While 2021 was an opening of the floodgates when it comes to growth-stage funding and VC exits, 2022 has been less of a closing of these gates but rather an easing of the “flood” of capital, as investors, especially those in the growth-stage, have reeled from the price correction in the public tech markets.

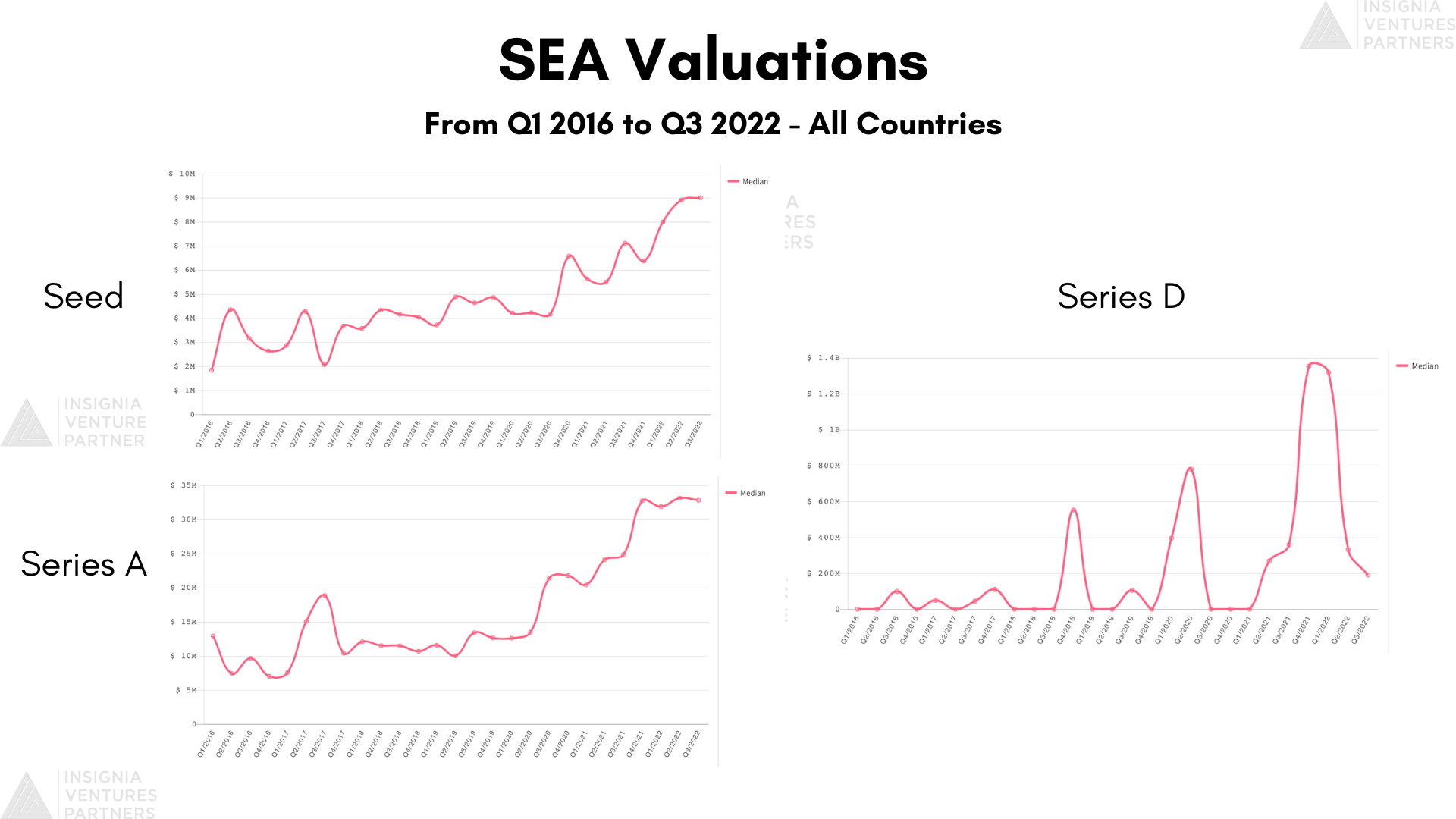

Comparing Seed, Series A, and Series D valuations from 2020 to 2022. Growth-stages have been hit harder but earlier stages have been more resilient with the influx of investors in these stages. Taken from https://www.insignia.vc/market-statistics.

In this article, we put together a list of insights on how 2022 has shaped up in terms of exit and funding pathways for venture-backed startups (#s 1-2), from growth-stage pipelines to M&As and secondaries as well as public market prospects. We also include insights on the impact these pathways have had on the way VCs find and invest in exitable companies.

- The shift in investor preferences is resulting in late-stage gaps and greater consolidation of capital in fewer companies.

- Greater confidence in Southeast Asia’s public market pathways but more preparation and patience expected leading up to IPOs.

- Bear markets are for building, even for VCs. Portfolio management plays an even greater role in differentiation and driving portfolio exits.

- A good beginning is half the journey toward an exit. More incentive to catalyze founder-market fit and back companies that are flipping prevailing wisdom on its head.

