2020 has been a year of greater awareness around health, and over the past year, we saw not only increased demand for online health services — like mental health company Intellect, whose CEO we talked to the previous week — but also insurance products as well. However, even with this interest in insurance products, buying insurance still remains a difficult and even painful experience in emerging markets like Indonesia, where only 2% of the population is covered.

So in this episode, we rang up Giacomo Ficari, CEO and co-founder of Lifepal, Indonesia’s leading marketplace for insurance. They closed one of the biggest rounds for insurtech in Indonesia and since January last year have been growing 30-40% every month. Giacomo shares with us how they’ve been leveraging the online-to-offline, PolicyBazaar insurance distribution model (PolicyBazaar plans to IPO this 2021) for Indonesia to be a “reliable friend” for consumers looking for insurance.

To host this episode my colleague and principal Samir Chaibi is back again. For our listeners, you may remember him from our calls with the CEOs of Indonesian wealth management platform Ajaib and Philippine digital bank tonik.

Takeaways

Takeaways from our conversation with Lifepal CEO and co-founder Giacomo Ficari

(1) “[COVID] has accelerated awareness among consumers around health risks and the importance of being protected with insurance…Lots of demand has shifted online and that’s where Lifepal is…In my view, this shift will be permanent. and it will remain after COVID.”

(2) “We noticed that when you go a little bit higher in income, so we are really talking about the middle class up, people want better alternatives…So I think the PGS is great, but it’s going to stay definitely for the low income.”

(3) “I like to see companies not by the year when they have been funded, but I like to see them age by how many tests they can run per year. And that’s really the power of a startup.”

(4) “We really aim for the long-term to become the number one shopping destination for insurances and the most trusted brand about insurance in Indonesia.”

(5) “Don’t throw people to problems, but develop solutions that are scalable with software…it’s been really a year where headcount has been flat but we [were] growing tremendously just with technology and product.”

(6) “We saw that your role as a leader, but also as an individual contributor in a fast-growing startup will change roughly every six months. And it’s really important to accept this change.”

(7) “Hypergrowth is not for everyone…I started hiring by “fast-growing startup fit”. And if a person has been part of a startup that grew like 3-5x a year this person probably is comfortable with hypergrowth and thinks that it is even normal. Otherwise, it can be painful for many people, this journey.”

Timestamps (Responses)

00:44 Samir introduces Giacomo;

02:11 Traditional insurance journey for Indonesians;

05:17 Three models of disruption in insurance distribution;

09:07 Cracking the O2O, PolicyBazaar model in Indonesia;

11:31 Impact of COVID19 on insurance industry;

12:42 Relationship of Indonesians with universal public insurance;

13:36 Lifepal’s 3 principles;

15:05 Applying Lifepal’s 3 principles amidst fast growth;

16:11 Lifepal in 2025;

17:28 Rapid-fire Round: Takeaways from YC, Lazada, and leading Lifepal

Transcript

Samir: Pleasure to be back to discuss insurtech with our guest today. So insurtech is indeed a really exciting space, precisely because of the opportunity to solve the inefficiencies of traditional offline distribution, especially in emerging markets like Indonesia.

And so today we are on call with Giacomo Ficari, who is the CEO and co-founder of a company doing just that. It’s Lifepal and it’s Indonesia’s leading insurance marketplace. Before we get started with Giacomo, I just want to speak a little bit about Lifepal’s growth and how Insignia met with Giacomo. So Giacomo was previously co-founder of Aspire, which is a Southeast Asia SME challenger neobank, and also an Insignia portfolio company. Prior to venturing into FinTech he has built leadership experience in Asia’s e-commerce space with companies like Lazada, leading up Lazada Malaysia, and Groupon, where he was the CEO of Japan and Malaysia. He’s also a Y Combinator and Rocket Internet alumni. Thanks Giacomo for coming On Call with Insignia today. Since we just started 2021, a new year, a new decade. Did you come up with any New Year’s resolution?

Giacomo: Yes I do! Make sure that more people are protected in Indonesia and our tagline is really “protect everyone”.

Samir: Perfect! Since this is our first episode on insurtech, I’d just like for you to paint a picture for our listeners of what the industry is like in Indonesia.

What is the insurance customer journey currently like for Indonesians? What opportunities did you see in the market that motivated you and your co-founders to start Lifepal in 2019, after co-founding and leading Lazada?

