This case study on AwanTunai was prepared as a basis for class discussion.

Copyright © 2025 by Insignia Press. No part of this publication may be reproduced, stored in a retrieval system, used in a spreadsheet, or transmitted in any form or by any means without permission.

Executive Summary

AwanTunai, an Indonesian fintech startup founded in 2017, has revolutionized the country’s FMCG supply chain by combining supply chain financing with enterprise resource planning (ERP) technology.

The company has maintained a laser focus on providing inventory purchase financing to MSMEs in Indonesia’s FMCG sector, which has served them well through the COVID-19 pandemic and beyond.

By pairing their financing product with their proprietary ERP solution, AwanTunai has been able to capture valuable transaction data that allows them to accurately assess creditworthiness even when traditional financial indicators are unreliable.

This case study examines AwanTunai’s journey from its founding through the challenges of the pandemic and into its current growth phase.

It explores the strategic dilemma facing the company as a venture-backed startup: Is concentrating solely on what they have refined and developed sufficient to deliver the growth and returns expected by their investors?

At what point should they consider expanding into new products or adjacent markets? What capabilities, resources, and strategic shifts would be required to do so successfully without compromising their core strengths?

Introduction and Problem Statement

Jakarta, March 2020

Editor’s Note: This segment is a scenario derived from conversations with AwanTunai management and not true to life. It is merely used for illustrative and educational purposes.

Dino Setiawan, co-founder of AwanTunai

Dino Setiawan stared at the dashboard on his laptop, the numbers reflecting the rapidly deteriorating economic situation across Indonesia. As CEO of AwanTunai, a fintech startup focused on supply chain financing for micro, small, and medium enterprises (MSMEs), he was watching the COVID-19 pandemic unfold with a mixture of concern and determination.

“We’re seeing recovery rates crash across the industry,” reported his team. “Most lenders are experiencing NPLs of 20-30%. The government is implementing loan moratoriums, but that’s just delaying the inevitable for many players.”

Dino nodded, his mind racing through potential scenarios. In the three years since founding AwanTunai with Rama Notowidigdo and Windy Natriavi, they had built a promising business providing inventory purchase financing to MSMEs in Indonesia’s massive fast-moving consumer goods (FMCG) sector. Now, that business model was facing its greatest test.

“What’s our exposure?” Dino asked.

“We’re in a better position than most,” his team explained. “Our focus on FMCG means our borrowers are still operating—people need to eat, even during lockdowns. But the supply chain is under enormous pressure. Wholesalers are struggling with cash flow, and micro-merchants are seeing volatile demand patterns.”

As Dino contemplated their next moves, he reflected on the journey that had brought them here. After 12 years in investment banking, with his last position as VP of Investment Banking at Morgan Stanley, he had returned to Asia from Silicon Valley to tackle the profound challenge of financial exclusion in Indonesia. The vision was clear: digitize Indonesia’s traditional supply chain and provide affordable financing to the millions of MSMEs that formed the backbone of the economy but remained underserved by conventional banks.

“We’ve always been data-driven,” Dino thought to himself. “My opinion as CEO doesn’t count unless it’s backed up by field data. That discipline has to guide us now more than ever.” (Setiawan, 2020)

What set AwanTunai apart from other fintech lenders was their strategic focus on the FMCG supply chain and their proprietary ERP product that complemented their financing solutions.

This dual approach would prove critical in the months ahead, as Dino later reflected: “Our focus on FMCG and the quick pairing of our financing with our proprietary ERP product was instrumental in mitigating the widespread pressure on NPLs during the pandemic. While the industry average NPL rate soared to 20-30%, we maintained a remarkable 3% NPL rate.”

Industry Background

In the sprawling archipelago of Indonesia, a nation of over 270 million people, the fast-moving consumer goods (FMCG) sector represented a massive US$100 billion market opportunity. Yet beneath this impressive figure lay a complex ecosystem plagued by inefficiencies, particularly in the traditional trade channels that dominated the landscape.

Over 66 million micro, small, and medium enterprises (MSMEs) formed the backbone of Indonesia’s economy, with more than 90% of the workforce being self-employed or operating within these enterprises. These businesses faced persistent challenges that had remained largely unchanged for decades: limited access to affordable financing, inefficient inventory management, paper-based record-keeping, and fragmented supply chains.

The traditional FMCG supply chain in Indonesia operated through multiple layers from manufacturers to distributors, wholesalers, and finally to the millions of small retailers and warung (small family-owned businesses) that served end consumers.