- Many more instruments are accessible to extend runways for startups but all are still best taken on top of good fundamentals.

(1) History echoes? Shift in investor preferences resulting in late-stage gaps and greater consolidation of capital in fewer companies

While buyer demand has been proven to be lucrative especially in Southeast Asia, it has been tempered by a flight to quality. And so for companies that meet this “quality” — profitable business models, audited financials, and mature corporate governance — the buyers are more likely to be easier to reach and engage.

We’re seeing somewhat of a reflection of what was happening in the early days of Southeast Asia’s venture capital value chain with momentum going towards a lot of early-stage activity with not as much late-stage activity to pick up on these companies as they scale. This time however the “gaps” in late stage are a result of the bear market rather than a lack of supply.

But there are key differences in SEA’s startup funding value chain today:

- The regional ecosystem does not necessarily have to be as dependent on foreign / global funds to fill in this gap. There are more local funds previously primarily targeting early-stage rounds may expand their appetite to growth stage through follow-on rounds or first tickets in these areas given the amount of dry powder and proven thesis around investing in the region

- There are also more local funds expanding into venture value chain like family offices

- There are more buyers, both corporates / strategics / fellow venture-backed startups and public market options for the more capital-efficient companies

While sights are set on Southeast Asia, the challenge is that thicker filters are being applied by these buyers when assessing opportunities. So rather than any significant long-term gaps in late-stage rounds, we will likely see more consolidation of capital in a smaller pool of companies in the late-stage with more earlier M&As.

With the rising cost of capital, consolidation is also likely to happen in terms of portfolio positions, which leads to more secondary sales. This momentum is not however simply a matter of speed or quantity but also of quality. Finding this balance is at the heart of the challenge for VC exits this year, where early-stage investors are seeking late-stage buyers in a capital-scarce market.

It continues to be in the best interest for Southeast Asia to have many inroads for talent and capital from anywhere in the world, from the US to China to Europe to the Middle East and South America. This is because Southeast Asia continues to be an appealing destination for innovation and entrepreneurship and the definitions of technology and business organization are becoming more borderless.

(2) Greater confidence in Southeast Asia’s public market pathways but more preparation and patience expected

That said, regardless of the current state of the public markets, early-stage venture capitalists will continue to optimize long-term for their companies to be acquired by the public markets. 2021 has opened up the proven optionalities for venture-backed companies to go public.

Even if 2022 has seen IPO plans being reconsidered or proceeding with more patience, there is a larger demand now than say five years ago for Southeast Asia-headquartered venture-backed tech companies.

This comes with platforms like Ajaib and Finhay making it easier for retail investors — typically the users of many of these tech companies — to invest in companies they are familiar with.

