Excerpts included from interview with Wall Street Journal on Chinese tech turning to financial services

Chinese influence in the region traces centuries back to sampans and Chinese junks making their way across rivers and seas to trade with locals, and later on the rest of the world that made Southeast Asia their trading outpost with the Middle Kingdom. The world’s oldest Chinatown can be found in Manila, a historical signpost for just how entrenched China has been in the region and how valuable the region has been for spreading Chinese influence globally.

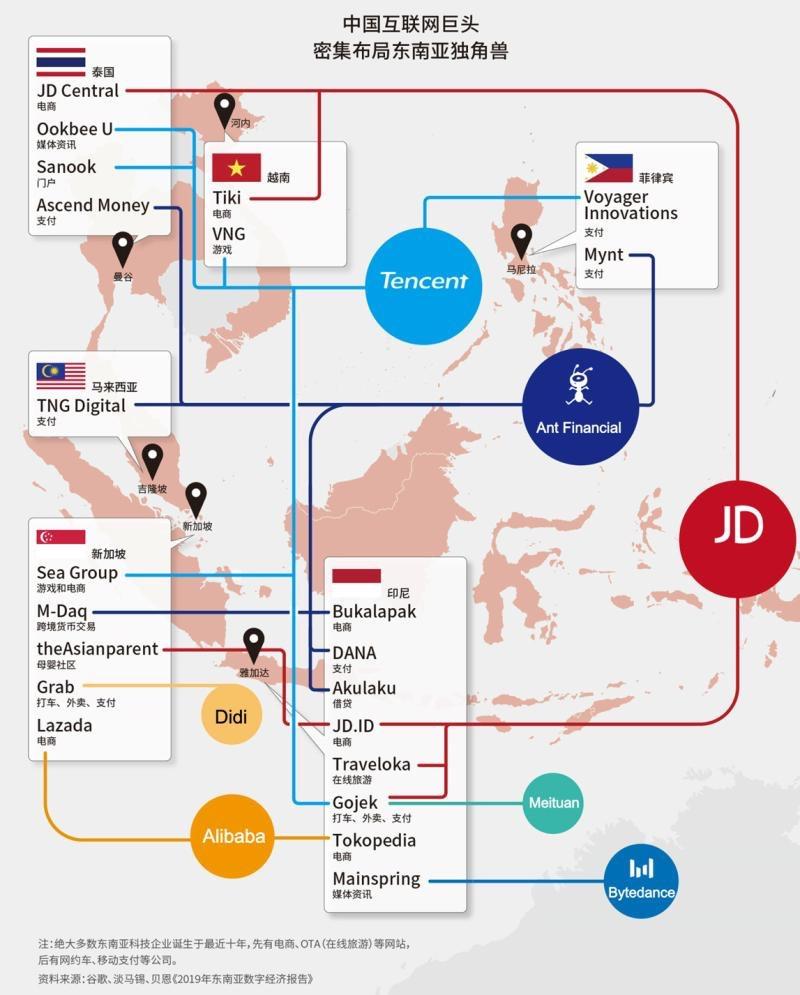

Digital merchants

This past decade has simply been an evolution of this dynamic in the digital age. When China became a tech powerhouse it made sense for the winners to take their technology and talent where their forebears took their spices and sails several centuries ago.

Apart from the geographical and even cultural proximity, China tech’s huge splash in the region can largely be owed to their overall investment approach, which did not just involve watering companies with cash, but cultivating their growth with talent (ie training), technology (eg 5G), and expertise.

Alibaba and Tencent set the precedent in this regard for the companies that followed, albeit to varying degrees. While Alibaba is known to have deployed talent and infrastructure, Tencent’s involvement remains largely in the boardroom and on the cap tables of their investments.

They also seem to have different approaches in terms of verticals, with Alibaba sticking to ecommerce with Lazada and Tokopedia. Meanwhile, Tencent is inclined more towards the content and gaming ecosystem with investments into Sea, Ookbee and Go-jek, given its dependence on the messaging superapp WeChat for scale. Another model for expansion into the region is JD’s where they did a joint venture with Go-jek and Traveloka to setup JD.ID, which is now reported to have joined Indonesia’s unicorn club.

