We took a look at the largest acquisitions in the last two years, based on the acquiree’s equity funding leading up to the acquisition as listed on Tracxn. See the list at the end of this article.

Broadly these acquisitions fall into four categories that are not mutually exclusive.

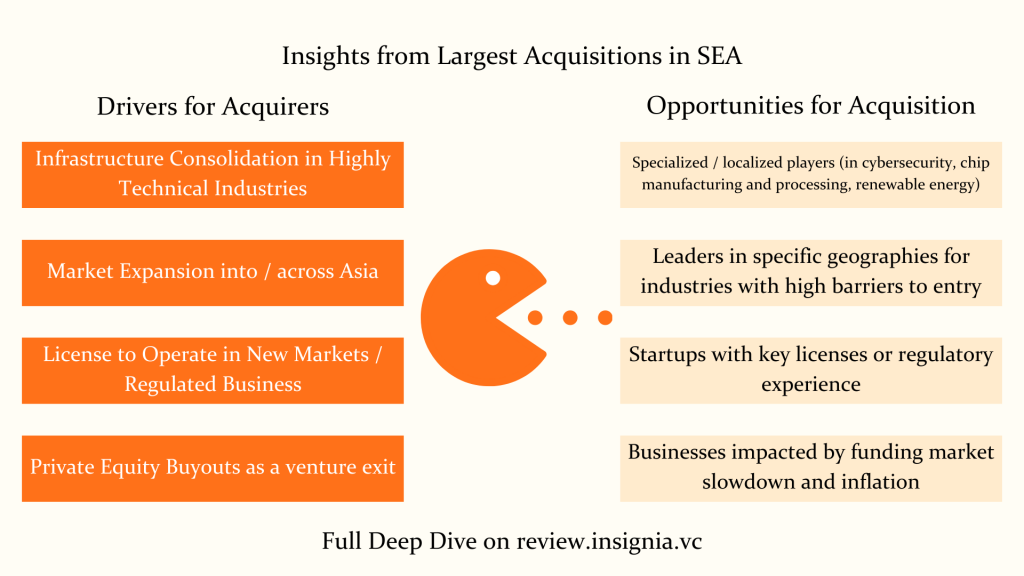

(1) Infrastructure consolidation in highly technical industries

These acquisitions cover industries like cybersecurity, chip manufacturing and processing, or renewable energy where (1) there is high fragmentation in services, creating demand for one-stop / end-to-end partners, (2) there can be high risk in depending on external parties for certain capabilities especially if the acquirer’s core business depends on these technological components (think cloud companies and chips).

These acquisitions reflect a larger pattern where companies are competing to “complete the puzzle” and build or buy critical infrastructure to de-risk dependencies.

The opportunity lies for startups that are highly specialized across the value chains of these industries at the frontier of innovation, and have patents for example that would be attractive to acquirers looking to buy certain capabilities or de-risk their supply chain.

Examples here include the Nebula Energy acquisition of AG&P.

(2) Market Expansion into / across Asia

We’ve covered this trend quite a lot on Insignia Business Review, especially the types of expansion we see, from day-one global companies to cash rich Japanese corporates looking for targets in the region.

The opportunity lies for startups and companies that are market leading in their respective geographies, and operate in industries where there is a high barrier to entry for non-local players due to regulation or operational nuances (i.e., proptech, fintech, auto).

On the other hand, we have seen how other startups like Carro have grown across Asia through a mix of strategies that have included acquisitions, including its acquisition of MyTukar in Malaysia and Beyond Cars in Hong Kong.

Examples in the list below include Sumitomo Insurance’s acquisition of Singlife (pan-Asia expansion), as well as OnPoint’s acquisition of Crea (Southeast Asia expansion).

(3) License to operate

An adjacent driver to (2) is the acquirer (or in some cases, the acquiree) seeking a license to operate in new markets or unlock access to regulated business.

We often see this with fintechs that are able to expand into stock brokerage products or insurance products or cross-border payment services by virtue of the appropriate licenses and registrations in a jurisdiction. Ajaib in Indonesia and Finhay in Vietnam acquired traditional securities brokerages to expand their services. Welab acquired a bank in Indonesia to launch in the market.

But this type of acquisition also applies to companies operating in industries where regulation may only be forming. We saw this most prominently with TikTok’s re-entry into Indonesia through its acquisition of Tokopedia.

(4) Private equity

While acquisitions have dominated exits, private equity buyouts of venture backed companies have not been as common until recently.

The challenges of the global economic landscape and its impact on liquidity in the public and private markets has opened up opportunities for PE firms to take on strategic acquisitions of (often distressed) venture-backed companies and reposition them for better growth.