Giacomo: Yeah. So when we approached insurance, we thought that today in Indonesia, insurance is largely solved by traditional offline agents. And they have created mistrust over the years and definitely due to a push approach but also for the lack of transparency of information. Not always the agents are really well-trained on the details that matter a lot in insurance.

Also, they give limited choices to customers. In fact in Indonesia, agents can sell only one brand. So the customer, they talk to the agent can only have that brand. And lastly, we saw a really strong lack of convenience when buying and when you use the insurance. For example, there’s a lot of paperwork, long approval processes and periods, and there’s no easy way to do claims.

So it’s really not a surprise to us that agents were pretty hated in Indonesia and they are clearly no longer capable of helping a more educated, younger, and digital consumer. Starting from that point, then we start thinking about how we should analyze the market, right, and what are the opportunities that we see?

So after a few years, there are a few questions that we ask ourselves. And the first one was how big is the impact that this can generate on people’s lives? And we saw that as a function of our impact is equal to the number of people that we can help. And the importance that these, the insurance in this case, has for each person.

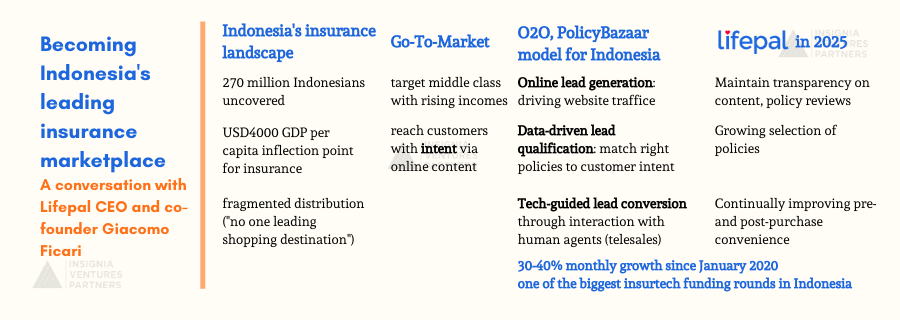

So we realized that in Indonesia, there are 270 million people that are not covered, only like 2%. A supermassive number of people that we can help. And then we realized that actually insurance is really important in people’s lives. It matters a lot for each individual. In fact, buying an insurance plan is one of the most delicate financial decisions that a person can take for himself and for the family and will impact many years to come.

So it was really a magical realization. We can really impact a lot of people. Then we ask ourselves, is it the right timing to fix this problem? Maybe it’s too early or maybe it’s way too late. And the answer was really, yes, it’s the right timing. And the insurance market is that we really see that it’s at an inflection point and we feel it on the ground.

Usually, GDP per capita is the more, simple kind of data point. Lots of papers say that the inflection point arrived at USD4,000 GDP per capita per year. From our experience, maybe slightly higher but it’s definitely the right moment for Indonesia. In fact, the majority of the income for top tiers, one and two cities in Indonesia is way above that.

And we do really see it in the ground. And the last question or box that we wanted to tick is, is someone else doing this or has already solved this problem? And then we realized that actually there is not really one leading shopping destination for insurance and customers still don’t have a good experience and a good alternative.

So we really decided to be the biggest online marketplace for insurance and fix the problem for the customer. As you know, our founding team is coming from Lazada and then we saw that the same digital revolution that we experienced back in 2012 with Lazada is actually happening really similarly to insurance. So for us, it was quite obvious that this is a big problem, it’s the right time. And we saw the same evolution to e-commerce to insurance.

“So we realized that in Indonesia, there are 270 million people that are not covered, only like 2% [are covered]. A supermassive number of people that we can help…And the insurance market is that we really see that it’s at an inflection point and we feel it on the ground…And then we realized that actually there is not really one leading shopping destination for insurance and customers still don’t have a good experience and a good alternative.”

Samir: Got it. Just to continue painting a better picture for our listeners about insurtech in Indonesia, how would you describe the insurtech landscape like in Indonesia vis-a-vis other markets in Southeast Asia, or India and China? And from the perspective of the insurtechs, are there any unique challenges to establish distribution and drive adoption in a country like Indonesia?

Giacomo: So we saw that in distribution, we look a lot at India actually, and we saw fundamentally three business models. The first one is the ZhongAn model actually from China. So micro insurances embedded inside a line checkout or a third party, external platform. That’s the usual travel insurance that you buy or you tick when you buy a flight ticket.

