Southeast Asia is no longer just a region for tech investment and expansion.

…Because it’s become much more than that. It’s also become a starting point for global talent to build global companies, and the region has come a long way.

Phase 1 was before Southeast Asia was view collectively as a group of emerging market economies ripe for tech and venture capital investment. The momentum was to attract global capital and talent into the region.

The history of Southeast Asia is one of global convergence and a new wave of convergence has come with technology companies

Phase 2 was when the Southeast Asia narrative attracting investors and strategic players went into full swing as local startups sought to become regional market leaders. The momentum was to produce regional players to deliver on this promise of Southeast Asia outcomes.

This convergence in Southeast Asia has strengthened amidst two contexts…

Phase 3 sees Southeast Asia as a destination for global talent to produce companies with a global presence.

A lot of the trends we’ve written about in terms of company building these past few months all contribute to this evolving role of the region:

- vertical AI or AI-as-a-Service (lowering barriers to tech) as with WIZ.AI or bluesheets

- growth stage companies shifting from 3P to 1P (increasing margins for market expansion and establishing global differentiation) as Carro and Pinhome are doing for cars and homes respectively

- slowdown and saturation of tech in more mature markets pushing talent to start companies from emerging market regions like Southeast Asia

- big tech and emerging consumer brands focusing on Southeast Asia as a key growth market

Today the role of Southeast Asia is evolving

Building a company with a global presence is not limited to market expansion.

- There are B2B / B2B2C companies like Intellect growing with the multinational partners and customers.

- There are companies that are inherently global from day one because of the global nature of problem they are solving like Finmo with global treasury pain points or Janio with cross-border logistics.

- There are also companies that create a global presence competitively even if they are just focusing on a single market because of the highly localized approach they take, companies like Ajaib’s approach to growing the investing class in Indonesia or Super reinventing retail in tier 2 cities to rural Indonesia.

There are a few pathways to build a global presence…

Market expansion is not cheap

Market expansion is not cheap, especially for B2C brands and companies, but there is a way…

Localization can take up a lot of resources if not done effectively, and even if there is a “playbook” to replicate across markets, it’s never a 100% copy paste

There will always be that “replication risk” inherent, and competitive advantages for brands and companies expanding across markets will be built on this ability to reduce the risks around replication

A lot of this ability hinges on robust partnerships, as we’ve learned from our portfolio companies, and these partnerships can take on multiple forms:

- Carro acquires leading local players in different markets and partners with leading players of specific functional areas (content, tech, aftersales), today operating in 7 markets (Singapore, Indonesia, Malaysia, Thailand, Taiwan, Hong Kong, Japan)

- Igloo built a distribution network globally to drive sales of their smart access technology, today distributing to 50+ markets across 6 continents

- Intellect built partnerships with leading healthcare providers like IHH Healthcare and Accresa to distribute their mental healthcare programs for employees across Asia and the US, today with 3.5 million+ members across 22 markets

- Dr Clear built an ecosystem of third-party dental clinics and healthcare groups in addition to their own flagship clinics, today with hundreds of third party and self-operated clinics across 7 markets.

While partnerships seem like an easy answer to the playbook replication and market expansion problem for startups looking to keep costs on the low end, there are two questions in particular that always need to be asked as this partnership ecosystem is built:

- How do you prioritize partnerships across different markets as well as balance it out with proprietary initiatives as well?

- How do you ensure partners are getting into a win-win relationship?

On question 1, it’s still important for the company to set the standard for how it expects its brand, products, and services to be delivered. It’s also important for the company to not be swayed left and right by demands of each market or partner and focus on what makes the most sense for the overall group.

On question 2, this can be easy to overlook especially if partnerships come inbound, but there needs to be a constant communication with partners on how they are benefiting from the relationship. In some ways this communication can lead to new product discovery or even more cost-effective ways of delivering products and services to a market.

Partnership-driven global presence of market leading consumer brands

Case Study: When it takes more than one CEO to build a global company

While it is important for a startup going global to have a replicable business model, it is just as critical to have leaders ensuring the execution is tailored to the needs and nuances of the market. These leaders are essentially building their own startup in these markets, with the overarching business as the framework in which to operate.

