Fintech. Monetization. Diversification. These three words best summarize Insignia Business Review’s takeaways from this year’s Google, Temasek, and Bain Economy SEA 2023 Report.

In this article, we highlight these takeaways and how they tie into themes we have covered throughout this year.

- Diversification: Funding cycle reverts to 2017 levels towards a focus on early-stage opportunities, but with higher bars on company performance and openness to previously non-traditional segments. Diversification also refers to companies taking an ecosystem approach to growth, leveraging on adjacencies with higher margins and stronger retention to build up their monetization strategy.

- Monetization: Higher bars on company performance and higher cost of money mean greater focus on monetization for venture-backed companies. When looking at market segments, it’s not just about market size potential but about revenue per user potential. Companies are then more likely to focus on high value users, and this focus on high value users drawn out in the long-term could result in a deeper digital divide.

- Fintech: Digital financial services have taken on a significant share of revenue over the past year, and show continued momentum in markets like Indonesia, Vietnam, and the Philippines, where the growth potentials are highest. In particular, embedded finance and wider integration of digital financial services across platforms as adjacent revenue sources will create an “arms race” towards bridging capital access (i.e., proprietary underwriting algorithms / credit bureaus for unbanked segments or previously uncovered products and services). This aligns with lending being the largest driver of revenue for DFS and loan demand continuing to grow in spite of rising interest rates. Ultimately, digital financial services arms race is ultimately a data arms race, as companies with more robust data infrastructures and flywheels will be better positioned to offer more comprehensive and complex financial products and services.

