Southeast Asia’s e-commerce story isn’t just about Shopee, Lazada, and Tokopedia anymore. While these platforms dominate headlines with their 84% market share, the real transformation is happening in the spaces between—and that’s where the biggest opportunities lie for founders.

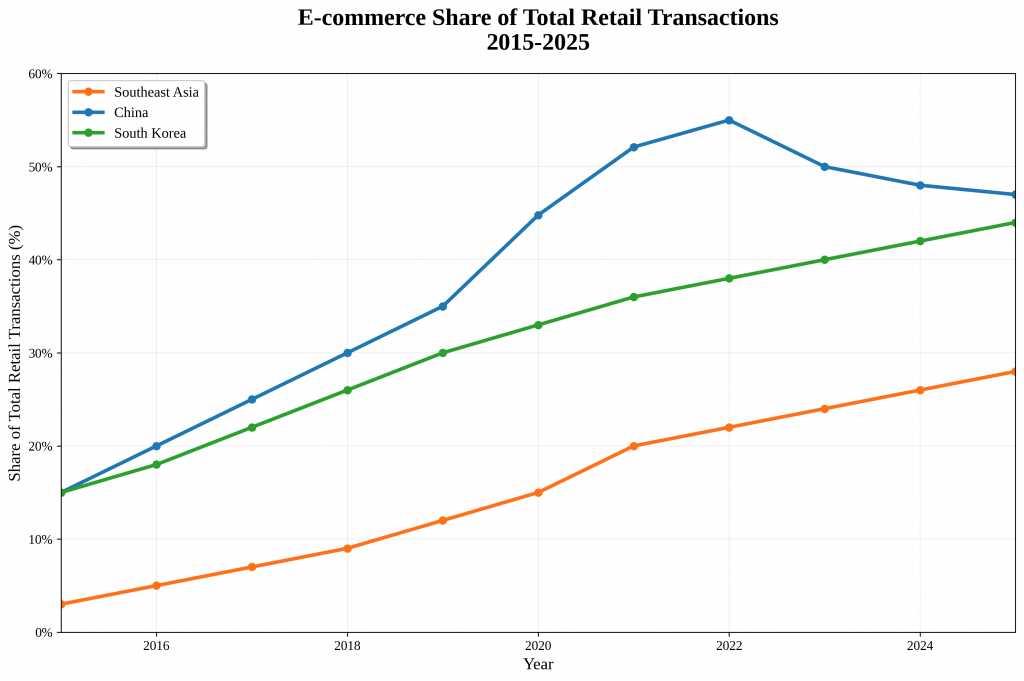

At 27% e-commerce penetration compared to China’s peak of 55% and South Korea’s 42%, Southeast Asia isn’t just catching up. It’s creating entirely new models of retail that work for its unique market dynamics. The question isn’t whether you can compete with the giants—it’s whether you understand the transformation they’re enabling.

The Numbers Tell a Different Story

The latest data from Bernstein Research, KOSTAT, and Nowak & Partner shows Southeast Asia’s e-commerce penetration trailing significantly behind mature markets. But this isn’t a story about being late to the party. It’s about a fundamentally different party altogether.

China’s e-commerce market peaked at 55% penetration in 2022 and has since entered what researchers call a “stabilization phase” with slight decline. South Korea, with its advanced digital infrastructure, sits at 42% penetration by 2024, projected to reach 44% by 2025.

Southeast Asia’s 27% penetration by 2025 represents something more interesting: a market where 73% of retail transactions still happen offline, creating massive room for hybrid models, social commerce, and direct-to-consumer brands that don’t exist anywhere else.

Beyond Platform Dominance: The Real Transformation

While Shopee, TikTok Shop, and Lazada control 84% of the region’s e-commerce market, the most interesting growth is happening in the remaining 16%—and in the 73% of retail that’s still offline.

Take Tentang Anak, one of Insignia Ventures Partners’ portfolio companies. Founded by pediatrician Dr. Mesty Ariotedjo and former Tokopedia executive Garri Juanda, they turned a massive social media following into top-selling brands for Vitamin D gummies and skincare products reaching more than 3 million children across Indonesia.

Their approach? Start with education, build trust through expertise, then create products that solve real problems. Their app has over a million downloads with a near-perfect 5.0 rating—all organic growth, no advertising. They’ve been profitable since mid-2024, not by competing on price with the platforms, but by creating what Garri calls “products that have a positive impact on children’s daily needs.”

This isn’t marketplace arbitrage. This is retail transformation.

The Social Commerce Revolution

The data shows social commerce revenue in Southeast Asia is expected to reach $116.50 billion in 2024, with live commerce driving real-time interaction between brands and consumers. TikTok Shop’s emergence as the region’s #2 platform demonstrates how social-first features are reshaping the entire landscape.

But the real opportunity isn’t in competing with TikTok Shop—it’s in understanding what TikTok Shop represents: the convergence of content, commerce, and community. This is where companies like Aloshop are thriving.

