The B2B payments landscape in Southeast Asia has long been characterized by archaic processes, cumbersome manual workflows, and inadequate financing solutions that fail to meet the dynamic needs of modern businesses. Traditional invoice factoring and trade finance options remain shackled by outdated methodologies, extensive KYC requirements, and protracted approval timelines that can span weeks or even months. This creates a significant friction point for small and medium enterprises (SMEs) seeking to scale their operations and optimize their working capital management.

Enter Fluid, a Singapore-based B2B AI payments platform that is fundamentally reimagining how businesses (suppliers and buyers) approach payment solutions.

Founded in early 2023 by a team of seasoned fintech and e-commerce veterans, Fluid embodies a product-first philosophy that brings consumer-grade payment experiences to the traditionally process-heavy B2B commerce sector.

As featured in our recent podcast with CEO and co-founder Trasy Lou Walsh, Fluid represents a compelling investment opportunity that addresses a massive market gap while leveraging proven leadership, innovative technology, and strategic positioning in an underserved market. The company’s mission to “make B2B payments truly fluid” resonates deeply with our investment thesis of backing transformative technologies that modernize traditional industries.

Since its inception, Fluid has demonstrated remarkable traction, achieving 10x growth over the past 12 months across Singapore and Malaysia, disbursed tens of millions and 200k transactions serving 3000+ businesses. This rapid scaling is underpinned by strong unit economics and validated by the company’s ability to secure debt financing term sheets despite its early-stage status.

As Fluid embarks on its mission to revolutionize B2B commerce financing across Southeast Asia, here are five key reasons underpinning our conviction in its transformative potential:

(1) Proven Leadership Team with Exceptional Track Record in Scaling Fintech Operations

Fluid’s founding team represents a rare convergence of complementary expertise across fintech operations, product development, and debt financing – precisely the skill sets required to build and scale a successful B2B lending platform. At the helm is CEO and co-founder Trasy Lou Walsh, whose career trajectory demonstrates an exceptional ability to drive growth and operational excellence in complex, multi-market environments.

Trasy’s experience as Regional General Manager at Atome, one of Asia’s leading B2C BNPL platforms, provides invaluable insights into the nuances of building and scaling payment solutions across diverse Southeast Asian markets. During her tenure at Atome, she played a pivotal role in supporting the company’s remarkable growth from 4-digit GMV to 9-digit monthly GMV within just two years, while simultaneously orchestrating the platform’s expansion across nine countries in Asia. This achievement is particularly noteworthy given the complexity of navigating different regulatory environments, consumer behaviors, and market dynamics across the region.

Prior to her fintech experience, Trasy honed her operational expertise as Head of Restaurant Operations at Uber Eats Asia Pacific, where she demonstrated her ability to optimize complex operational processes at scale. Under her leadership, the restaurant onboarding process achieved a 42% increase in efficiency while simultaneously reducing onboarding costs by 20%, generating millions in savings for the region. This experience in streamlining B2B relationships and optimizing operational workflows directly translates to Fluid’s mission of simplifying B2B payment processes.

The founding team’s expertise is further strengthened by co-founder and Chief Product Officer Steven Li, who brings deep product development experience from his role as the first product leader and early employee at Atome. Steven’s involvement in building Atome’s initial product from scratch provides Fluid with critical institutional knowledge about the technical and product challenges inherent in developing BNPL solutions. His subsequent experience as Head of Product at Coupang Pay in Korea adds additional depth to his understanding of payment platform development in competitive Asian markets.

Completing the founding team is Chief Financial Officer Ruoyun Yang, whose specialized expertise in debt financing represents a critical competitive advantage for Fluid’s business model. As the former Head of Asia at Lendable, a private credit fund, Ruoyun brings sophisticated understanding of debt markets, risk assessment, and capital structuring that is essential for a lending-focused business. Her experience has already proven invaluable, as evidenced by Fluid’s ability to secure multiple debt financing term sheets despite its early-stage traction – a remarkable achievement in the current challenging fundraising environment.

This combination of operational scaling expertise, product development acumen, and debt financing specialization creates a leadership foundation that is uniquely positioned to navigate the complex challenges of building a B2B lending platform.

The leadership team’s proven ability to execute in high-growth, complex environments provides confidence in Fluid’s capacity to navigate the challenges of scaling a B2B lending platform across multiple markets while maintaining operational excellence and risk management discipline.