EQT and CVC Capital are examples of PE firms have made notable acquisitions in Southeast Asia in the last two years.

Acquistions as long-term signals of industry maturity

Regardless of the type of acquisition and motivation, it is clear that:

- Acquisitions are a signal of increasing demand for end-to-end infrastructure and capabilities, from financial services/banking to renewable energy or chip manufacturing.

- Acquisitions reflect a demand for maintaining competitive advantages in digital transformation (this demand only grows with the “AI or Die” mindset being proliferated across corporate organizations)

- Inflationary environments have opened up opportunities for acquisitions in sectors where there is still high demand for products amidst rising prices, like healthcare.

- Acquisitions can potentially reflect short-term distress in a sector but also long-term optimism in economic fundamentals of a specific geography’s industry or market.

Top 10 Largest SEA Acquisitions from 2023-2024 Based on Acquiree’s Equity Funding

Tokopedia

| Total Equity Funding | $3.3B |

| Location | Indonesia |

| Founded Year | 2009 |

| Acquirer | Tiktok |

| Acquisition value | $1.5B |

Last December 2023, Tiktok acquired 75% of Tokopedia, worth over $1.5 billion. The transaction combines Tokopedia and TikTok Shop Indonesia’s businesses under the Tokopedia entity.

With this transaction, Tokopedia is now co-owned by Tiktok and the GoTo group. Despite TikTok having a controlling stake in the merged entity, GoTo will still earn revenue from an e-commerce service fee. TikTok will operate and maintain shopping features within its app in Indonesia, while GoTo will benefit from a sustainable revenue stream and avoid further funding obligations for Tokopedia (GoTo Press Release).

The partnership aims to leverage TikTok’s 125 million monthly active users in Indonesia to drive e-commerce growth, particularly in live commerce, while Tokopedia caters to affluent, intent-based buyers. The collaboration will expand Tiktok’s digital financial services through GoPay and Bank Jago, and delivery services via Gojek.

The deal also supports Indonesia’s MSMEs and digital economy, with initiatives like the Belanja Lokal campaign. This partnership positions the combined entity as a leading e-commerce player, enhancing the ecosystem of all the companies involved and driving long-term growth.

PropertyGuru Group

| Total Equity Funding | $690M |

| Location | Singapore |

| Founded Year | 2006 |

| Acquirer | EQT |

| Acquisition Value | $1.1B |

EQT Private Capital Asia and PropertyGuru announced the completion of PropertyGuru’s acquisition by BPEA Private Equity Fund VIII on December 13, 2024, at USD 6.70 per share, valuing the company at approximately USD 1.1 billion (PropertyGuru).

Following the merger, PropertyGuru was delisted from the New York Stock Exchange and transitioned to a privately held entity. Unexercised warrants will be exchangeable for USD 0.7526 until January 12, 2025.

The acquisition aims to support PropertyGuru’s growth by leveraging EQT’s expertise in digital marketplaces and real estate classifieds. EQT plans to accelerate technology development, expand market reach, and improve operational efficiency, strengthening PropertyGuru’s position in Southeast Asia’s dynamic PropTech sector. This partnership aligns with regional trends like urbanization, middle-class expansion, and digitalization, driving innovation and market leadership.

AG&P

| Total Equity Funding | $453M |

| Location | Singapore |

| Founded Year | 1900 |

| Acquirer | EQT |

| Acquisition Value | $300M |

Nebula Energy LLC acquired a majority stake in AG&P LNG, a subsidiary of AG&P Group, through a $300 million investment. The transaction, announced on January 31, 2024, aims to accelerate the development of LNG terminals and downstream gas infrastructure in underserved and fast-growing markets across South and Southeast Asia.

AG&P LNG, which operates as an independent subsidiary of Nebula Energy, will focus on expanding its LNG infrastructure ecosystem, leveraging Nebula’s investment to bridge the gap between LNG supply and demand in emerging markets (AG&P Press Release).

The investment will support AG&P LNG’s growth pipeline, which includes six LNG terminal projects with a proposed capacity of 25 MTPA, including the Philippines LNG (PHLNG) Import Terminal. Nebula Energy’s involvement, led by Chairman Peter Gibson and CEO Sam Abdalla, will also include the establishment of Nebula Energy Shipping to provide efficient LNG transportation services.

This partnership positioned AG&P LNG as a key player in delivering cost-effective and reliable LNG solutions, addressing the increasing demand for clean energy in high-growth markets across Asia.

Singlife

| Total Equity Funding | $319M |

| Location | Singapore |

| Founded Year | 2014 |

| Acquirer | Sumitomo Life Insurance Company |

| Acquisition Value | Undisclosed |

Singlife became a fully owned subsidiary of Sumitomo Life Insurance Company following regulatory approvals in Singapore and Japan last December 22, 2023 (SingLife Press Release). This was on the back of the agreement to acquire TPG’s 35% stake for S$1.6b billion along with its earlier acquisition of Aviva plc’s stake.

