“Adventure is the life of commerce, but caution is the life of banking.” – Walter Bagehot, British journalist, businessman, and essayist

Highlights

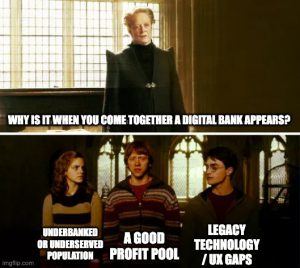

- Different seeds and growth trajectories but there is such as thing as “fertile ground” in digital banking: (1) underbanked or underserved population, (2) a good profit pool (proven by incumbent banks), and (3) weak / legacy incumbents (referring to technology).

- As lines blur between traditional and digital banks, and even beyond banks with open finance and more channels to develop and deliver financial services, the competitive landscape boils down to which players are able to serve their customers’ needs the best and retain them in the long-term.

- This customer focus means reframing customers from account holders (how to get customer to open and keep account) to DAUs (how to provide value-adding services), and this approach is producing mutant, segment-specific banking models.

- When it comes to fintech, fin without tech gets left behind, tech without fin comes and goes. Digitization can only be sustained if it’s built on top of rational decision-making structures (especially for lending and financing), data-driven expansion, and disciplined scale.

In the Finovate Edge: Asia event on 13 July 2022, our founding managing partner Yinglan Tan joined Asian banking leaders WeLab Group COO Ernest Leung and Kota Mahindra Bank Chief Digital Officer Deepak Sharma on a panel on “The Rise and Fall of Asia’s Digital Banks”, moderated by FinTech Futures reporter Shruti Khairnar.

Insignia Business Review has featured digital banking and adjacent business models quite a lot, including:

- this thesis article on the fully digital banking proposition as an evolution of the fintech rebundling

- learnings on the ground behind the Philippines’ first fully digital bank

- the power of embedded insurance

- a case study on the “all-in-one finance OS” play

- a survey of the different ways fintechs are building their own digital banking propositions for specific segments.

It’s clear that there’s always more to learn, and therefore write, about the topic, especially as the tech market continues to evolve (with growing pains). So through insights shared on the Finovate panel, we revisit (1) what makes a digital bank work, (2) how it stacks up against traditional banks and vice versa, and (3) the long-term value of digital banking, through four key insights shared on the Finovate panel.

(1) Different seeds and growth trajectories but there is such as thing as “fertile ground” in digital banking

Different market segments and geographies targeted by digital banking propositions have resulted in the emergence of different business models. There are models serving the unbanked and underbanked or others serving the digital-savvy millennials or even children (i.e. the parents make deposits for them). There are models focused on improving access to credit or more lending-focused.

In order to best cater to their target customers, different players have taken different strategies.

In the panel, Ernest talks about WeLab as a digital-only bank in Hong Kong, where “Hong Kong is by no means an underbanked market…[but they were] looking to provide services to a segment of the population that has decent wealth but perhaps underserved [because they were] not meeting the sweet spot of [traditional] banks.”

Regardless of the trajectory, Yinglan adds that there are three important criteria for digital banks: (1) underbanked or underserved population, (2) a good profit pool (proven by incumbent banks), and (3) weak / legacy incumbents (referring to technology). He shares that in the Philippines, these criteria existed and provided the fertile ground for Tonik to rapidly grow its user base and deposits in its pioneering fully digital bank.

(2) Competitive landscape between traditional and digital banks boils down to the customer

Fully digital banks have the ability to move faster and deliver more catered services, with digital-first understanding (i.e. data) of the customers. This means digital banks are ideally able to reach that holy grail of personalizing offerings to a “segment of one,” in a significantly shorter period of time than traditional banks.

For WeLab, spotting the market opportunity for a digital-only banking proposition in Hong Kong put them ahead of the game today, but the lines are blurring, as Ernest adds, “The big boys have their own digital initiatives or are spinning off. As one of the first movers, we have an advantage of being ahead, however, the lines between a digital-only bank and [a bank becoming digital] are blurring.”

The lines are even blurring beyond banks, with Kota Mahindra Bank CDO Deepak sharing that the “form and shape of financial services is rapidly changing,” with “embedding finance moving [financial services] away from physical [bank] branches to retail stores”, enabling even non-fintechs to break into services that banks or even fintechs have had a monopoly over. That said, Deepak also adds that traditional banks “still enjoy the trust of the common depositor or investor” and that is keeping incumbents where they are.

With the competitive landscape becoming more complex, thanks to the various channels and proliferation of data access through which financial services can be developed and delivered, how does a digital bank stay focused and stand out amidst the noise?

Ernest cites that while the fundamentals for a digital bank are actually (and should actually) be the same as incumbents (i.e. trust, presence, customer service, risk management, regulatory compliance) and even for regimes like Hong Kong requirements, guarantees and protections are the same for digital banks and incumbents, differentiation and distinction mean going beyond building the fundamentals and “building for customers, a customer-centric bank.”

He cites a feature of WeLab Bank in Hong Kong, where small depositors are able to pool together savings to get higher interest rates, developed catering specifically to customer behavior and needs in the market. Features like this stemming from understanding the customer have ripple effects in lowering customer acquisition costs and lengthening customer lifetime value.

(3) Shift in focus from accounts to DAU resulting in mutant, segment-specific banking models

Because digital banking services are now operating on the same platform as many other apps (which may also have banking services embedded), then framing customers as “account holders” may no longer be good enough to compete.

For Yinglan, “the competition [of incumbents] is not the banks down the road but the fintechs.” When it comes to digital evolution and transformation, banks need to think like tech companies. Emphasizing the previous point, it’s all about “providing services that customers are comfortable paying for.”

This means framing customers as “daily active users,” and think about how the digital banking proposition is continually able to be a part of the customer’s regular transactions.

“If you’re just trying to move the bank teller to an app, I don’t think there’s much value there,” Yinglan adds, “whereas if you’re combining services…” and he cites the examples of Indonesian fintech unicorn Ajaib, which he describes as a globally unique case of having a bank, a stock brokerage license, and a crypto license.

Essentially it’s an evolution of existing billion-dollar tech companies (i.e. Robinhood, Chime, Coinbase), where users in Ajaib can deposit in their accounts, buy shares of their preferred stock, then diversify with crypto holdings as well.

(4) When it comes to fintech, fin without tech gets left behind, tech without fin comes and goes

Amidst the rush to digitize, Yinglan cautions that fundamentals are still important. “Fintechs tend to have a lot of “tech” but not a lot of “fin”…[we’ve seen] irrational lenders that come and go…” Digitization can only be sustained if it’s built on top of rational decision-making structures (especially for lending and financing), data-driven expansion, and disciplined scale.

This is a philosophy shared and discussed further by AwanTunai CEO Dino Setiawan on our podcast:

And even with the bear market, the leaders on the panel remain optimistic especially from a user adoption and market opportunity perspective, as fertile ground still remains for more digital banking seeds to be planted (again, segmentation is proliferating). For WeLab for example, they have been building up their own proposition for Indonesia, to leverage their investments and learnings from Hong Kong into another geography.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.