(2) Massive Market Opportunity in Southeast Asia’s Underserved B2B BNPL Landscape Leading to Further Growth within Payments

The B2B Buy Now Pay Later market in Southeast Asia represents one of the most compelling untapped opportunities in the region’s fintech ecosystem. While B2C BNPL solutions have achieved significant penetration and market validation across consumer segments, the B2B equivalent remains dramatically underserved, creating a blue ocean opportunity for innovative players like Fluid.

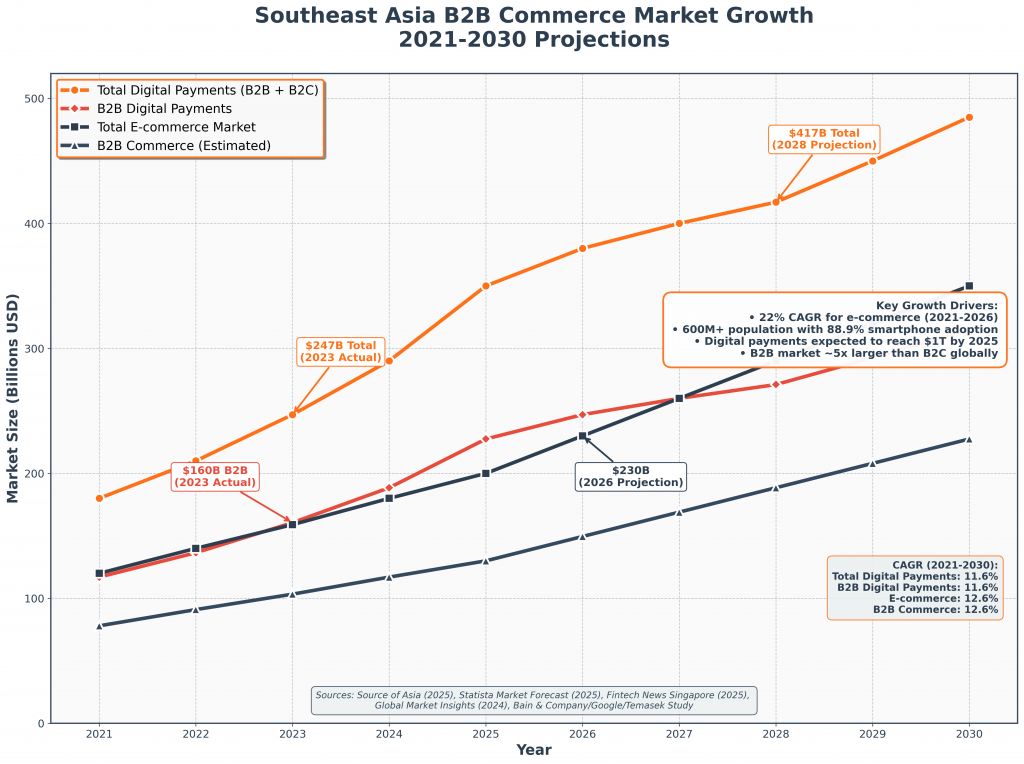

The scale of this opportunity is substantial. Southeast Asia’s B2B financing market represents a net interest income Total Addressable Market (TAM) of US$21.9 billion as of 2023, with Indonesia commanding the largest market share at US$10.6 billion, followed by Thailand at US$4.5 billion. These figures reflect the enormous capital requirements of businesses across the region seeking flexible financing solutions to optimize their working capital and accelerate growth.

To contextualize this opportunity, it’s important to understand that globally, BNPL solutions represent only 2% of the total online payment market as of 2021, according to Block/Afterpay research. This statistic reveals the significant headroom for expansion, particularly in the B2B segment where adoption has lagged behind consumer applications. Industry estimates suggest that up to 30% of transactions will be conducted via marketplace platforms, creating natural integration points for embedded financing solutions like Fluid’s platform.

The demand signals from the market are particularly encouraging. Multiple studies indicate strong appetite for B2B BNPL solutions among target customers. Research from MarTechAsia reveals that 75% of surveyed SMEs worldwide who have used BNPL for personal purchases express willingness to embrace similar payment schemes for their business operations. This finding suggests significant potential for cross-pollination between consumer and business payment behaviors, particularly as business decision-makers become increasingly comfortable with flexible payment solutions in their personal lives.