Then we saw there was another model. We call it the Turtlemint model from India. This model helps traditional offline agents to sell better faster. This model doesn’t focus on the customer but focuses more on the agents. So it’s kind of like a backend system and software for agents.

And lastly, we saw the PolicyBazaar model from India also. And this model is about to be the number one, shopping destination for insurance, but also the number one brand. So it’s kind of like a D2C of fintech, or D2C for insurance, if you like. And this is really a direct to consumer model that is changing how insurance policies are purchased and offer it in an alternative way to the traditional offline agents.

Besides that, we also saw that not only consumers benefit from this, but also insurance carriers, they see online distribution as an incremental channel and not really a cannibalization model that attacks the traditional agents. So we really saw that PolicyBazaar was the winning model for consumers and for the industry and that’s something that we decided to go for.

“So we really saw that PolicyBazaar was the winning model for consumers and for the industry and that’s something that we decided to go for.”

And going to your second question, what are the challenges? The first one was we needed to get clarity on which is the right target audience. And the second was once you got the clarity, what is the best way to reach the target audience?

So on the first point, it was not really obvious for us initially to understand who to target. Of course, we wanted to help everyone so we were targeting the entire population especially the lower-income, right? We thought those are the people who need more help.

But soon we learned that selling insurance to meet the low income is definitely a noble action but it’s really arduous and inefficient simply because those people don’t really have enough income to even cover the daily expenses. So definitely they’re not gonna have savings for insurance. And then we actually learned that the right target audience is really the rising middle class. They have a minimum level of saving and education and they can really allocate a little bit of those savings to insurance. There’s a lot of papers saying that as we said before, this is 4,000 GDP per capita per year inflection point for insurance.

In Indonesia, the middle class is growing rapidly. And in tier one and tier two cities, the income has already surpassed the inflection point. So getting this clarity was not easy. But we got that after a few months.

“We actually learned that the right target audience is really the rising middle class. They have a minimum level of saving and education and they can really allocate a little bit of those savings to insurance…In Indonesia, the middle class is growing rapidly.”

The second challenge was how do we reach this target audience? That is a little bit more narrow and we definitely didn’t want to use the old pushy method of traditional insurance that really has failed customers in the past. And we understood that people that have searched for insurance or personal finance topics and advisors specifically online have already a pre-intent to buy insurance.

So it’s more like there’s already an initiation. So we started to create online content about insurance, personal finance, that addresses the needs of customers. We call it a top of the funnel approach and it has been working really well for us in these 18 months of operation. In fact, today we are the biggest online marketplace by traffic with 3.5 million visitors every month rapidly we combined one million social media followers and this today generates actually a really big portion of our business and it’s purely organic. So it’s great to see that we found the right audience and we are building something that customers actually want.

“We understood that people that have searched for insurance or personal finance topics and advisors specifically online have already a pre-intent to buy insurance…So we started to create online content about insurance, personal finance, that addresses the needs of customers.”

Samir: Just to go back on what you just said, right about building that differentiated business model, I’m curious about the thought that was put behind building that PolicyBazaar model, approaching it from an online to offline model.

And we actually wrote about this ourselves on our business review at Insignia, but I’m curious about what was the thought process here and how did you build that really strong brand combined with telesales operations and at the end of the day, now that you’re trying to crack that insurance disruption model, how does Lifepal’s model compare to other players in Indonesia?

Giacomo: So we started approaching the insurance distribution with two components. The first one was lead generation and then lead conversion. And the question we ask ourselves is what should be done by technology and digital marketing and what should be done by humans, the insurance agents?

And we realized that the lead generation should be done online. Because in this way, leads have a clear intent to buy insurance. They are applying, they are looking for help and this causes, of course, a higher conversion rate from a business perspective, but also a better customer experience. We don’t need to be pushy and aggressive like traditional agents. So lead generation definitely should be done online.

And the second was lead conversion. So we realized that these parts require human interaction mainly because insurance policies are quite expensive and they can be complicated as well but we also realize that if we cannot leave it to humans completely, we actually need to enhance them with technology. So we have been focusing a lot on the software that helps agents to sell better and make them super agents like they would like to call it. So today it becomes really easy for an agent to work with us and deliver a good customer experience and also make the targets and convert.

“We realized that the lead generation should be done online. Because in this way, leads have a clear intent to buy insurance…[Meanwhile lead conversion] requires human interaction mainly because insurance policies are quite expensive and they can be complicated as well but…we cannot leave it to humans completely, we actually need to enhance them with technology.”