Back to Basics in SEA Digital Economy, but not quite

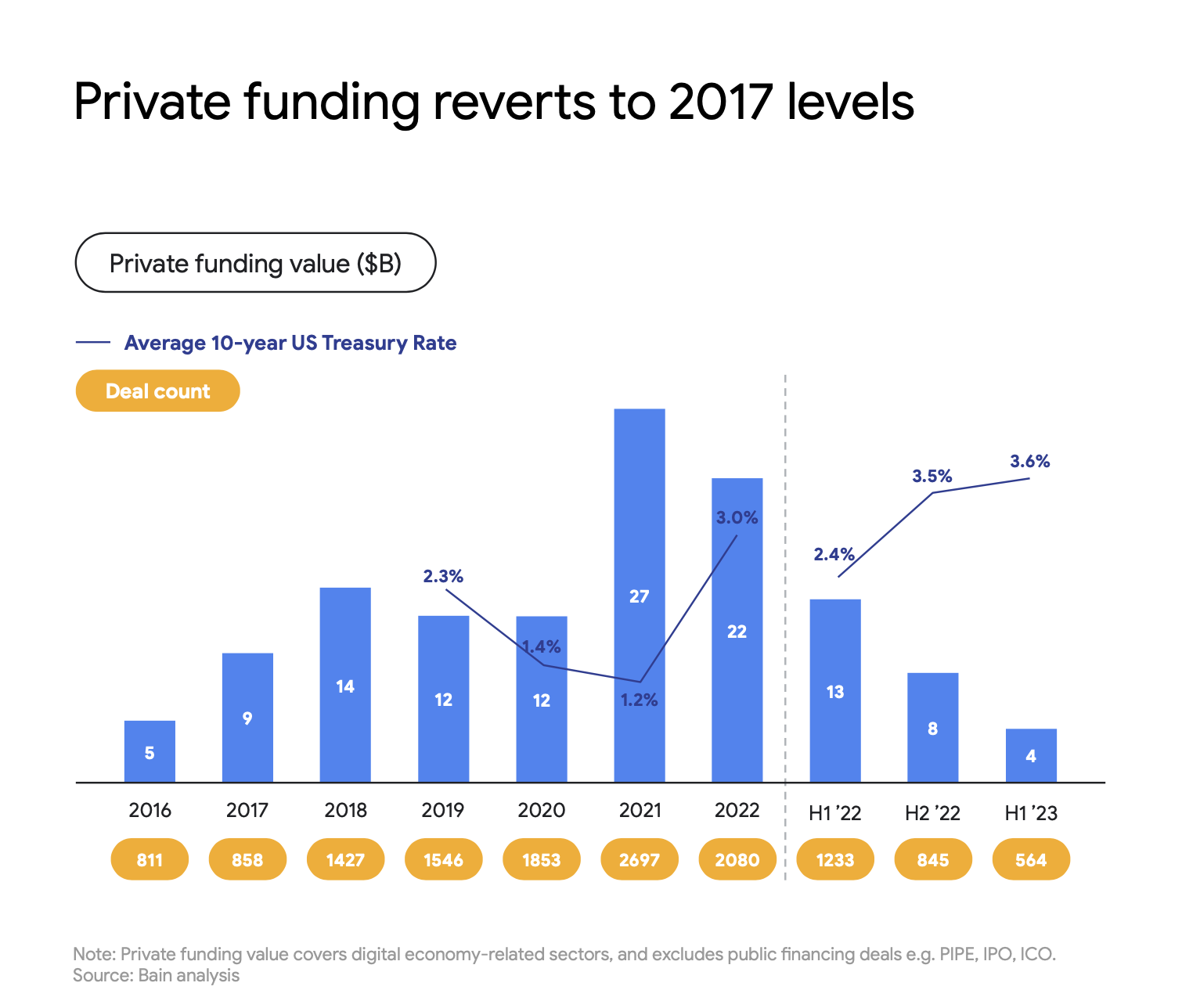

Page 18 of the report states “Private funding reverts to 2017 levels”, illustrating how funding activity in 2023 rounds out to similar amounts as in 2017, and how this has been trending in a similar way to the global interest rate environment (with the US Treasury Rate as proxy).

Private funding reverts to 2017 levels

Tying this into the broader story of Southeast Asia, this return to 2017 levels is not pure coincidence. It also signals a return to focus on early-stage opportunities, albeit with more mature investor expectations. 2018 to 2019 saw the fruits of this early-stage focus in pre-2017 funding, with the creation of many of the region’s current unicorns and participation of many global investors like Softbank, KKR, Meta, Google, etc. There was already word in the market of a bubble in late 2019, especially following the failed We IPO, but the bubble didn’t quite burst in 2020 thanks in part to the digitalization rush induced by the pandemic.

The pandemic delayed the market cycle reset (ie. return of investment activity towards earlier stage rounds). Unfortunately it also created a higher “fall from grace” for startups especially in terms of valuations, but now the cycle has reset with majority of funding in H1 2023 has gone to sub 50M rounds.

Market cycle rest in SEA digital economy

But at the same time, it also heightened the potential and strengthened the Southeast Asia growth story, demonstrating company resilience amidst the pandemic then the high interest environment, as well as digital adoption’s continued growth. As page 49 in the report shares, cash is no longer king, with more than 50% of digital economy transactions facilitated by digital payments.