Aloshop, through Shipper and another Insignia portfolio company, has become a standout performer in Thailand’s TikTok Shop ecosystem. In July 2024, they achieved First Place in the Lifestyle Brand Content GMV TSP Cluster Champion Category and secured Rank 2 for Highest GMV Brand on TikTok Shop Thailand. Their success demonstrates how e-commerce enablers can help brands master the social commerce revolution without having to build the infrastructure themselves.

The Counter-Intuitive Omnichannel Opportunity

Perhaps the most interesting transformation is happening with companies that are using online success to build offline presence—the reverse of traditional retail evolution.

Konvy, Thailand’s leading beauty e-commerce platform and another Insignia portfolio company, exemplifies this counter-intuitive approach. After establishing dominance online and raising $11 million to expand regionally, they’re now leveraging their digital success to develop an offline store network in major shopping malls including Central, The Mall, and Paragon.

This isn’t just about adding physical touchpoints—it’s about creating an integrated experience where online data informs offline strategy, and offline experiences drive online engagement. Konvy’s omnichannel approach recognizes that in Southeast Asia’s retail landscape, the 73% of transactions that happen offline aren’t going away—they’re going to integrate with online in ways that create entirely new customer experiences.

The E-commerce Enabler Ecosystem

The infrastructure layer is perhaps the most overlooked part of Southeast Asia’s retail transformation. Companies like Aloshop are building the rails that enable brands to succeed across multiple channels, from traditional e-commerce platforms to emerging social commerce channels.

Aloshop operates 300+ warehouses across Indonesia and Thailand, providing the logistics backbone that allows smaller brands to compete with larger players. But their real value isn’t just in warehousing—it’s in understanding how to optimize performance across different platforms. Their success on TikTok Shop Thailand demonstrates how enablers can help brands navigate the complexity of social commerce while maintaining operational efficiency.

This enabler ecosystem is what makes Southeast Asia’s 27% penetration so different from China’s early days. The infrastructure exists. The payment systems work. The logistics networks are established. What’s missing isn’t infrastructure—it’s brands that understand how to use it.

The D2C Opportunity in a Platform-Dominated World

Direct-to-consumer brands in Southeast Asia face a unique challenge: how do you build direct relationships with customers in markets where platforms dominate discovery and transaction?

The answer isn’t to avoid platforms—it’s to use them as customer acquisition channels while building owned relationships. Tentang Anak’s model is instructive: they use their app as the relationship layer while selling through multiple channels. Their books, skincare products, and educational content create touchpoints that platforms can’t replicate.

This hybrid approach—platform distribution with owned customer relationships—represents a new model that’s uniquely suited to Southeast Asia’s market dynamics.

The Mobile-First Advantage

Unlike China or South Korea, where e-commerce evolved from desktop to mobile, Southeast Asia went mobile-first from the beginning. This creates opportunities for experiences that simply don’t exist in more mature markets.

Social commerce, live streaming, and in-app purchasing aren’t add-ons to existing e-commerce infrastructure—they’re the foundation. Brands that understand this can create experiences that feel native to how Southeast Asian consumers actually shop.

The Founder’s Playbook for Retail Transformation

Build for the infrastructure that exists, not the infrastructure you want. Payment systems, logistics networks, and platform APIs are already established. Your job is to create value on top of them, not rebuild them.

Think omnichannel from day one. The 73% of retail that’s still offline isn’t going away—it’s going to integrate with online. Brands like Konvy that can bridge physical and digital experiences have sustainable advantages.

Focus on owned customer relationships. Platforms are great for discovery and transaction, but terrible for building long-term customer value. Use platforms to acquire customers, then create direct touchpoints that platforms can’t replicate.

Understand social commerce as infrastructure, not marketing. Social features aren’t promotional tools—they’re transaction infrastructure. Build them into your core product experience, not as an afterthought.

Create what’s needed, not what’s trending. As Tentang Anak’s founders put it, “Create what is needed, not what is trending.” The biggest opportunities are in solving real problems, not chasing platform features.

The Reality of Retail Transformation

Southeast Asia’s retail transformation isn’t about replacing traditional e-commerce platforms—it’s about building on top of and around them. The 27% e-commerce penetration isn’t a limitation; it’s a feature.

In markets where 73% of retail still happens offline, the opportunity isn’t to digitize everything. It’s to create hybrid experiences that work for how people actually live and shop in Southeast Asia.

The companies that succeed won’t be those that copy what worked in China or the US. They’ll be those that understand Southeast Asia’s unique combination of mobile-first infrastructure, social commerce adoption, and hybrid retail preferences.

The retail transformation is happening right now. The question isn’t whether you can compete with the platforms—it’s whether you can build something the platforms enable but can’t replicate.

The opportunity is massive. The infrastructure is ready. The only question is whether you’re building for the transformation that’s actually happening.

Data sources: Bernstein Research (2025), KOSTAT Monthly Online Shopping Survey, Nowak & Partner (2023), PCMI E-commerce Data Library (2024), Momentum Works Ecommerce in Southeast Asia 2025, Insignia Business Review

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.