More specifically within Southeast Asia, 80% of Singapore’s SMEs have expressed interest in installment payment options for small businesses, according to industry research. This high level of interest indicates that the market is primed for adoption of innovative B2B payment solutions, with businesses actively seeking alternatives to traditional financing options that often involve lengthy approval processes and restrictive terms.

The competitive landscape further validates the market opportunity. B2B BNPL is most developed in the United States and Europe, where leading players have demonstrated the viability and scalability of the business model.

However, nearly all leading global players were incorporated between 2018-2022, indicating that even in developed markets, the sector remains relatively nascent compared to B2C BNPL players that typically launched between 2010-2014. This timeline suggests that the B2B BNPL market is still in its early development phase globally, providing additional runway for growth and market expansion.

Critically, the early stage of global B2B BNPL development creates a strategic advantage for regional players like Fluid. Given the complexity and resource requirements of international expansion, it is highly likely that established players in the US and Europe will focus on consolidating their home markets rather than expanding to new geographies in the near future.

This dynamic provides valuable time for local Southeast Asian players to establish strong market positions and build defensible competitive moats before facing potential international competition.

Traditional invoice factoring companies, while present in the market, typically focus on blue-chip invoices from multinational corporations and rely on cumbersome manual processes that are poorly suited to the dynamic needs of SMEs and e-commerce transactions.

The market timing is particularly favorable as businesses across Southeast Asia increasingly embrace digital transformation and seek more sophisticated financial tools to optimize their operations. The COVID-19 pandemic accelerated digital adoption across B2B segments, creating greater openness to innovative payment solutions and embedded financing options. This shift in business behavior, combined with the massive addressable market and limited competition, positions Fluid to capture significant value as the market leader in Southeast Asia’s B2B BNPL space.

(3) Early Traction Linking Product-Market Fit to Investor Trust and Interest

Despite being founded in early 2023, Fluid has demonstrated remarkable early traction that validates both its product-market fit and the sustainability of its business model. The company’s growth trajectory over its first 18 months of operation provides compelling evidence of strong market demand for its B2B BNPL solution and the effectiveness of its go-to-market strategy.

The most striking indicator of Fluid’s momentum is its 10x growth achievement over the past 12 months across Singapore and Malaysia. This exponential growth rate is particularly impressive given the typically longer sales cycles and higher customer acquisition costs associated with B2B fintech solutions. The fact that Fluid has achieved this growth rate while maintaining operational discipline and unit economics demonstrates the scalability of its platform and the strength of its value proposition.

Fluid’s early traction is evidenced by its ability to secure debt financing term sheets despite its early-stage status. The ability to secure debt financing is particularly critical for Fluid’s business model, as access to low-cost capital directly impacts the company’s ability to offer competitive rates to customers while maintaining healthy margins. The fact that debt providers are willing to extend financing to Fluid at this early stage suggests that the company’s underwriting approach, risk management systems, and overall business fundamentals have passed rigorous institutional due diligence processes.

Fluid’s customer success stories further validate its market traction. The company has successfully onboarded clients across various industries, including traditional suppliers and online marketplace platforms of all sizes, including Coca-Cola, Treedots, Eezee (another Insignia Ventures portfolio company), among others.

One case study is that of Ben & Belle, a Malaysian coffee roastery that was previously burdened by manual payment chasing and reconciliation processes. By implementing Fluid’s automated payment and reconciliation solutions, Ben & Belle was able to eliminate these operational inefficiencies and focus on core business growth activities.

Fluid has also successfully raised more than US$7 million since its founding, including a US$5 million round in 2024. This fundraising success in a challenging market environment reflects investor confidence in the team’s execution capabilities and the market opportunity. The capital raised provides Fluid with sufficient runway to continue scaling its operations and expanding its market presence while working toward sustainable profitability.

The combination of strong growth metrics, healthy unit economics, successful debt financing, and diverse customer adoption creates a compelling foundation for continued expansion and market leadership in Southeast Asia’s B2B payments space.

(4) AI Payments Platform Delivering Consumer-Grade Experience to B2B Commerce

User journey for buyers ordering through website with value proposition for suppliers / sellers

User journey for buyers ordering through ERP with value proposition for suppliers / sellers

Fluid’s technological approach represents a fundamental departure from the traditionally process-heavy, finance-centric solutions that have long characterized the B2B payments landscape. By applying a product-first philosophy drawn from the consumer fintech playbook, Fluid has created a platform that delivers the seamless, intuitive experience that modern businesses expect from their financial tools.