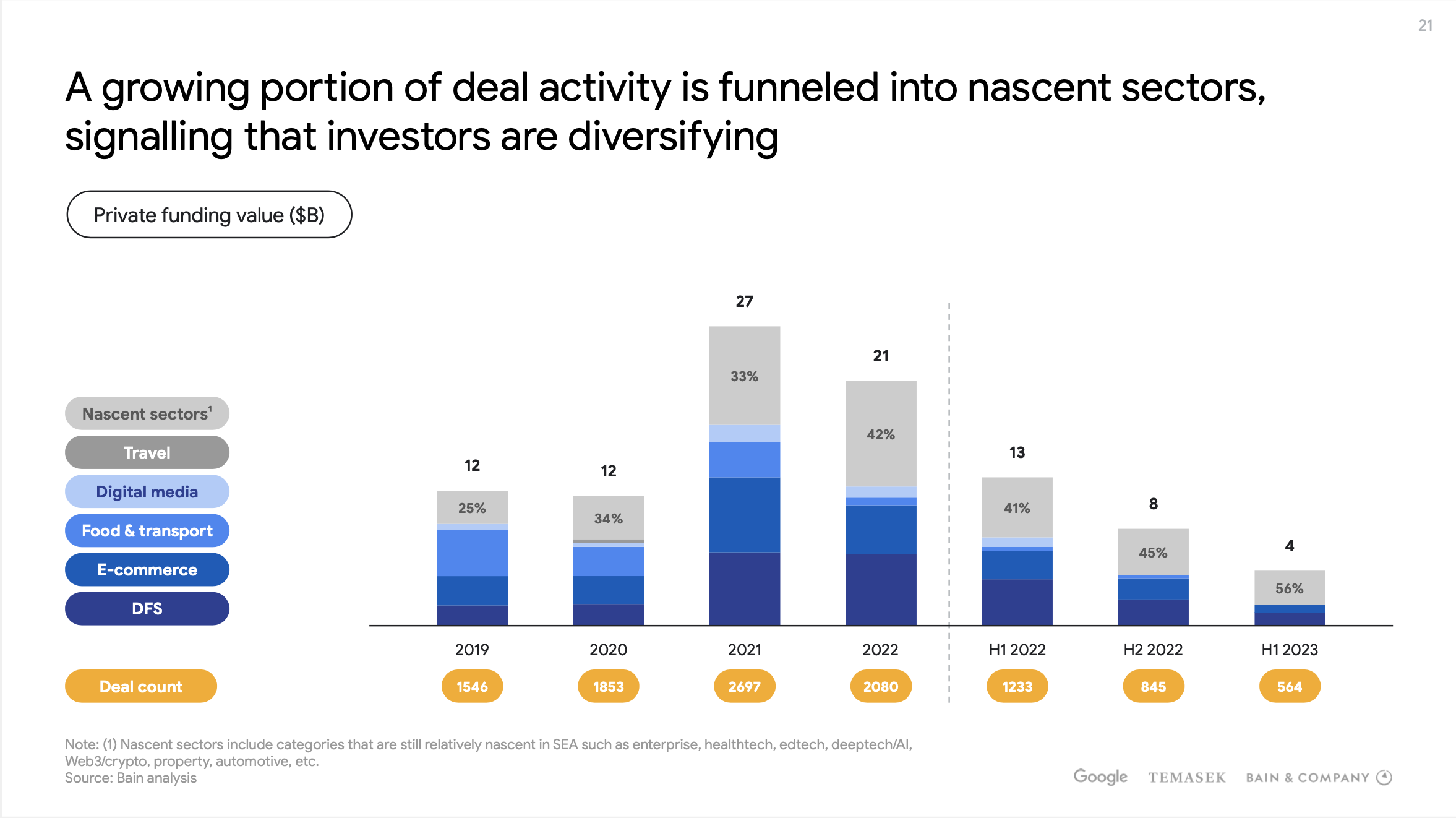

This catalysis in Southeast Asia’s digital economy, combined with the return to early-stage opportunity, sees greater capital being committed to what the report calls “nascent sectors” in page 21. These sectors could be “nascent” in a few ways, either in terms of technological development like AI, or in terms of digitization, say like agriculture or rural commerce. Investments into these “nascent sectors” will be critical for the maturity of Southeast Asia’s startup ecosystems, as these sectors will often demand more innovative or uniquely ASEAN business models and products — think Aplikasi Super’s approach to social commerce or WIZ.AI’s LLM for Bahasa.