In many ways, scaling a startup geographically is an art of building a startup from the ground up in every market — this could mean quite literally starting from scratch, or even in the case of a joint venture or M&A market entry, integrating the local operations into the wider global operation, both from a process and people standpoint.

Regardless, the leaders in every market need to be able to balance alignment with management with the flexibility to meet the specific needs of their market

Such was the challenge that Carro’s Chief Science Officer Bryan Tan took on, becoming CEO of Carro Indonesia more than a year ago

From an outsider’s perspective, Bryan has already had quite the journey, going from the academe as a nuclear physicist to joining a fast growing tech company, which we’ve covered previously:

But Bryan took this even a step further taking on an even larger executive role with growing the Carro business in one of its first markets and Southeast Asia’s largest market. He went from Singapore to Indonesia, even taking along some colleagues from his data team.

While coming from the unlikeliest of backgrounds for a tech company in the auto industry, he became the right person at the right place at the right time. His work developing Carro’s AI/ML capabilities especially around pricing has been essential to creating a more seamless tie in between Carro’s business work at the P&L level and the tech level.

Having a leader able to bridge this link between P&L and tech has been important for a market like Indonesia where more effort has been needed to drive process automation and market education

It also helped that while he had an academic background he was also keen to take on a role that would require him to be a “people manager”, and be able to marry his existing “tech enabler” role with people management as well.

He and his team have grown Carro Indonesia 5x over the past year, creating momentum for the market and contributing to Carro’s positioning as a global company as the group has been eyeing a potential IPO.

Having Indonesian roots on his mother’s side has made this transition a full circle moment for him as well, in a way giving back to what has played a significant part of his own life as well.

Bryan’s story is one of finding and enabling the right people to take ownership of growth levers that actually suit their strengths, even if it may not be obvious at first.

And Bryan is not alone — Carro’s six other markets also have leaders with their own stories and strengths that align with the needs of the market — and a global company like Carro will continue to need more than one such leader — a global citizen, if you will.

Market Case Study: Japan’s increasing value as a destination market for global companies coming from Southeast Asia

As we’ve seen with companies like used car platform Carro and mental healthcare company Intellect, Japan can be a valuable destination market for Southeast Asia companies for products and services that customers are willing to pay significantly higher on average compared to most Southeast Asia markets.

This is ideal especially for products and services meeting the needs for Japanese enterprise and organizations to undergo digital and/or organizational transformation, as well as outsource business needs that are more efficient to do with a partner startup. Even for B2C or B2B2C focused companies, a Japan entry could work with the right strategic partners.

In particular, Japan’s socio-economic challenges in aging and low fertility, as well as in energy and food security, lend itself as an ideal destination market for companies tackling these issues. The size of their core industries like financial services and auto also align with companies operating in these spaces, providing a big enough opportunity to contribute to a pan-Asia play even if a player only captures a relatively small portion of the market.

With the right go-to-market strategy, a company could leverage its presence in Japan to complement a global expansion strategy that drives healthy unit economics with scale. With enough cash as well, a company from Southeast Asia could invest in Japanese startups and serve as avenues for local entrepreneurs to scale or even exit.