The deal values Singlife at S$4.6 billion, making it one of the largest insurance transactions in Southeast Asia. The transaction followed Sumitomo Life’s earlier acquisition of Aviva plc’s stake in Singlife.

Sumitomo Life, which first invested in Singlife in 2019, views Singapore as a strategic hub for its Southeast Asia expansion. The acquisition aims to strengthen Sumitomo Life’s international business portfolio while maintaining Singlife’s current operations, brand, and management team.

Singlife, a leading Singapore-based insurer with S$14.4 billion in total assets as of December 2022, will benefit from Sumitomo Life’s capital and support to pursue growth in Singapore and the broader region. Both companies emphasize their shared commitment to customer-focused financial solutions and long-term growth in Southeast Asia.

U Mobile

| Total Equity Funding | $303M |

| Location | Malaysia |

| Founded Year | 1998 |

| Acquirer | Mawar Setia Sdn Bhd |

| Acquisition Value | undisclosed |

Singapore Technologies Telemedia (ST Telemedia), through its subsidiary Straits Mobile Investments, has entered into a conditional share purchase agreement to sell a majority stake in U Mobile to Malaysia’s Mawar Setia Sdn Bhd.

While the exact financial terms and the specific percentage of shares being sold were not disclosed, it was noted that upon completion of the transaction, ST Telemedia will retain approximately a 20% minority stake in U Mobile, resulting in U Mobile no longer being a subsidiary of ST Telemedia. The completion of this transaction is contingent upon regulatory approvals and is anticipated by the third quarter of 2025 (Reuters).

This strategic move aligns with U Mobile’s recent announcement to reduce its foreign shareholding to 20%, aiming to ensure greater Malaysian control and attract local investors. By divesting a majority stake to Mawar Setia, a Malaysian private limited company, U Mobile seeks to comply with national regulations that cap foreign ownership in telecommunications companies at 49%. This shift is also expected to facilitate the company’s plans for future growth and local market integration.

Siloam Hospitals

| Total Equity Funding | $165M |

| Location | Singapore |

| Founded Year | 1996 |

| Acquirer | CVC |

| Acquisition Value | ~$1.6B |

In August 2024, CVC Capital Partners, a Luxembourg-based private equity firm, acquired a majority (45% (Forbes) to 65% (DealstreetAsia), depending on the source stake in Indonesia’s Siloam International Hospitals from PT Lippo Karawaci Tbk for approximately $1 billion. Prior to this deal, CVC held a 26.18% stake in Siloam, making it the majority shareholder post-acquisition.

The acquisition aligns with CVC’s strategy to capitalize on the growing healthcare market in Southeast Asia. By increasing its stake in Siloam, CVC aims to leverage the hospital chain’s extensive network and reputation to meet the rising demand for quality healthcare services in Indonesia. For Lippo Karawaci, the divestment provides an opportunity to strengthen its balance sheet and focus on its core real estate operations.

Sun Cable

| Total Equity Funding | $153M |

| Location | Singapore |

| Founded Year | 2018 |

| Acquirer | Grok Ventures |

| Acquisition Value | undisclosed |

Australian billionaire Mike Cannon-Brookes, through his firm Grok Ventures, has acquired the $20 billion Sun Cable renewable energy project, with the transaction expected to close by July. While the sale value remains undisclosed, it will fully repay Sun Cable’s unsecured creditors.

The project includes the Australia-Asia PowerLink, a plan to transmit power from a 20-gigawatt solar farm in northern Australia to Singapore via a 4,200-kilometer undersea cable. Grok aims to advance the project, with Stage 1 targeting 0.9 gigawatts for Darwin and 1.8 gigawatts for Singapore (The Guardian).

Cannon-Brookes highlighted the project’s potential to position Australia as a renewable energy leader, calling it a “big step in the right direction.” Sun Cable collapsed in January due to funding disputes between its owners—Grok Ventures and Andrew Forrest’s Squadron Energy.

Forrest, skeptical of the PowerLink’s viability, opted not to bid, while infrastructure investor Quinbrook joined Grok’s consortium. The deal reflects Cannon-Brookes’ commitment to ambitious renewable energy initiatives despite significant challenges.

Chope

| Total Equity Funding | $50.4M |

| Location | Singapore |

| Founded Year | 2011 |

| Acquirer | Grab |

| Acquisition Value | undisclosed |

Grab, Southeast Asia’s leading ride-hailing and food delivery firm, has acquired Singaporean dining reservation platform Chope for an undisclosed sum, as confirmed by both companies. The deal aims to create synergies for Grab’s merchant-partners, particularly in capturing online-to-offline opportunities.