More opportunities for investment in SEA digital economy

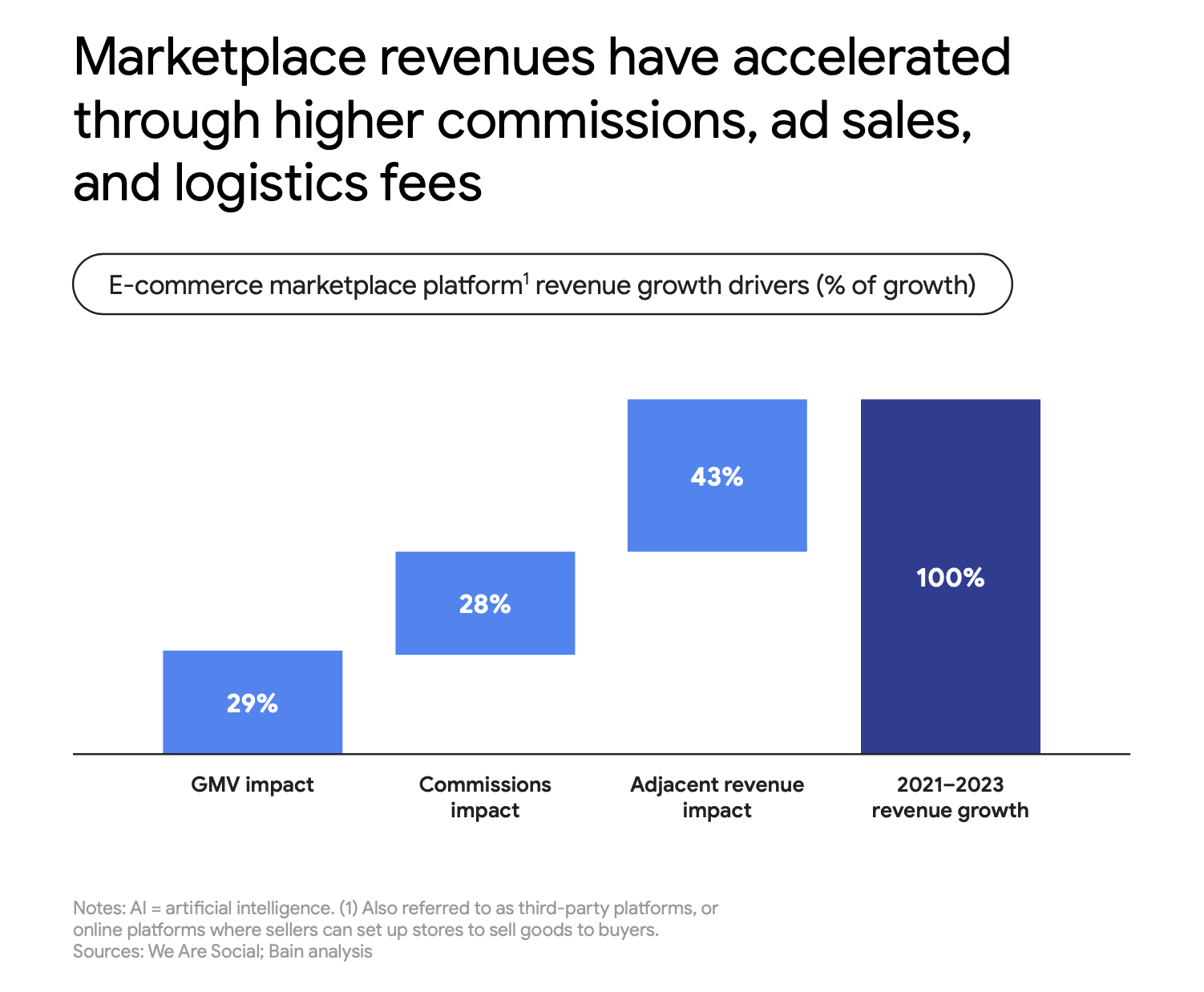

Diversification also refers to companies taking an ecosystem approach to growth, leveraging on adjacencies with higher margins and stronger retention to build up their monetization strategy.

In page 34 of the report, marketplaces are illustrated to derive 43% of their revenue from adjacencies, pointing towards the viability of the ecosystem approach.

We dive deeper into how companies in Southeast Asia have implemented this ecosystem approach in this article.

Marketplace revenue breakdown

Monetization Focus’s Long-Term Impact on SEA’s Digital Economy

This ecosystem approach is just one way companies are improving their monetization strategy with higher bars on company performance and higher cost of money in today’s market.

We write about monetization strategies among other considerations in company building in today’s market environment in this article.