At the core of Fluid’s differentiation is its AI-powered underwriting engine, which leverages data aggregation from both first-party and third-party sources to enable more precise risk assessment and faster decision-making. This sophisticated approach to credit evaluation allows Fluid to offer instant credit approval through what the company describes as a “zero-question approach,” eliminating the lengthy application processes and extensive documentation requirements that typically characterize traditional B2B financing solutions.

The AI-driven underwriting system represents a significant competitive advantage in the fragmented B2B lending landscape. By pooling transaction data across multiple suppliers and marketplace platforms, Fluid can develop increasingly sophisticated risk models that account for industry-specific patterns, seasonal variations, and business relationship dynamics that traditional credit scoring methods often miss. This data aggregation creates a virtuous cycle where increased platform usage enhances underwriting accuracy, which in turn enables more competitive pricing and broader market access.

Fluid’s platform architecture is designed for seamless integration with existing business systems, including websites, mobile applications, Enterprise Resource Planning (ERP) systems, ordering platforms, and accounting software. This integration capability is crucial for B2B adoption, as businesses are typically reluctant to adopt solutions that require significant changes to established workflows or create additional operational complexity.

The platform’s automated reconciliation functionality addresses one of the most persistent pain points in B2B commerce: the manual matching of buyer payments to supplier accounts. Traditional B2B transactions often involve complex reconciliation processes that require significant administrative overhead and are prone to errors and delays. Fluid’s automated approach eliminates these inefficiencies, allowing businesses to focus on core operational activities rather than payment administration.

From a user experience perspective, Fluid has successfully translated the intuitive design principles of consumer fintech applications to the B2B environment. The platform offers flexible payment terms with transparent pricing, enabling buyers to access financing options at the point of purchase without navigating complex approval processes or lengthy credit applications. This consumer-grade experience is particularly valuable in the B2B context, where decision-makers increasingly expect the same level of convenience and transparency they experience in their personal financial applications.

The platform’s approach to risk management and collections also reflects its technology-first orientation. Rather than relying on traditional collection processes that often involve manual intervention and relationship management, Fluid has built automated systems that handle the entire process from risk assessment through collections and reconciliation. This automation not only reduces operational costs but also provides more consistent and predictable outcomes for both suppliers and buyers.

Fluid’s technology stack is designed to handle the complexity and scale requirements of B2B transactions while maintaining the speed and reliability that businesses require for their operational workflows. The platform can process transactions across multiple currencies and jurisdictions, accommodate various payment terms and structures, and integrate with diverse marketplace and e-commerce platforms without requiring extensive customization or technical integration work.

The company’s focus on data security and compliance is particularly important given the sensitive nature of B2B financial transactions and the regulatory requirements across different Southeast Asian markets. Fluid has implemented enterprise-grade security measures and compliance frameworks (ISO 27001 certified) that meet the stringent requirements of institutional customers while maintaining the user-friendly interface that drives adoption.

One of Fluid’s most significant technological innovations is its ability to provide suppliers with immediate payment (often on Day 1) while offering buyers flexible payment terms. This capability requires sophisticated cash flow management, risk assessment, and capital allocation algorithms that can balance the competing needs of different stakeholders while maintaining platform profitability and risk discipline.

The platform’s real-time analytics and reporting capabilities provide businesses with unprecedented visibility into their payment patterns, cash flow dynamics, and financing utilization. This data-driven approach enables more informed financial planning and working capital optimization, creating additional value beyond the core financing functionality.

Fluid’s technology platform also demonstrates impressive scalability characteristics. The automated nature of its core processes means that the platform can handle significant increases in transaction volume and customer base without proportional increases in operational overhead. This scalability is essential for capturing the large market opportunity in Southeast Asia’s B2B commerce sector and achieving the unit economics necessary for sustainable profitability.

The combination of AI-powered underwriting, seamless system integration, automated reconciliation, and consumer-grade user experience creates a comprehensive technology platform that addresses the full spectrum of B2B payment challenges while delivering superior outcomes for all stakeholders in the transaction ecosystem.

(5) Strategic Early Mover Advantage in Southeast Asia’s Blue Ocean B2B BNPL Market

Fluid’s positioning in Southeast Asia’s B2B BNPL landscape represents a classic blue ocean opportunity, where the company can establish market leadership in an underserved segment with limited direct competition. This strategic positioning provides multiple advantages that compound over time, creating increasingly defensible competitive moats as the market develops.

