Over the past decade, fintechs have been making great strides in Southeast Asia, revolutionizing banking in the region. These moves have reached a new high this year with digital banking license applicants hitting the races, consumers looking for more convenient digital alternatives in a contactless world, and tech majors in the region building out their fintech stack to unlock the next stage of growth.

This fintech revolution has forced banks and other financial incumbents to find ways to turn threat into opportunity, whether it be building their own fintech apps, opening up their APIs for fintechs to integrate, or partnering with tech companies to launch new services.

Regardless of the strategy, it is clear that the path to success in the finance industry is not a solo flight. A lone wolf strategy in a red ocean is costly and will not entirely be beneficial for the consumers. Collaboration will be necessary at one point or another for both incumbents and fintechs. And for these partnerships to work, it takes two (at least).

Last Tuesday (15 September 2020), our managing partner Yinglan Tan shared his thoughts on bank and fintech partnerships in a panel hosted by MoneyLive APAC with prominent banking leaders in the region including HSBC’s Jen Flowers, Standard Chartered’s Marnix Zwart, and Krungsri Finnovate’s Sam Tanskul. Insignia Business Review took down notes from the session, and here are our key takeaways:

Key Takeaways from MoneyLive APAC talks

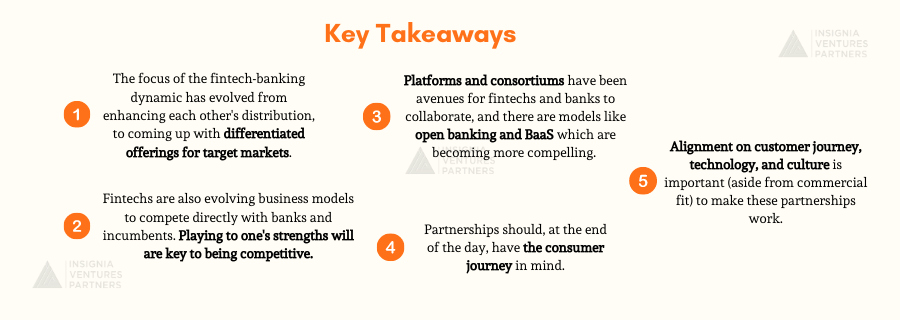

(1) The dynamic of fintechs and banks are going beyond enhancing each other’s distribution to creating differentiated products and services for the digital economy.

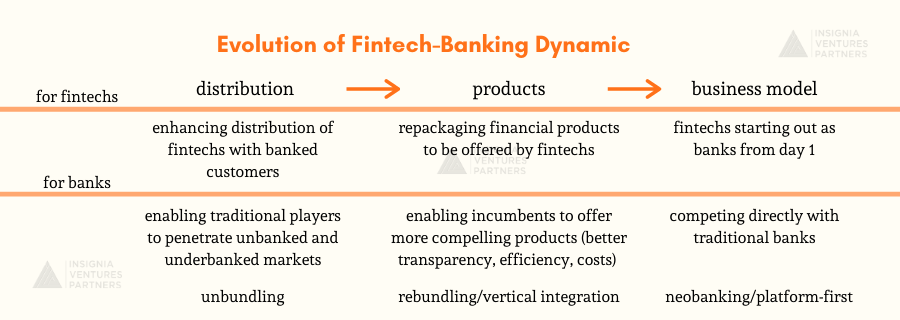

Over the years there has been an evolution in terms of the motivation behind bank-fintech partnerships. Initially, as fintech unbundled bank offerings, these partnerships served to enhance the distribution of fintechs and help them gain a wider user base and stronger retention, especially for banked customers. Since fintechs were targeting specific financial services and isolated use cases, they still needed to link with banks that had ownership of the customers’ accounts.

As fintechs moved into the unbanked and underbanked sector, partnerships with banks or financial institutions enhanced the distribution of these incumbents to penetrate a market that has been traditionally been difficult to penetrate alone. For example, AwanTunai has been developing ways to bridge the gap between financing institutions and underserved MSMEs that need capital.

As fintechs look to capture user accounts and entire verticals, the dynamic is going beyond enhancing the reach of either party and towards repackaging products and services for the specific target market of the fintech. In Indonesia, wealth management platform Ajaib recently acquired a stock brokerage firm to be able to provide digital stock investing services to their users.

And as these fintechs evolve to become neobanks and more digital-only banks are set up in Southeast Asia, we can expect more direct competition between fintechs and traditional banks that are also trying to catch up with digitalization.