Samir: Seems like it’s really about qualification, right, really making sure that the intent is there, really making sure that there is the ability to buy and really making sure that whatever product you’re selling actually feeds into the requirement and the pain that the client is experiencing, which is not what most offline agents are used to doing. It’s all about selling. It’s all about shoving product down the throat of their clients, right? And this is why this industry has always been seen as a push industry, as opposed to a pull one.

Giacomo: Correct. So we really need to build up a pull business in a push industry. And lead qualification as you said is really important. What this means is given that we have so much traffic and data on the website, we can actually start collecting those data and really profile and qualify the leads and understand what is the right offer that we should propose to the customer.

And this is what an agent would propose to the customer. Like it’s not really random when an agent will call you and we offer two or three products. It’s really filtered by the data analysis and qualification, and this is something insurance has never done because of course, they don’t have massive traffic on their website.

They don’t have maybe the DNA to really analyze those data. And haven’t really met the demand and supply. We found this really powerful and believe in this more lead qualification with data and pull approach.

“Lead qualification as you said is really important. What this means is given that we have so much traffic and data on the website, we can actually start collecting those data and really profile and qualify the leads and understand what is the right offer that we should propose to the customer.”

Samir: Let’s switch gears a little bit. Let’s talk about what happened last year in 2020. Obviously, there’s been really interesting trends and shifts from both providers and customers because of COVID. Tell us a little bit about what you’ve seen.

Giacomo: Yeah, for us last year was really important. We learned a lot. There’s a lot of things that happen, but the biggest event was definitely COVID. It has accelerated awareness among consumers around health risks and the importance of being protected with insurance. Also given it is much harder for customers to meet traditional agents face-to-face. Lots of demand has shifted online and that’s where Lifepal is.

So we have been really lucky about this shift and in fact, our website has increased rapidly. We went to 3 million organic visitors every month and 1 million social media followers. And our net premium has been growing 30-40% consistently every month since January. In my view, this shift will be permanent. and it will remain after COVID so this awareness and the probably less face to face meeting. So we’ve been definitely lucky on that.

“[COVID] has accelerated awareness among consumers around health risks and the importance of being protected with insurance…Lots of demand has shifted online and that’s where Lifepal is…In my view, this shift will be permanent. and it will remain after COVID.”

Samir: And you’ve been positively impacted by COVID. And I guess talking a little bit about health coverage in the middle of the crisis when it comes to Indonesia, right? The majority of the population by now is kind of covered by the universal public insurance, the PGS. How do Indonesians think about health coverage in that context? Do they actually seek the higher and better coverage on top of this? What’s their relationship to health insurance?

Giacomo: Yeah, we iterated a lot on this topic. And what we concluded was that I would say the bottom of the pyramid, so kind of the low income, they will definitely use the PGS and it’s pretty decent coverage. It’s kind of a full — there is no limitation on it, covers pretty well. Maybe their operations and the customer experience is not great like the long waiting period, but for people that really are low income, that’s a pretty good solution that the government is offering.

We noticed that when you go a little bit higher in income, so we are really talking about the middle class up, people want better alternatives, and this could be through a company offering health insurance or even people they want to have really extensive coverage for them and their family. So I think the PGS is great, but it’s going to stay definitely for the low income.

“We noticed that when you go a little bit higher in income, so we are really talking about the middle class up, people want better alternatives…So I think the PGS is great, but it’s going to stay definitely for the low income.”

Samir: Got it. That’s a very helpful context. Let’s look at what’s happening under the hood. I think our listeners would be very interested to know about the company culture and so how would you describe what’s happening in Lifepal internally and how does it reflect in your brand and customer experience?

Giacomo: We have three major business principles that shape our culture and that’s what we are focused on. The first one is speed. Then there’s ownership and then there’s simplicity. We are really obsessed with speed so we are always forcing ourselves to test and learn as much as possible and keep the learning cycle as short as possible. I like to see companies not by the year when they have been funded, but I like to see them age by how many tests they can run per year. And that’s really the power of a startup.

The other principle is ownership. And we don’t say this is not my job, this is another department’s job, he’s not my accountability. We just get it done if it helps the customer.

And the last one is something really dear to me is the simplicity. I always say simplicity makes us effective. And this can be applied to ops processes to the customer journey customer experience on the app, even to the analysis and reporting that we do. Because this is not really an easy topic. If it’s really hard to understand no one can really use it and therefore is not effective. So really these three things speed ownership and simplicity.