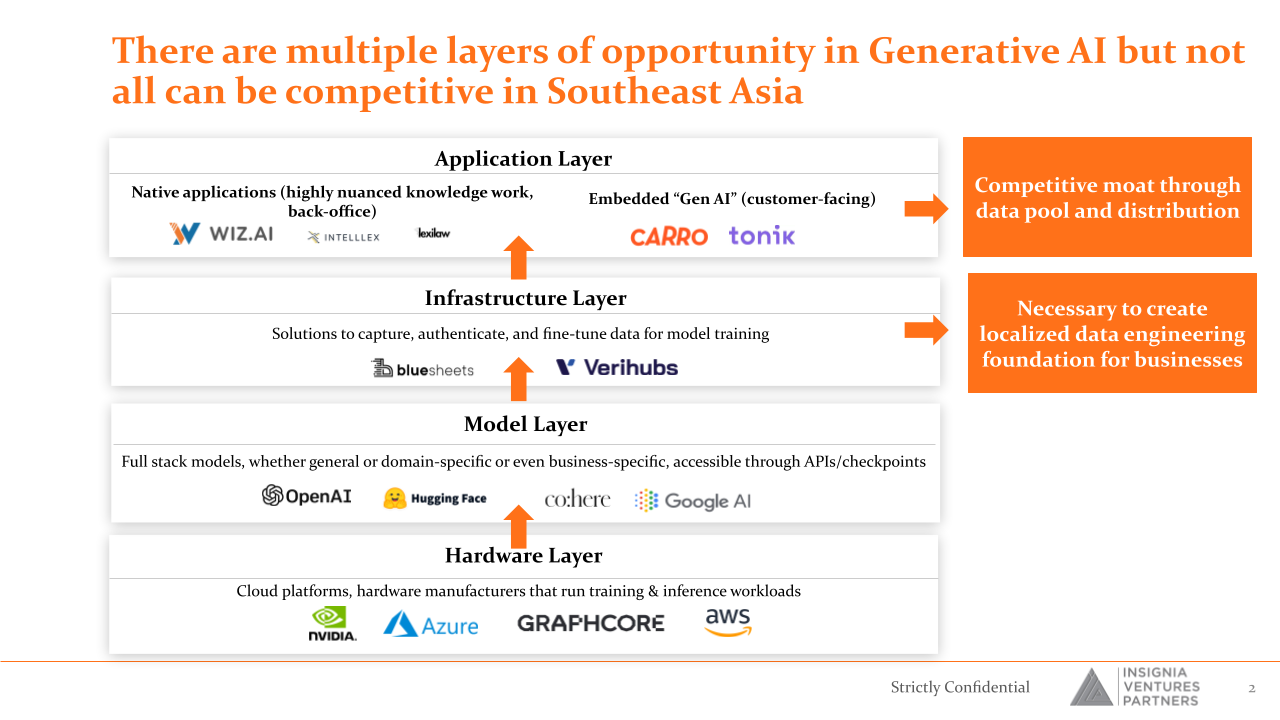

Vertical AI as the competitive edge for Southeast Asia software companies to go global

Where exactly are the winning opportunities for generative AI in Southeast Asia, especially when you already have dominant general LLM players globally and low barriers to entry for AI-native applications?

Going back to the AI / data value chain, AI players from markets in Southeast Asia are more likely to have a competitive edge in the application layer where native applications are able to target highly localized knowledge and backoffice work and non-native apps are able to embed Gen AI to scale acquisition and retention strategies.

A competitive edge also exists for Southeast Asia players in the infrastructure layer, where there is demand for localized data engineering foundations for businesses.

There are multiple layers of opportunity in Generative AI but not all can be competitive in Southeast Asia