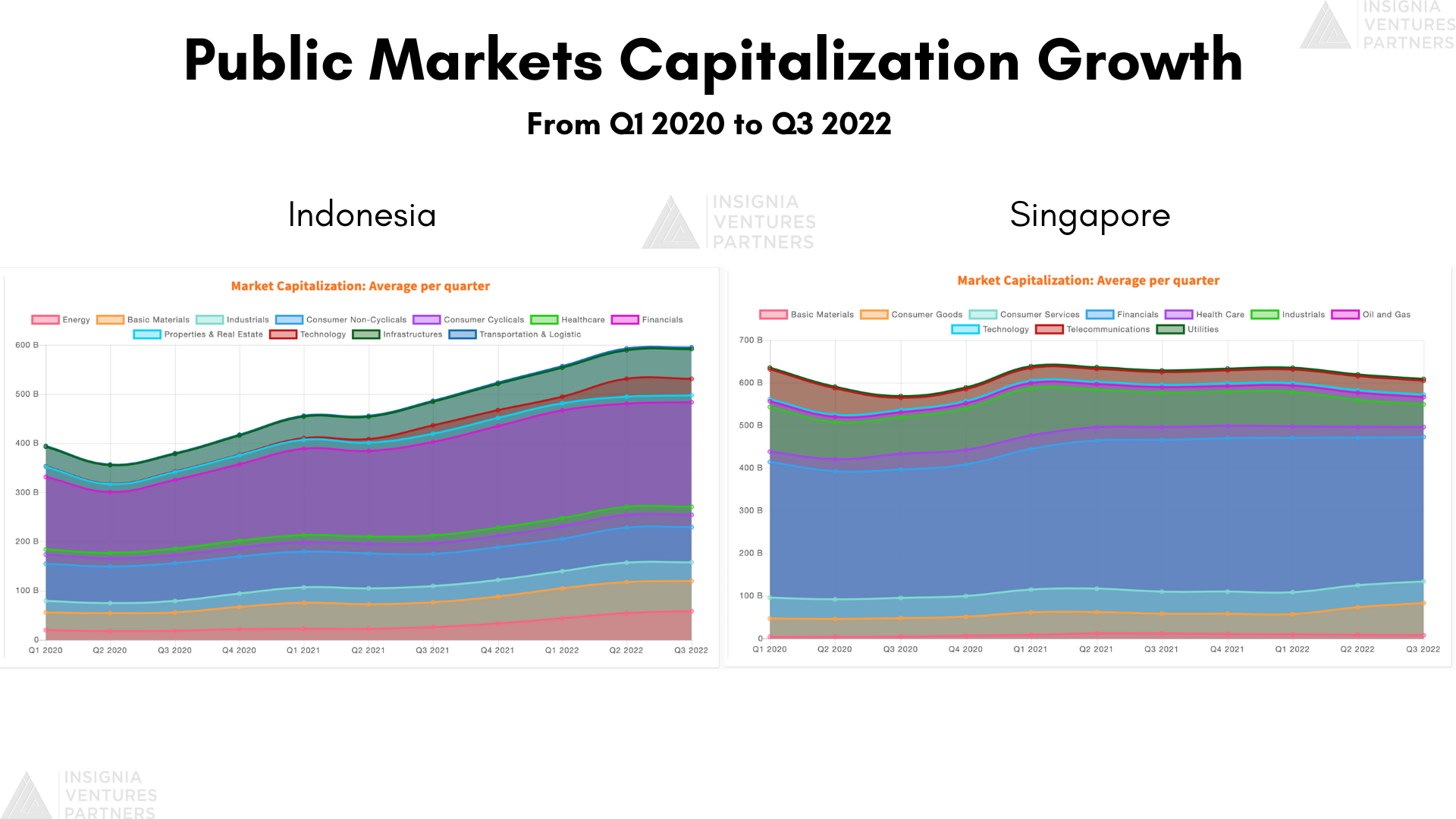

Comparing Indonesia and Singapore’s public market capitalization growth. Taken from https://www.insignia.vc/market-statistics.

(3) Bear markets are for building, even for VCs

Beyond the exits themselves, this year has also seen a greater focus on bringing portfolio companies up to shape for even better exit opportunities down the line, with bridge and follow-on rounds as well as operational support. Bear markets are for building, the saying goes, and VCs are also investing with this mindset. There is no hard and fast rule for VCs for timing exits. At the same time, there is increasing momentum for Southeast Asia’s tech markets to mature even further in terms of its exit landscape.

And because there is no hard and fast rule for timing, one way to look at the role of VCs is ensuring companies are ready when the right timing knocks on their door and the pieces fall into place for them. From hiring key management, introducing them to valuable investors, helping them with regulators, providing key insights to avoid pitfalls, there’s a lot to do, but foundational to any support is ensuring these companies are run by high-quality management. At the end of the day, growth is still driven by having the right people.

This level of support for portfolio companies post-investment is foundational for VC differentiation in the thickening Southeast Asia landscape. Differentiation goes beyond dry powder, though that can certainly go a long way in itself. Venture capital is increasingly platformized, connecting founders to various resources beyond capital. Technology will also be playing a greater role in terms of moving faster and gaining a more sophisticated baseline for outlier insights to emerge.

(4) A good beginning is half the journey towards an exit

Apart from building, venture capitalists can also be expected to adjust their sourcing and investment strategy. When it comes to finding, it may no longer be enough to look for founders who are raising. Ecosystem and community building are important to be readily accessible to founders even before they realize they are founders or even know what they want to build or even before they decide to raise their first round of venture funding.

Case in point: Super and Shipper

Counterintuitive finds are often the result of understanding the “norms” or prevailing wisdom and seeing it broken or flipped on its head on the ground through market data and observations (e.g. the value of the offline component in innovating or solving pain points in Southeast Asia’s logistics and commerce value chains, or dominance of simpler platforms over more complex applications in consumer-facing ecommerce).

Putting two and two together — differentiation will be defined by the combination of investment strategy and portfolio management approach, forming the ability of local firms to cycle through venture capital flywheel in the region.

(5) Many more instruments accessible to extend runways for startups but all are still best taken on top of good fundamentals

Similar to the advice passed around in the first half of 2020, it’s in the best interest of startups to be open to various channels of funding in a capital-scarce market. Today’s market demands creativity as founders may prefer to extend their runways with less dilutive forms of financing. The catch-22 is that many of these alternatives also have their own demands in terms of quality and assets that not all startups may be ready to present, for example, pure debt from banks requiring collateral.

This points to the reality that extending their runway, regardless of the source of capital, is ultimately a short-term initiative. Funding best works for businesses that already have that foundation of using capital efficiently, from company culture to a profitable business model, and these foundations are what many investors are now looking for in this market as well.

A note on convertible notes and venture debt

Convertible notes and venture debt have been around for a while. In Southeast Asia, the former has been an increasingly predominant instrument for startups to raise capital quickly and early on while bringing on board long-term partners. The latter has seen more use in recent years, especially amidst 2020’s initial impact in the pandemic. But both were designed for the venture-backed company; they have their roots in tying access capital to a company’s ability to raise further capital down the road and investor willingness to double down on the company.

In today’s environment, this implies that the company should be fit to raise in a capital-scarce market, which boils down any pursuit of funding to the fundamental question — is the business a sustainable one?

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.