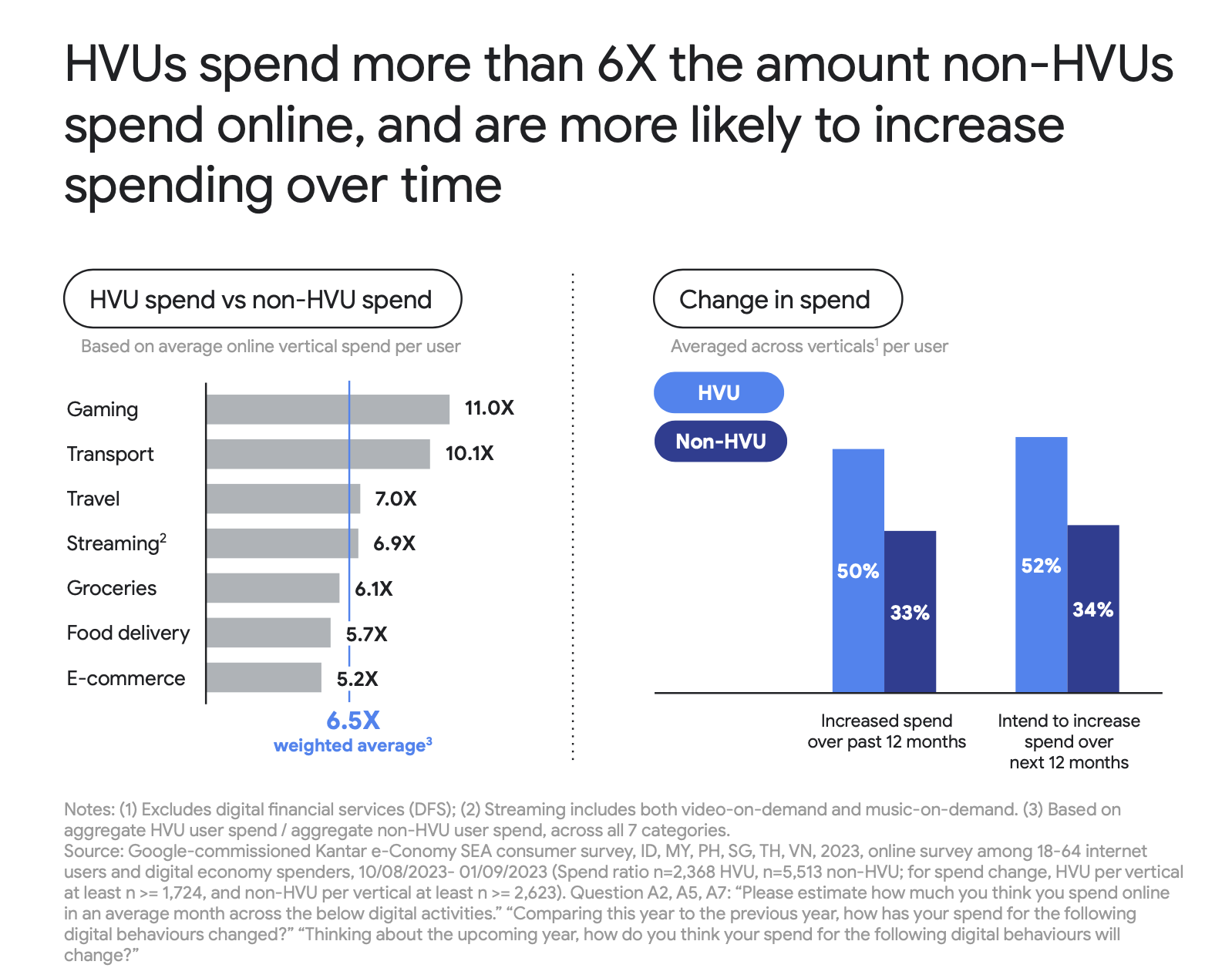

Companies are also focusing on high value users, and the section in the report covering this particular focus illustrates just how stark the difference is in terms of spend between high value users and non high value users. Page 58 is just an example.