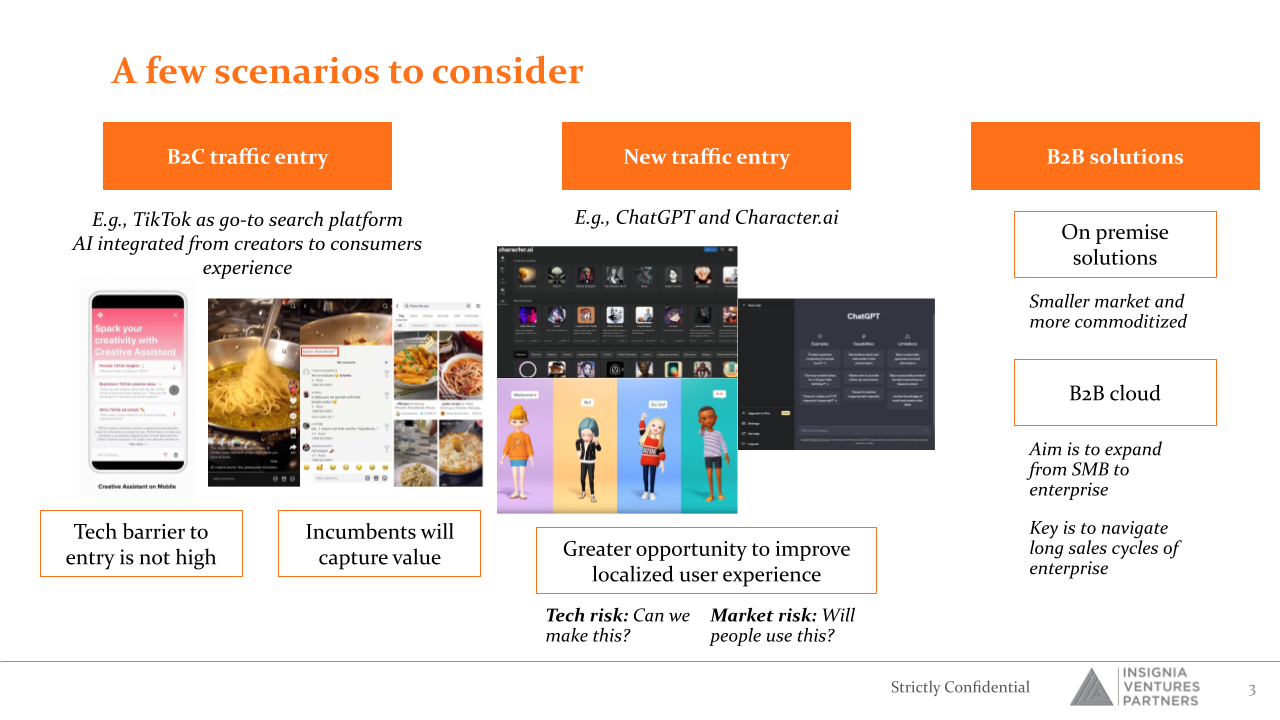

Looking at it from a go-to-market standpoint, B2C is a lot more challenging than B2B given how tech barrier to entry is not high. The threat comes from non-native players with established traffic like TikTok for example, already developing or launching in-house, consumer and business customer-facing generative AI solutions.

Even if an app were to capture new traffic and improve localized user experience, there are still the risks of feasibility (Can we make this (at scale)?) and market fit (will people use this?)

While there is more opportunity to monetize on top of localized B2B generative AI solutions, there is still the typical SaaS challenge of going from SMB to enterprise customers and navigating long sales cycles.

