming into the funding spotlight, Indonesia’s public markets entering a moment of truth with these venture-backed tech companies, shifts in capital and talent distribution in the country being shifted further by the movement of the political capital, there’s a lot to be excited about for Indonesia’s startup and venture capital ecosystem.

And more importantly, there’s a lot more room for founders and investors to push the envelope of Indonesia’s digital economy. There may be dominant players and market leaders, but the very nature of a startup’s existence and technology’s rapid development demands the constant emergence of opportunity for the new and the innovative.

William Gozali is the Head of Indonesia at Insignia Ventures Partners (IVP). Prior to joining Insignia, William was a founding member of two Indonesian corporate venture capital firms, MDI Ventures (by Telkom Indonesia, 2015), and BRI Ventures (by BRI Group, 2019). Working together with Indonesia’s largest telco and largest bank gave him deep knowledge and understanding on how to crack the Indonesian market.