High value users vs non-high value users in SEA digital economy

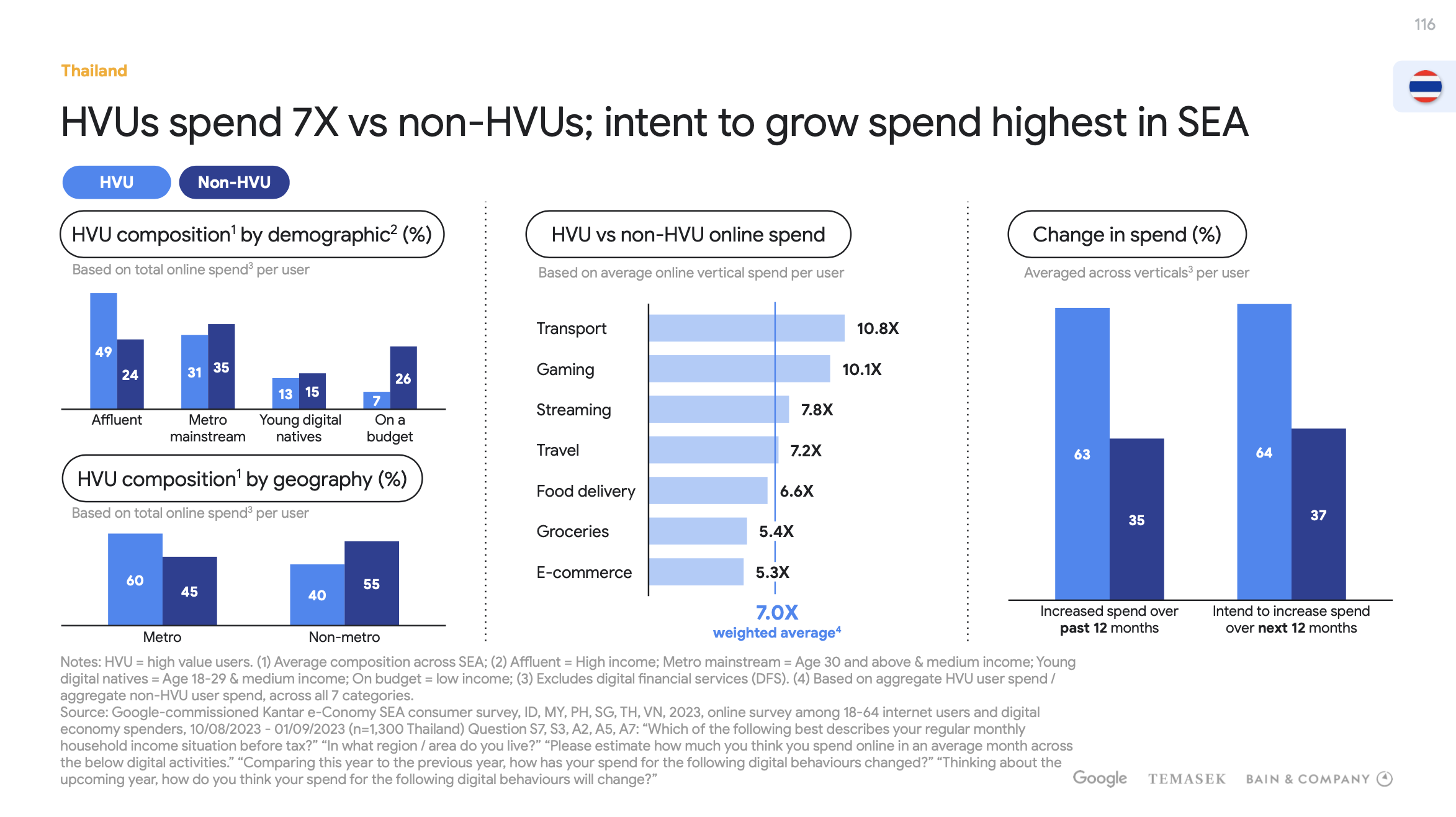

This focus on high value users has some interesting implications. This could bring greater focus towards economies or market segments with higher spend and intent to spend as opposed to just a higher user count or user base. Take Thailand for example. It’s not just about market size, but revenue per user.

Thailand’s beauty market is the best example of this revenue per user potential, as the CEO and co-founder of Konvy, Qinggui Huang, shares on our podcast.