A few scenarios to consider

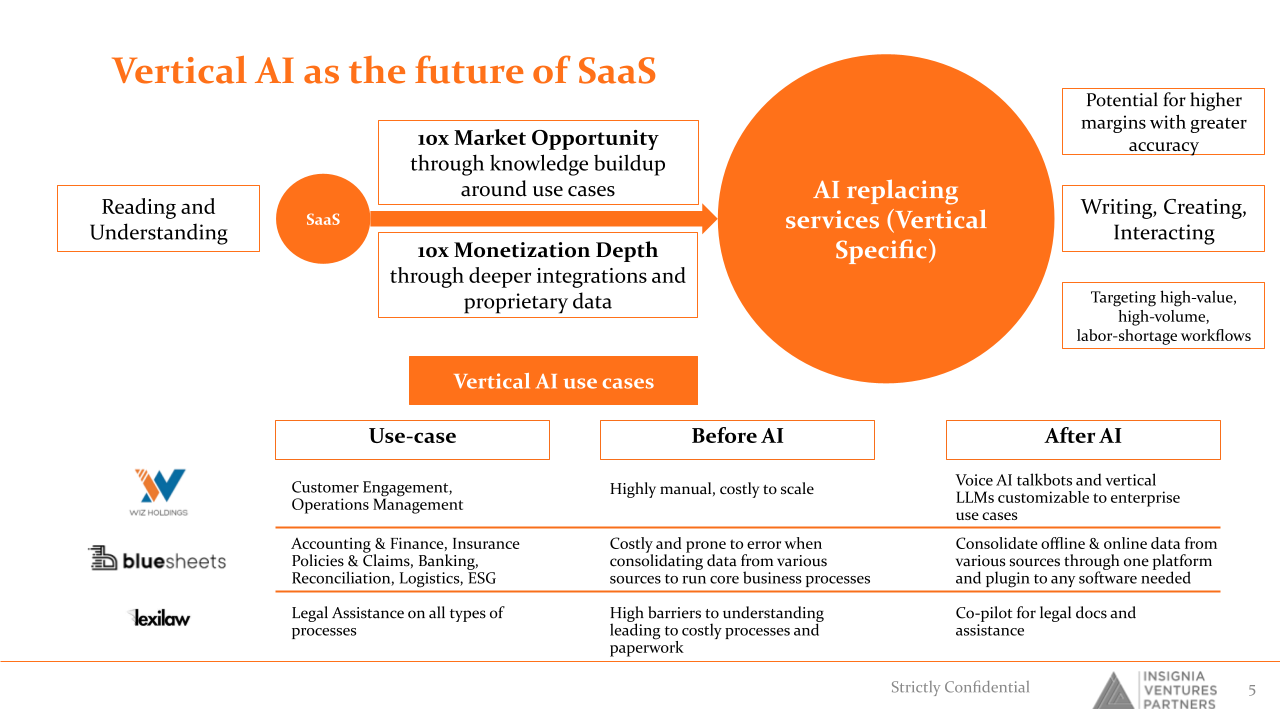

Nevertheless, it is clear that vertical (localized and industry-focused) AI is the future of SaaS. We’ve already actually written about this in a previous AI Notes essay, but from a user and product perspective.

But vertical AI is also the future of SaaS for investors because of how generative AI has the potential to significantly widen the market opportunity and deepen the monetization potential of software businesses. The market opportunity wides through the learning nature of generative AI to service an increasing number of use cases as it trains on more data and builds up a knowledge base.

The monetization deepens as the software solution is integrated into more business functions and tools and trains on proprietary data. There is potential for higher margins with greater accuracy.

By targeting high-value, high-volume, labor-shortage workflows, B2B generative AI solutions can not only create higher margins but also repeat sale and upsell opportunities.

Exponentially increase both market and monetization and you create a blue ocean in investment opportunity.

Vertical AI as the future of SaaS

How do you prioritize tackling a global problem?

Building a company tackling a global problem from day one is a great start in theory, but the biggest question for such an addressable market is:

How do you prioritize growth?

Which pain points, customer segments, and markets are worth spending time on first? What capabilities does the company need to focus on to reduce scaling friction down the line?

Thanks to lower barriers to building with technologies like AI and demand for cross-border solutions across various functions (logistics, finance, operations, etc.), there are more opportunities for global companies from Southeast Asia to emerge. They are globalizing not by moving from one market to the next, but already having an addressable market that is global in nature from day one.

There are a variety of drivers for the emergence of these global addressable markets:

Diversification of treasury for global businesses across markets has led to demand for consolidated treasury platform like Finmo.

The demand for open banking solutions to support cross-border payment solutions and fintechs across emerging markets (e.g., MENA to SEA) has led to opportunity for open finance platforms like Brankas to enable these cross-border transactions.

The emergence of technology supporting digital asset infrastructure enabling companies like Straits (part of Fazz group) to launch solutions like stablecoins to facilitate cheaper atomic settlement of cross-border transactions.

Diversification of supply chains and greater interest in Southeast Asia industries creating opportunity for a logistics 4PL solution like those provided by Janio Asia to manage cross-border logistics in and out of Southeast Asia

Greater awareness and recognition of the financial upside of automating certain business operations leading to demand for solutions to automate frontline operations at scale, like Nimbly’s

But with these opportunities comes not only more pressure around outselling competition, but also pressure around resource allocation and capital efficiency. These global, cross-border problems are often the result of friction across a multitude of moving parts. Without a clear strategy and discipline around product development it is easy to overspend on experimentation and finding product-market fit.