Grab emphasized its focus on supporting small and medium-sized businesses, which make up the majority of its platform and often lack the resources of larger brands. The acquisition was first reported by Business Times, citing an internal email (TechCrunch).

Chope, founded in 2011, operates in seven cities, including Singapore, Hong Kong, and Bangkok, with over 13,000 restaurants listed on its platform. Founder Arrif Ziaudeen stated that partnering with Grab aligns with Chope’s mission of connecting restaurants to diners and will help drive sustainable growth in a competitive market. The acquisition reflects Grab’s strategy to expand its ecosystem and strengthen its position in the food and dining sector.

Crea

| Total Equity Funding | $38.0M |

| Location | Thailand |

| Founded Year | 2019 |

| Acquirer | OnPoint |

| Acquisition Value | undisclosed |

OnPoint, Vietnam’s leading e-commerce enabler, has acquired CREA, a top e-commerce enabler in Thailand, as announced on December 18, 2024. This strategic partnership unites two industry leaders, creating a comprehensive ecosystem to support global and regional brands in Southeast Asia’s rapidly growing digital economy.

Together, OnPoint and CREA serve over 250 brands, supported by a workforce of 600+ employees and 1,000+ outsourced personnel specializing in warehousing, livestreaming, and end-to-end e-commerce operations.

The collaboration leverages advanced AI-driven tools for content creation, livestreaming, and personalized consumer engagement, enhancing operational efficiency and customer experiences (Crea Press Release).

The partnership aligns with the vision of both companies to become Southeast Asia’s leading e-commerce solutions providers over the next five years. OnPoint, backed by SeaTown Private Capital Master Fund, brings financial stability and technological expertise, while CREA contributes local market insights and operational excellence.

The combined entity aims to empower brands to thrive in Southeast Asia’s e-commerce market, which is projected to grow significantly, reaching a Gross Merchandise Value (GMV) of $370 billion by 2030. This acquisition marks a new era in e-commerce enablement, driven by innovation and a shared commitment to building a sustainable and inclusive digital ecosystem.

iPrice Group

| Total Equity Funding | $26.6M |

| Location | Malaysia |

| Founded Year | 2014 |

| Acquirer | Bukalapak |

| Acquisition Value | undisclosed |

Bukalapak, a leading Indonesian e-commerce company, has acquired a majority stake in iPrice Group, a price comparison platform, as part of its strategy to focus on niche marketplaces and accelerate growth. Founded in 2014, iPrice allows users to compare product prices, specifications, and seller feedback, and has raised approximately $26 million in funding.

Despite laying off 20% of its workforce in 2022 due to economic challenges, iPrice will continue to operate independently post-acquisition, with plans to expand into the gaming sector and enter the Australian market (Tech in Asia).

The partnership aims to help iPrice reach more consumers and offer enhanced deals and discounts across new categories and regions. Additionally, iPrice intends to support Bukalapak’s goal of achieving profitability in 2023.

Bukalapak views the acquisition as a strategic move to strengthen its position in the e-commerce landscape which underscores both companies’ commitment to sustainable growth and move towards profitability in the competitive digital marketplace.

Takeaways

The recent wave of acquisitions in Southeast Asia reflects a dynamic and maturing market where consolidation and strategic investments are reshaping key industries.

- One clear trend is the consolidation of the financial sector, with major players acquiring or increasing their stakes in fintech, insurance, and real estate platforms. This signals a push toward building stronger, more integrated financial ecosystems that can serve the region’s growing middle class and expanding digital economy.

- Additionally, the surge in technology-driven acquisitions highlights the increasing competition for dominance in e-commerce, digital services, and cybersecurity, as companies seek to leverage AI, data protection, and online marketplaces to scale their operations. Investors are betting on Southeast Asia’s rising digital adoption and urbanization, recognizing the region’s potential for long-term growth in tech-enabled sectors.

- Beyond finance and technology, acquisitions in renewable energy and healthcare demonstrate a strategic pivot toward sustainability and long-term resilience. The growing investment in clean energy infrastructure and LNG projects suggests that Southeast Asia is positioning itself as a future leader in the global energy transition, with governments and private players aligning efforts to address energy security concerns.

- Similarly, healthcare acquisitions reflect increasing investor confidence in the sector’s profitability and long-term demand, as improving healthcare access becomes a priority in developing economies.

Overall, these acquisitions highlight a broader shift in Southeast Asia’s business landscape, where capital is flowing into industries that promise scalability, digital transformation, and sustainable growth, setting the stage for deeper market integration and economic expansion in the years to come.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.