“I like to see companies not by the year when they have been funded, but I like to see them age by how many tests they can run per year. And that’s really the power of a startup.”

Samir: This is a really powerful set of ideas especially for a company that is building its playbook, as it goes in the country where nobody has done it before. I’m curious if you could tell us maybe one or two stories that emerge from applying that principle, right? You have a pretty sizable management team now, each and every one of them I’m sure have ownership around their functions. You also have a telesales team and I assume that it’s very difficult to maintain the level of speed, the level of ownership, the level of simplicity across all functions, and to make sure that the telesales agent, for instance, reflects well on the customer experience.

So how do you apply those three values on a daily basis?

Giacomo: You’re actually right. It’s not easy to maintain them. I saw also in Lazada when we were growing, we had to kind of go through and re-simplify things over time, because it’s so easy to get your software or your program to get more complex, your processes analysis. I think that element where we saw that is really on how we manage our agents, that somehow we like to say are our customers as well because they use our software.

And those are people that don’t really have necessarily an insurance background. So if we don’t make things simple, you have a loss of screw-ups and that translates into really bad customer experience. Everything on our software for agents is really straightforward and is really a controlled environment where it’s really hard to make mistakes.

Samir: Well, that’s good. And I think if anything, COVID19 is the year of making sure that the company is resilient. It’s the year of making sure that whatever you’ve built stands the passing of time. It’s the year of making sure that your playbook works. So I think you’ve done a tremendous job at standardizing processes across the company.

So we spoke about the past. We spoke about your playbook.

Let’s take a look at what’s ahead. Can you share with our listeners and with us, if you want to fast forward five years from now, what is Lifepal going to be like?

Giacomo: If we talk more about 2025, so a little bit longer term, I think it’s really important for us to stay really focused on the customer experience and deliver value to them. And this means three points for us.

The first one is to really keep our transparent content and policy reviews on the website. So customers can really find all the information with clarity and transparency, and they really can trust us and can avoid those misleading behavior from traditional agents.

The second one is we need to keep growing our selection. We already are the company that has the largest selection of brands and policies in the market. So customers can really find what is right for them and not what an agent is trying to push them to buy.

And lastly is really the convenience that happens pre and post-purchase. So we will be focusing more on our application post-sales and how we can really stay close to the customer when an emergency happens.

So we really aim for the long-term to become the number one shopping destination for insurances and the most trusted brand about insurance Indonesia. Our tagline is your reliable friend, the friend you can trust and rely on when emergency and delicate matters around insurance really happen.

“We really aim for the long-term to become the number one shopping destination for insurances and the most trusted brand about insurance Indonesia.”

Samir: We really hope that you’re going to become the reliable friend for anybody who’s looking for an insurance product in Indonesia, regardless of its complexity. So to close things off we always ask our guests to share some of their favorite things in our rapid-fire question round.

What is the biggest takeaway you have from the YC program?

Giacomo: First was the product-market fit. And this is what founders should focus on in the early days, especially before raising big rounds. Many startups from my experience die because they do not find product-market fit. Even if they have raised large rounds, they would just die later or they will stop growing. So really build something people want, not what founders want or maybe even the investor wants. And then raise your Series A only when you are sure that you have that.

The second is to scale the business with technology and product. Don’t throw people to problems, but develop solutions that are scalable with software. We apply this principle in Lifepal. We haven’t increased headcount, just a little bit, but since January last year. So it’s been really a year where headcount has been flat but we are growing tremendously just with technology and product.

“Don’t throw people to problems, but develop solutions that are scalable with software…it’s been really a year where headcount has been flat but we [were] growing tremendously just with technology and product.”

What is the biggest takeaway you have from your time as a founding member and exec at Lazada that you have brought to Lifepal as CEO?

Giacomo: So the first one is that execution eats strategy for breakfast. Strategy can be done at night, over the weekend, but during the day you need to execute. And if you’re as a CEO maybe you don’t necessarily have to execute everything, but make sure people execute and get that full commitment and motivation from everyone.

The second was that we saw that Lazada really scaled fast. So we saw that your role as a leader, but also as an individual contributor in a fast-growing startup will change roughly every six months. And it’s really important to accept this change. I see many people rejecting it maybe in a direct manner may be more in our subconscious, but really maintain this mindset of becoming a technical expert in every role and in every evolution of the company.