Listen to Southeast Asia’s first digital-only bank tonik CEO and founder Greg Krasnov >>>

“To compete with traditional players, fintechs will have to rely on their core advantage as a technology company — user experience, transparency, speed — while at the same time building up key relationships with regulators and filling in roles with banking expertise,” says Yinglan.

How fintech banking partnerships are evolving

Our principal Samir Chaibi writes about why fintechs are shifting towards platform-first models >>>

(2) Banks are becoming more involved in banking-fintech partnerships, but the fundamentals remain the same: building for the consumer/customer.

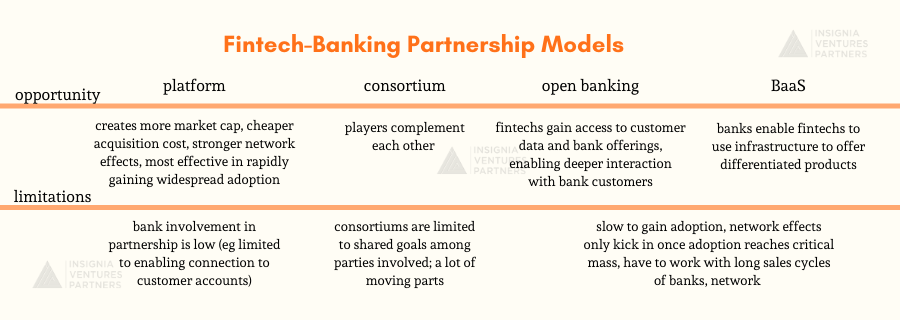

Now there’s more than one type of approach to partnerships for banks to consider. There’s the platform approach, where fintechs bridge or improve access between traditional players and customers. The level of partnership involved here is not as deep as the other approaches, but are still crucial for both parties. According to Yinglan, platforms create more market cap, have cheaper user acquisition costs, greater network effects, and have proven to be the most successful in gaining widespread adoption.

Other approaches see more hands-on involvement from banks, like consortiums, where a single player works with others to fill in each other’s gaps to offer a better proposition for their customers. We see this in the consortiums that have formed in Singapore’s digital banking race.

Then there’s open banking and banking-as-a-service (BaaS). In open banking, banks open up their APIs for fintechs to tap into bank data of existing customers and existing service offerings, whereas in BaaS, banks enable their functionality to be used by other players to reach entirely new customers.

According to Yinglan, these approaches are slow to get adoption, and the network effects only kick in once adoption has reached a critical mass. He also points out that it has traditionally been challenging with the sales cycles of banks to get open banking on the road.

The other panelists say however that that is changing.

According to Jen Flowers, it’s high time for the market to prove open banking and BaaS as compelling models for banks and fintechs to work together.

For Marnix Zwart, it’s all about betting on all angles as it is too soon to tell what approach is the winning approach. Diversification will be key to staying relevant in the space, and Standard Chartered has been active across these various approaches.

Sam Tanskul is excited about BaaS as a way for banks to power the financial back end of big tech platforms and cites Krungsri’s project with Grab.

Regardless of the approach, Jen says it’s important to consider the consumer lens — “are we addressing the new needs of the customer in this pandemic world?”

“Most banks right now like DBS and big banks in Thailand are turning to digital banking to [meet] customer expectations…banks [themselves] will have capabilities, but [the question is] how to make processes lean and reduce costs,” says Sam Tanskul from Krungsri Finnovate.

And regardless of the bank’s decision, time is of the essence during this period and the ability to pivot is important. Jen adds, “Consumers will remember who was there for them [during this time].”

Fintech-Banking Partnership Models

(3) There must be alignment for these partnerships to work — on the customer’s needs, the technology, and culture.

When it comes to making these partnerships work, the customer should still be at the core. Jen points out that there must be a “mutual understanding of where the customer is.” It’s important to “understand the end-to-end journey, [and] not just where to push products.” These partnerships are long-term plays and require constant communication and testing.

For Marnix, these partnerships should focus on relevant products, and using the right kind of technology is very important.

For Sam, it’s all about having “a minimum loss on product”. Banks should manage their expectations on the results of these partnerships and set the bar for costs that can be borne by the company.

According to Yinglan, these partnerships should be taken step-by-step and not be entered into hastily. There must also be a cultural fit, not just commercial fit, especially as fintechs and banks will often have polar opposite cultures and organizational structures. And this alignment starts at the top; if leadership is aligned, the rest will easily follow.

“It’s important that there’s cultural alignment on the onset [of these partnerships]…will the startup be able to work at the cadence of a larger, more hierarchical organization?

***

Even as the competition between fintechs and incumbents thickens, so do the kinds of partnerships between them. Success is not just coming out on top of the race, but being a proponent for a more open and connected industry that benefits its customers.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.