Hands-on approach to the market

This hands-on ability stems from investors seeing the region’s digital transformation as almost mirroring that of China’s nearly a decade ago, only this time going at a faster pace with better technology and more sources of capital. Indonesia, for example, is currently viewed as being at the inflection point where China was when Alibaba’s Taobao took off. The business models that succeeded in China, with their strength in generating user stickiness at low cost, are also proving to be crucial to expansion in Southeast Asia’s fragmented landscape.

The recent slew of startups hitting the brakes on the public markets has certainly pushed tech investors globally to reevaluate their positions and become more scrutinous when it comes to profitability and quality overall, and Chinese tech investors are no different.

Even then, their moves in the region have not abated and are becoming more focused on securing stronger positions in the region and supporting the path to profitability for local investments. Instead of the pure investments and joint ventures which have characterized most of China tech’s activity in the region in latter half of the decade, Chinese tech companies will strengthen their ground up initiatives in the region, with Ant Financial, Xiaomi, and even Tencent (through Sea) joining the digital banking race, Ping An launching telehealth consulting services in Indonesia with Grab, and JD launching a mobile wallet in Thailand with Central Group.

Where the China’s biggest digital merchants have set up shop in Southeast Asia. Taken from https://www.linkedin.com/posts/carlos-y-2ba58a171_sea-is-a-huge-playground-for-chinese-tech-activity-6619148553300336640-57u6

A closer look: setting up fintech moats around the region

Chinese tech unicorns are leveraging on the ubiquity of financial services to compete in the region, taking advantage of their massive user base and gain penetration across different markets. Finance is a foundational vertical for tech companies in Southeast Asia, where most of the region’s population is unbanked or has difficulty with financing. Enabling access to financial services opens up opportunities to tap into other verticals, like ecommerce and logistics.

Many of these tech giants also have a high number of active users and traffic – personal finance allows them to monetise these users effectively, and also in the process, collect transaction data that underwrites many financial services. Tencent and Alibaba have already shown how tapping into a financial services platform play, whether by acquiring local players or setting up subsidiaries, has enabled them to extend their reach into regions like Southeast Asia and Africa.

The stiff competition in China’s fintech sector is pushing tech companies to tap into the growing opportunity in Southeast Asia for financial services, where the majority of the online population transact heavily on ecommerce and ride hailing. It also helps that financial services in the region serves both as a strong moat from which to expand into other offerings and an expansion strategy for platforms with already deep market share.

Apart from Singapore where the digital banking race is afoot, markets like Malaysia, Thailand, and the Philippines are becoming more open and structured in terms of financial services regulation and bank partnerships with tech companies.

Another key motivation is expansion. The best offense begins with setting up good defense. Covering financial services entrenches their position in the market, creating stickiness with existing customers. This lays the foundation to expand into new markets and across more services. Integrating financial services won’t necessarily ensure profitability, but done right, can result in better unit economics and create more breathing space for these giants to grow.

Coming into the region, the tech platforms have traffic, data, often superior artificial intelligence / machine learning capacity and cloud computing capabilities. They often also have a more acute sense of the user when it comes to engineering retention on their platforms. However, what they lack is often the regulatory license, low funding cost, risk management capabilities, product offerings and in certain cases like private banking, personalised services.

When it comes to regions like Southeast Asia, regulations vary with each country, and this can be a hurdle for platforms seeking to tap into finance. Some markets can be proactive with their regulations (like Hong Kong and Singapore which is issuing virtual banking licenses), while others tend to wait for players to make more considerable moves before stepping in.

With the variability across markets, the key for tech platforms venturing into finance is to form the right partnerships with local banks and financing institutions. These partnerships won’t only get a foot in the door, but also set a defensible moat for these platforms should competitors follow.

Settling in means long-term opportunities for local founders

A combination of local competition, pushback from other markets, and the raw market potential will continue to attract Chinese investment into Southeast Asia. With the market uncertainties and tension across the Pacific heightened, the relatively China-friendly regulation in Southeast Asia stands more favorably versus the pushback companies like Huawei and Bytedance have received in the West. The trade war has also resulted in supply chain diversification driving manufacturing growth in insular countries like Vietnam, which will only serve to make the region an even more attractive destination for Chinese investment.

What differentiates the impact of Chinese investment from the rest of the world’s in the region is that it has gone well beyond capital and the play for these big tech companies is long-term. For local founders, opportunities abound to leverage on China tech not just for investments but long-term infrastructure plays as well. The question is who to partner with and which platforms will benefit your business model. This degree of influence has played a huge role in accelerating the region’s digital transformation thus far and will continue to do so in the next decade.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.