In the Forbes Asia 100 To Watch Webinar on November 24, three managing partners of Southeast Asia venture capital firms came together to talk abo ut navigating today’s fundraising landscape, among them our own Yinglan Tan, Openspace Ventures’ Shane Chesson, and AC Ventures’ Helen Pei-Hua Wong. As we usually do with these kinds of panels, Insignia Business Review took notes and for this discussion, put together a list of the more practical and salient points for founders to take away.

ut navigating today’s fundraising landscape, among them our own Yinglan Tan, Openspace Ventures’ Shane Chesson, and AC Ventures’ Helen Pei-Hua Wong. As we usually do with these kinds of panels, Insignia Business Review took notes and for this discussion, put together a list of the more practical and salient points for founders to take away.

While we have written throughout the year about fundraising amidst market headwinds, with at least one fundraising article every quarter…

- January 2022: Raising your first round of funding? Founder-CEOs share fundraising best practices feat. conversations from Season 1 to 3 of On Call with Insignia

- May 2022: 7 Learnings on Cost-Cutting, Fundraising, and Growth for Startups in the Winter feat. nine of our growth-stage portfolio founders

- September 2022: Creating Competitive Contrast, Buying Opportunities in the Winter, Relying on the Right Partners to be Self-Sustaining: Counterintuitive Measures in a Bear Market feat. advice from Fazz founders Hendra Kwik and Tianwei Liu, as well as Yinglan Tan

…this particular list is in its own class, coming from the experiences and bird’s eye view perspective of seasoned venture capitalists. There are some points here that have appeared in the previous articles above, and just prove that these bear repeating especially as the winter shows no clear signs of ending any time soon. There are also some points here that may be just as relevant for the startup investor, who is also pressured in this environment to find truly quality early-stage opportunities and put dry powder to good use.

This list features eight key points:

1. Never underestimate the regulatory side. Large, fast-growing market? Check. A business model with positive unit economics? Check. Proven and capable founder with market fit? Check. Clear regulatory alignment / approval / accreditation? This last point is often overlooked, whether intentionally or not, but it can be the tipping point that puts a company in a bind in the midst of fundraising, especially in the later stages and in this environment, as later-stage investors will be more cautious.

2. Never too early for a company to set in place rigorous corporate governance and frameworks for institutionalization. It pays to build for maturity early on, even if seed or pre-seed investors may not be focusing on these things. A simple way to begin doing this in the early days of the company is to start building up the company’s finance function, either bringing in a finance-savvy and trustworthy founding team CFO or hiring a finance controller who could grow with the company. This is important arguably even regardless of whether the CEO is finance-savvy or not, as the finance function serves as a key balance in the organization’s growing complexity. Another useful mindset in this regard is to raise the next round already in mind and have a long-term view of what the company needs to achieve for a substantial exit amidst the hustle of everyday operations. Easier said than done from an individual CEO / founders’ perspective, but that is what management teams and startup boards are for — to provide that additional perspective a founder or CEO could miss juggling all these different aspects of taking a company off the ground.

3. Goodbye to cheap money. The fast and easy fundraises of the tech markets are gone. Founders are pressed to work towards at least 36 months of runway or be profitable within that period. Investors, in spite of maybe having more money to deploy, will have a higher bar for deployment in terms of unit economics and other company-specific metrics.

4. Winters call for creativity in securing money. Especially for capex-heavy companies, considering other sources of creative capital or non-dilutive capital (as the cost of dilution increases) are best on the table, like debt financing (capex-heavy companies are better positioned to set up collateral).

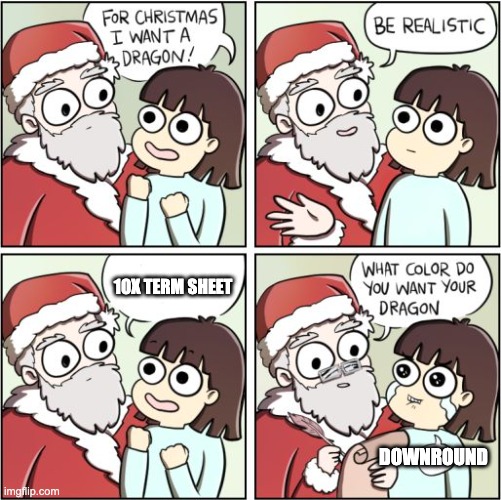

5. ‘Tis the season of flat rounds and downrounds. The nature of this downturn is a price correction, and this inevitably comes with flatrounds and downrounds (already 25-35% in Europe). The priority is to get money in the bank, and use that money to grow the company’s actual value, as opposed to magically growing its paper value expecting purely favorable term sheets.

6. The focus should be on growth. The best defensive measure in a winter is to be pragmatically aggressive. Fundraising in a market with higher bars, tighter wallets, and more caution demands more from the company’s pace and quality of growth. Healthy growth will ultimately attract investors more than any other fundraising tactic. Here the advice to build a finance function or have a CFO comes into play as well, as they can provide a clearer picture of a company’s usable cash position (which is not as simple as money in the bank, because there are payables, receivables, illiquid assets, etc. to consider) and from there the rest of management and the board can come up with pragmatic and realistic strategies to work this usable cash into the company’s growth trajectory. This mindset of leveraging growth is also important with respect to cost-cutting — a company can cost-cut to the bone, but without growth, get into a vicious reductive cycle where any future prospects are also diminished. Navigating today’s markets is not about pulling the plug on spending but spending more efficiently.

7. The unstoppable founder can turn things around. The three most common points of failure in early-stage startups tend to be the lack of product-market fit, founder disagreements, and running out of cash — the risks for all of three of which are only exacerbated in today’s markets. But another commonality for all three of these is that an unstoppable founder can turn things around.

In the panel, Yinglan gave the example of Super — whose story we have covered many times on Insignia Business Review, most recently as a result of their feature in the Harvard Business School case study on Insignia Ventures — given the company went through several pivots with a gamified media company to SaaS company to finally a social commerce platform for rural Indonesia that brought the company to the next level of growth. The previous iterations of the company could have been points of failure or stagnation, but Steven was unstoppable in the sense of exploring new opportunities and leveraging his advantages (partners, team, and his own experience) to execute on these new opportunities.

8. Never short tech. Amidst the price volatility in recent years, people are building — and the key for founders and investors is to not be swayed by either the hype or the doom and gloom (one would argue that they should go in the opposite direction — be wary of the hype and aggressive amidst the doom and gloom). As this relates to sectors in particular, investors are looking at those relatively more immune to the cyclicality of markets and price volatility, like those working in healthcare or sustainability, and solving massive and complex problems like fragmentation in Indonesian agriculture. At the end of the day, venture capitalists are playing the long game. As Yinglan put it, a simple question to reflect on a potential partnership is, “can we see ourselves in business with the founder/s in the next 12 to 15 years, with a large enough problem, a product that customers love, and an unstoppable founder? There’s nothing more rewarding than that as a venture capitalist.”

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.