The competitive landscape analysis reveals that Fluid faces minimal direct competition from established players with comparable capabilities and market focus. While several companies operate in adjacent spaces, none have achieved the combination of scale, technology sophistication, and market traction that Fluid has the potential to grow into. One company focuses primarily on invoice management SaaS with financing as a secondary offering, while another targets a narrower MSME inventory financing niche.

This competitive vacuum is particularly significant given the substantial barriers to entry that characterize the B2B lending space. Building a successful B2B payments platform requires the convergence of multiple complex capabilities: sophisticated risk assessment and underwriting systems, regulatory compliance across multiple jurisdictions, debt capital access and management, technology integration capabilities, and deep understanding of B2B commerce workflows. The combination of these requirements creates natural barriers that protect early movers like Fluid from rapid competitive encroachment.

Traditional financial services providers, while possessing capital and regulatory expertise, typically lack the technology capabilities and product development agility necessary to compete effectively in the embedded finance space. Invoice factoring companies and trade finance divisions of banks are constrained by legacy systems, manual processes, and risk frameworks that are poorly suited to the dynamic, technology-driven approach that modern B2B commerce requires.

Fluid’s strategic positioning provides multiple pathways for value creation and market expansion. The company can leverage its B2B payments platform to expand into adjacent financial services, develop industry-specific solutions, or pursue geographic expansion across Southeast Asia and beyond. The foundational capabilities and market relationships that Fluid is building today create optionality for future growth initiatives that may not be available to later entrants in the market.

The combination of limited direct competition, high barriers to entry, network effects, data advantages, and favorable market timing creates a compelling strategic position that should enable Fluid to capture significant value as Southeast Asia’s B2B commerce financing market continues to develop and mature.

References

- Arthur D. Little – B2B BNPL Market Analysis (January 2025): https://www.adlittle.com/en/insights/viewpoints/b2b-buy-now-pay-later-huge-emerging-opportunity

- Source of Asia – E-commerce Market Analysis (January 2025): https://www.sourceofasia.com/e-commerce-market-in-southeast-asia-2025-2026/

- Global Market Insights – B2B Digital Payment Market (October 2024): https://www.gminsights.com/industry-analysis/b2b-digital-payment-market

- Fintech News Singapore – Asia Payment Trends (January 2025): https://fintechnews.sg/106915/e-wallets/asia-payment-trends-2025-digital-finance-revolution/

- Business Wire – Southeast Asia E-commerce Growth (March 2025): https://www.businesswire.com/news/home/20250311192743/en/Southeast-Asias-E-Commerce-to-Reach-New-Heights-Driven-by-Digital-Payments-and-Cross-Border-Commerce-Growth

- Southeast Asia Market Research – Digital Payment Landscape (July 2024): https://www.southeastasiamarketresearch.com/insight/trends-and-development-of-sea-digital-payments

- IBS Intelligence – Digital Payments Growth (February 2025): https://ibsintelligence.com/ibsi-news/tap-pay-spend-how-digital-payments-are-surging-in-southeast-asia-india/

- Asian Banking and Finance – APAC Card Payments (May 2025): https://asianbankingandfinance.net/cards-payments/in-focus/apac-card-payments-markets-grow-43-247t-in-2025

- Statista Market Forecast – Southeast Asia Internet Economy (January 2025): https://www.statista.com/statistics/1007199/southeast-asia-internet-economy-size-market/

- Gulf Business – B2B BNPL Global Trade (January 2025): https://gulfbusiness.com/b2b-bnpl-transformative-potential-in-global-trade/

- Statista – Digital Payments Asia Pacific: https://www.statista.com/topics/9335/digital-payments-in-the-asia-pacific-region/

- Verified Market Research – Asia Pacific Fintech (February 2025): https://www.verifiedmarketresearch.com/product/asia-pacific-fintech-market/

- Research and Markets – Digital Payments Report (March 2025): https://www.researchandmarkets.com/reports/5939641/digital-payments-market-report

- Sirma – B2B BNPL Context Analysis: https://sirma.com/insights/from-credit-to-convenience-the-rise-of-bnpl-in-the-b2b-context.html

- Fluid Podcast Interview: https://review.insignia.vc/2024/08/14/trasy-lou-walsh-fluid/

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.