Thailand’s monetization potential

Impact of monetization focus on high value users

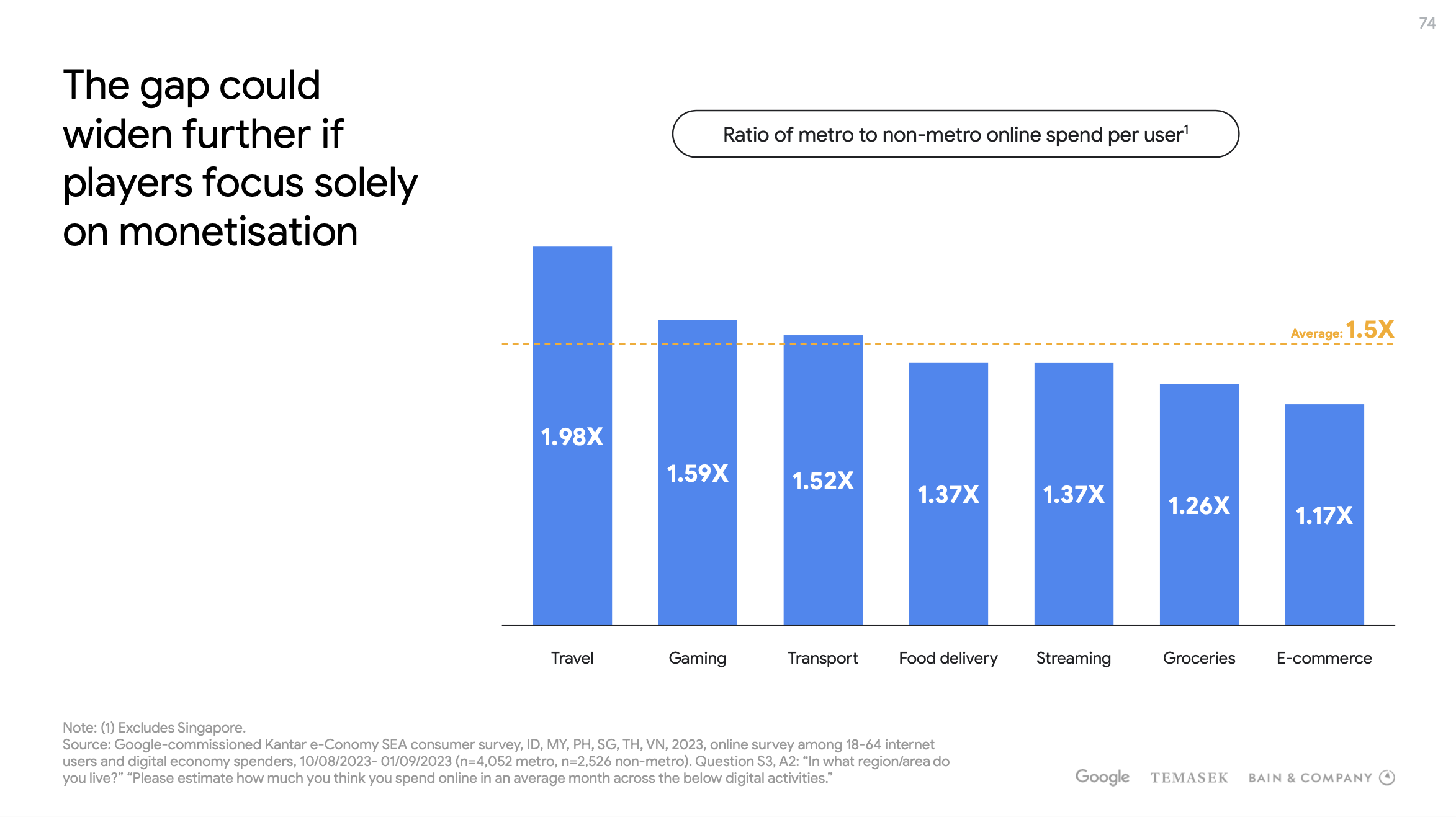

This focus on monetization could have long-term impacts on the gap between the maturity of metro and non-metro digital economies, as illustrated in page 74 of the report.