In our recent podcast with David Hanna, CEO of Finmo, he shares two approaches they have taken to reduce the complexity of tackling an inherently complex problem:

Market informs the product: “We’ve actually built directly with treasurers, so instead of building a product, throwing it to market, and then figuring out feedback, we’ve taken treasurers into our product development process and helped give real-time feedback for actual problems they face day-to-day.”

Company-wide focus alignment: “We have a concept internally called the “top five.” On a week-to-week basis, we talk about the top five initiatives company-wide. Each leader and the leadership team hook into those top five because those are the key things we need to solve for our customers.”

Customer-driven global presence of B2B enablers

Case Study: Finmo’s Treasury OS as the Next Stage of Global Payments Platforms

Founded in late 2021 by ex-senior executives at Rapyd, Paypal, Citibank across Australia, Singapore, and the US (all APAC region), Finmo identified a massive opportunity within the global payments industry, particularly in Southeast Asia (US$233B globally, >US$100B in APAC).

And in our podcast with Finmo CEO and co-founder David Hanna, we talked about the company’s role in the evolution of B2B fintech and payments.

“There have been various studies over the last year or so around this space, and the addressable market for B2B flow is about $150 trillion. From our perspective, there’s a sizable addressable market that we’re helping to solve.

When you talk about treasury issues and problems, I think of the example of simple fintechs starting out in the space. Typically, they want to market their product, figure out their runway, and how they can add value to their clients. They need to get a business off the ground.

What we’ve found is a huge demand coming from that space. Fintechs want to serve their customers globally from day one. Gone are the days when you start in one market and then enter another. Now, they have funds collected all over the region and the globe.

Therein lies the problem of treasury. They need to figure out how to de-risk the fluctuation from an FX point of view, get consistency with cash management visibility, and look at yield and return on their funds. Quite quickly, they recognize the challenge of treasury management. That’s what we’re really trying to solve for our customers.”

While Finmo has addressed pain points #1 and #2 initially (RTP rails) as part of its solution, it has purposefully gone a step further to address organizations with collections from different parts of the world and multiple bank or virtual accounts in multiple jurisdictions — this is where today’s treasury challenge comes in:

- How do you bring all those funds together?

- How do you maximize your return on some of these funds that are floating around?

- How do you solve for the spreading out of cash globally to de-risk the bank runs issue that we saw a couple of years ago while maximizing different components of treasury?

- How do you have visibility over cash management throughout the globe, and in various regions depending on where you’re situated, and maximize yield and return capabilities?

- How do you look at your AR/AP processes and how do you manage that in a way that relates to your cash management visibility?

- How do you optimize FX in a way that isn’t just about spot trading from one currency to another?

These questions and more, often posed by treasurers themselves, are what Finmo has been building its modularized solution around.

What has made Finmo’s approach interesting, not just from an industry but also an investment perspective, has been their funds flow-first approach, in contrast to peers that have taken an open banking-first or data-first approach:

(1) Building the “pipes” for real-time payment capability was in response to a fundamental trend David and his co-founder saw when starting Finmo: more global companies were emerging thanks to tech but it is not uncommon to see these organizations holding cash in one environment.

“The catalyst, as I mentioned, is the bank runs, the fact that organizations are global from day one, and the complexity of managing different banking infrastructures around the globe.

These new problems are being faced every day by payment players, fintechs, trade, export merchants, etc. The need to better manage this complexity is clear. Frankly, we don’t see a similar platform in the market today. We believe we are category-defining in terms of the treasury operating system.”

(2) Covering the regulatory bases by securing five licenses around the globe not only allowed them to connect directly into banking infrastructure and operate RTP services across markets, but also build their reputation entering into the market and trust with potential customers entrusting them with their treasury flows.

“From a regulatory point of view, most regulators in the region, particularly around Asia, are starting to become more mature to these types of business models. There is a pretty clear framework in terms of licensing infrastructure. To your point, we went after the licensing component from day one, and now we’ve got five licenses around the globe.