So you may be asked to do a year in digital marketing, can be financed logistics, or it can be also seniority like now you’re asked to be CMS but then maybe in six months, you’re asked to be a CMO So really keep that flexibility because the company, every six month change and I saw many people not being aware of that.

“We saw that your role as a leader, but also as an individual contributor in a fast-growing startup will change roughly every six months. And it’s really important to accept this change.”

What is one thing you learned in your experience so far leading Lifepal that you wish you had known earlier?

Giacomo: Yeah I started realizing that hypergrowth is not for everyone. And I’m realizing that not everyone has the origin and personality to grow the business or a department by 30-40% every month for years. Many people like the idea but they actually fail to execute. And this is really hard because lots of times it’s the motivation because it’s really hard to grow 40% especially in the early days when resources are limited and you need to really be focused. So I’ve seen people accepting smaller growth because hypergrowth is painful or maybe they are unable or unwilling to grow personally or willing also to find the resources externally.

So to solve this problem I changed my hiding criteria. Before I was hiring by startup fit. That has always been really important, especially in the early days. Now I started hiring by fast-growing startup fit. And if a person has been part of a startup that grew like 3-5x a year this person probably is comfortable with hypergrowth and thinks that it is even normal. Otherwise, it can be painful for many people, this journey.

Samir: I’m curious about what makes it painful in your experience. What makes it so difficult for a “normal growth person” to adapt to this? What are the key challenges that a person like that would face?

Giacomo: Sometimes product-market fit and product iteration take time. And even if you get it, really few companies get product-market fit that really is exponential. Lazada was not really exponential by magic. It was us in the beginning who really pushed the growth and really understand things and execute things and solving problems.

And this is something that doesn’t come for free. And it’s a lot of stress, right? Because you don’t know how the future will look like. You don’t know if you’re going in the right direction or maybe you have been failing the past six months. So this kind of sense of uncertainty and the fact that you need to push it and it’s not automatic makes it really draining.

And I think that uncertainty can be really heavy for many people. On the other side. I think people who have lived that, actually have this mindset where they actually accept that it is tough. Maybe because their first job was actually in a fast-growing startup, so they don’t even know how easy things are in like a nice corporate.

And sometimes I meet with people that say, “Oh, you’re growing 40% a year. Oh, this is really slow. When my previous company did IPO, we were growing much more.” And then you meet the opposite person, ” Oh 40% you are kind of the idol.” So you really see different perspectives of what is normal and it’s really hard to change how people see normality.

Samir: I think that’s very, very helpful for anybody who’s listening here and either wants to recruit or become a founder. Hypergrowth is really a mentality that needs to be entrenched from day one, essentially.

Giacomo: It doesn’t mean that if you didn’t experience it in the past, you cannot do it, but just let’s have this awareness and this clarity that that’s the journey we are going through and it’s going to be tough.

“Hypergrowth is not for everyone…I started hiring by “fast-growing startup fit”. And if a person has been part of a startup that grew like 3-5x a year this person probably is comfortable with hypergrowth and thinks that it is even normal. Otherwise, it can be painful for many people, this journey.”

Anything you’d like to plug or announce?

Giacomo: We are hiring and have many exciting positions for people that want to become their SuperHeros and fast track their personal growth.

You will learn from people that have built Lazada from day zero and you will be part of one of the most exciting startups in Indonesia. We have raised one of the biggest rounds in insurtech in Indonesia and we are growing 30-40% every month. We would be really happy to share this amazing journey with you and make sure we protect everyone.

Samir: If you are interested in joining a fast-growing insurtech in Indonesia, I highly recommend reaching out to Giacomo and his team. On that note, thanks Giacomo for coming over On Call with Insignia. I’m sure our listeners learned a bit more about the insurtech world and how it is fast-evolving in Indonesia. It has been a privilege to have been partnered with Lifepal, and we look forward to all the good work you’re doing to improve access to insurance for Indonesians.

About our guest

Lifepal CEO and co-founder Giacomo Ficari

Giacomo Ficari is the CEO and co-founder of Lifepal. So Giacomo was previously co-founder of Aspire, which is a Southeast Asia SME challenger neobank, and also an Insignia portfolio company. Prior to venturing into FinTech he has built leadership experience in Asia’s e-commerce space with companies like Lazada, leading up Lazada Malaysia, and Groupon, where he was the CEO of Japan and Malaysia. He’s also a Y Combinator and Rocket Internet alumni.