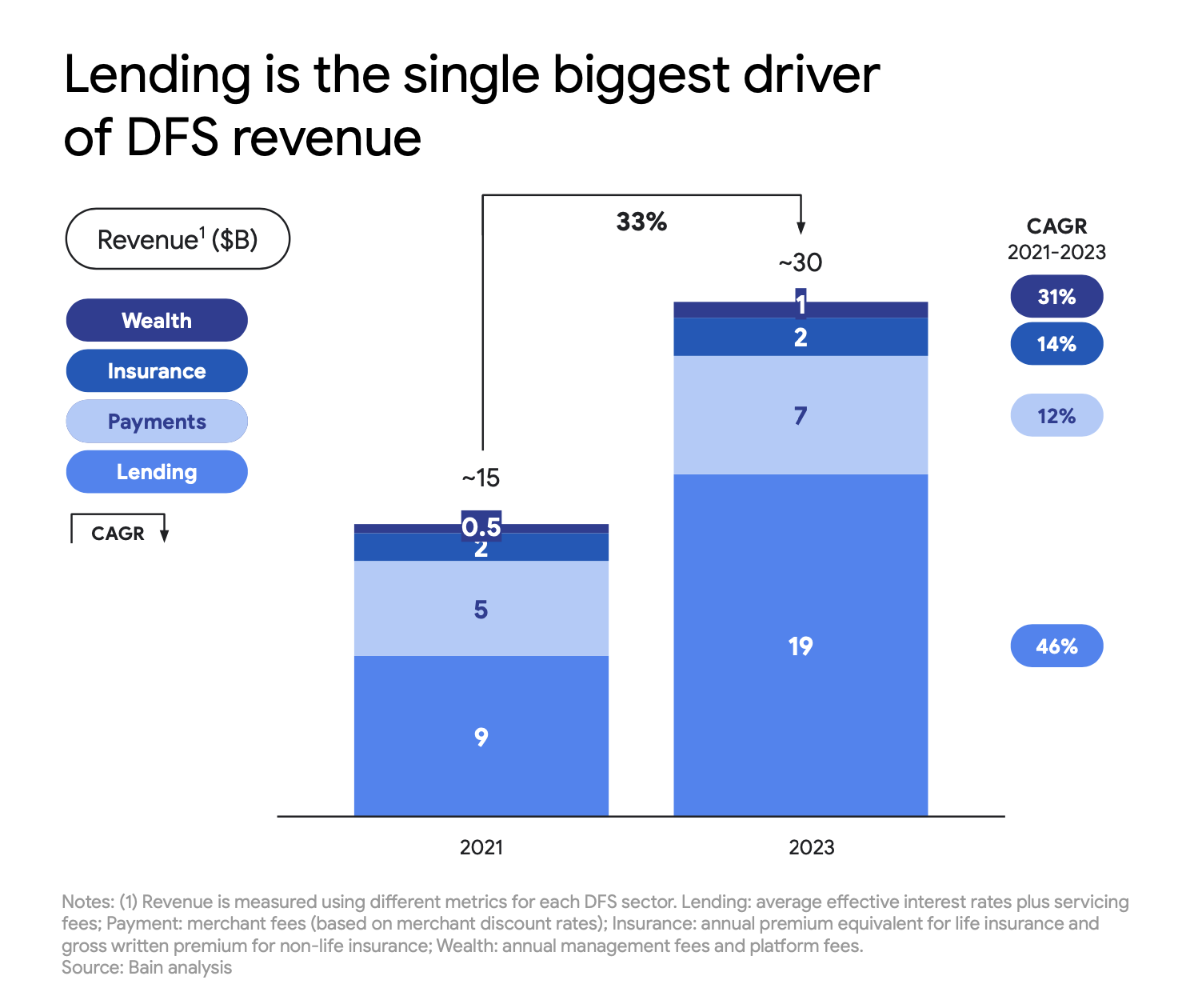

Digital financial services arms race is ultimately a data arms race

Digital financial services (DFS) took up a significant share of last year’s revenues (30%) (Page 30), with lending being the biggest driver of DFS revenue (Page 48).

Lending as single biggest driver of DFS revenue

This is a confluence of multiple factors, with companies looking to diversify into adjacencies to improve monetization and customer journeys (financing, insurance, payments playing a massive role here), and access to capital being a key barrier to overcome for greater participation and spending in the digital economy.

Fintech for Southeast Asia used to be about bringing the bank into the digital economy, but now it has become about improving the digital economy itself. We can expect more companies to go beyond offering pure financial services and really positioning fintech products and services as a means to a greater end — whether that’s improved treasury management or financing for a car or a home.

That’s because fintech is about more than just financial services — it’s about data. Ultimately, the arms race to improve consumer experiences with financial services is tied to, if not runs on the same track as, the arms race to build up robust data infrastructure and data lakes.

This link between fintech to every aspect of the digital economy through embedded and open finance is something we have written extensively about, especially with regards to its implications for AI adoption in the region.

What are your thoughts on this year’s e-Conomy SEA 2023 report?

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.