We think that’s our moat, having the ability to connect directly into the banking infrastructure. To do that, you need licensing. You can control the end-to-end experience with our merchant base, and you should be robustly regulated.

From a treasury platform perspective, if we’re holding millions and billions of dollars worth of client funds, we want to be in a position where the most robust regulators are overseeing our business. That’s how we see regulatory compliance and licensing and why we’ve taken this approach from the beginning.”

(3) Addressing the funds flows pain point first opens up a wider pool of potential customers Finmo can build the full-stack treasury OS with.

“Actually, further to that, if you think about the problem we’re solving, at the smaller end of the market, a small flat organization might use accounting software like Xero or QuickBooks. This might be fine for their needs.

At the large end of the market, they might buy software like Ariba or other large enterprise solutions, which can start at half a million dollars and above. You still need to code, develop, and mold it to your business. The problem we’re solving is in that mid-market space, where there’s complexity around the region, multiple bank accounts, and multi-org structures.”

(4) Building with treasurers allows them to build on their modularized approach to tackling workflow issues (e.g., things as simple as logging into 10+ bank accounts daily and downloading all this data into an Excel file / their global treasury book).

“Every treasurer we’ve spoken to over the years has mentioned the challenge of pulling everything together. For example, the CFO might call the treasurer and say, “Spread my cash around to de-risk the banking scenario.” The treasurer then has to consolidate this information, often using various tools and platforms.

They tend to rely on Excel to download data, manipulate it, and figure out their cash position. This is a broken process. What Finmo is doing is bringing all of that together into a single platform to solve the treasury problem.”

(5) More recently, Finmo’s customer-centric approach has led them to developing a white-label solution for customers (like fintechs) to have integrated services for merchants on their own platforms

Building up this solution stack in this way has allowed them to acquire and retain customers from various angles.

“There are organizations tackling this from different angles, such as open banking in mature markets that pull in data insights to a merchant’s banking infrastructure. However, they can’t necessarily move money in real-time…We’ve tackled it in the reverse. We’ve gone after the regulatory aspects, built the pipes, developed the RTP capability, and then laid on top the kind of insight and action, dealing with the treasury solution.

This means that if merchants want to use us for just money movement, in that modularized approach, they can do just that. If they want to take additional value from the treasury component, they can do that as well.”

Go global without going global

Can you build a global presence without going global?

There are advantages to building a global presence even if the company is not focused on global expansion and primarily building market leadership in a single market.

This “global presence” can include:

(1) Having strategic or global investors on board to develop competitive insight, as in the case of Tonik who raised their Series B led by Mizuho or SuperApp (YC W18) who raised their Series C led by New Enterprise Associates (NEA).

These partnerships do not only build up validation in the capital markets for the business, but also can present valuable inroads into key partners or market insights that may have otherwise been more difficult to obtain

(2) Raising debt from global institutions, as in the case of AwanTunai, which recently secured a US$18million debt facility from HSBC.

This builds on the company’s ongoing journey of connecting local and global capital to underserved MSMEs in Indonesia through their proprietary supply chain financing engine.

Depending on the business model, these fundraises could provide not just a validation of the business model but also the level of maturity in the company to be able to pay back.

(3) Building a globally differentiated / comprehensive business that raises the barriers to entry, as in the case of Pinhome with their platform covering all aspects of the home buying journey from home seeking to home services or Ajaib bringing together access to stocks, funds, digital assets, and even banking through one platform

(4) Building up a global team to eventually lay the groundwork for a second or third market, or even just raise the bar and diversify the quality of the organization.

Not all business models can be expanded into other markets as easily as others. Such is the case for highly regulated industries like digital banking or geographic markets like Indonesia where certain market segments can be large enough for startups to focus on.

In certain cases, the monetization within that model already creates a significant addressable market even if the company focuses on one market.

These avenues to build a “global presence” on the competitive landscape, in the capital markets, or in the talent pool can catalyze the company’s path to market leadership or a stable enough market presence to then explore actual market expansion.

Narrative-driven global presence of world-class businesses tackling local problems with global capital

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.