At each stage of this chain, businesses struggled with working capital constraints, lack of technological infrastructure, and information asymmetry. Banks and traditional financial institutions had historically viewed these MSMEs as high-risk borrowers, resulting in severe underbanking across the sector. When financing was available, it often came with prohibitively high interest rates, stringent collateral requirements, and cumbersome application processes.

The consequences of these challenges were far-reaching. Without adequate working capital, MSMEs could not optimize their inventory levels, leading to stockouts or excess inventory that tied up precious capital.

The lack of digital tools for transaction recording and inventory management resulted in inefficient operations and limited visibility into business performance. Meanwhile, suppliers struggled to expand their distribution networks due to the high costs and risks associated with serving small, fragmented retailers.

The COVID-19 pandemic further exacerbated these challenges. As lockdowns and movement restrictions were implemented, traditional businesses faced unprecedented disruptions. Recovery rates crashed and non-performing loans (NPLs) skyrocketed across the industry, with many lenders experiencing NPL rates of 20-30%.

Government-sponsored interest and loan moratoriums provided temporary relief but did not address the fundamental issues. The pandemic highlighted the urgent need for digitalization and financial inclusion in this critical sector.

Indonesian MSME. From AwanTunai website

Company Background

AwanTunai, an Indonesian fintech startup, approached these complex challenges by developing an innovative model that combined supply chain financing with enterprise resource planning (ERP) technology.

Founded in 2017 by a team with deep expertise in banking, technology, and operations, AwanTunai set out to revolutionize Indonesia’s FMCG supply chain by digitizing wholesaler operations and providing micro-merchants with affordable inventory purchase financing and integrated online ordering.

Since its founding, AwanTunai has maintained a laser focus on supply chain financing for MSMEs in Indonesia’s FMCG sector. As CFO Shilpa Gautam explained, “We’re a simple lender. We’ve got one product, which is inventory purchase financing, and we lend to the FMCG space.”

This disciplined approach served the company well, particularly during the pandemic when their deep understanding of the market and strong risk management capabilities enabled them to mitigate risks effectively while competitors struggled.

What proved critical to AwanTunai’s resilience during this period was their contrarian philosophy of “solving for risk before solving for scale” and their strategic decision to pair their financing product with their proprietary ERP solution.

By installing their ERP system at wholesalers, AwanTunai captured valuable transaction data that allowed them to accurately assess creditworthiness even when traditional financial indicators were unreliable. This approach enabled them to maintain a remarkably low NPL rate of just 3% during the pandemic—a time when the industry average soared to 20-30%—while simultaneously growing their revenue by 600%.

“The value of solving risk before scale,” noted Gautam, “has been through our proprietary ERP solution capturing alternative sources of data to underwrite loans.” This integration of financing with technology not only protected AwanTunai from the widespread pressure on NPLs during the crisis but also positioned them for significant growth afterward. Their focused strategy attracted significant venture capital and debt financing, with the company raising over $177 million across multiple funding rounds.

The Strategic Dilemma

However, this focused approach raised a critical strategic question for AwanTunai as a venture-backed startup: Was concentrating solely on what they had refined and developed sufficient to deliver the growth and returns expected by their investors? At what point should they consider expanding into new products or adjacent markets? What capabilities, resources, and strategic shifts would be required to do so successfully without compromising their core strengths? The tension between deepening their current market position and pursuing broader opportunities represented a classic strategic dilemma for successful startups that had achieved product-market fit in a specific niche.

“We stayed true to the vision, knowing deep down that we should start solving the problems,” reflected Dino. “And we certainly applied a disciplined approach to resolving the risk problems. Now we’re best-in-class in terms of risk management. In terms of lending capital, it’s now actually triple-digit in the millions. We certainly solved that particular supply chain issue.”

By examining AwanTunai’s evolution from its founding through the challenges of the pandemic and into its current growth phase, we can uncover valuable insights about this strategic dilemma and draw lessons about when and how fintech startups should consider expansion beyond their initial focus areas.

Company History and Development

The Genesis of AwanTunai (2017)

L-R: AwanTunai co-founders Rama Notowidigdo and Dino Setiawan

The story of AwanTunai began with a convergence of expertise and vision. In late 2016, Rama Notowidigdo, who had recently sold his shares in Gojek where he served as Chief Product Officer, was not ready to retire. Instead, he began traveling through Indonesia’s countryside, where he witnessed firsthand the profound challenges of financial exclusion in regional areas. His dream was to build a digital rural bank that could address these issues.

Around the same time, Dino Setiawan returned to Asia after spending four and a half years in Palo Alto, where he had been running an alternative data-based underwriting financial inclusion fintech platform. Prior to his Silicon Valley experience, Dino had spent 12 years in banking, with his last position being VP of Investment Banking in Indonesia for Morgan Stanley.

The two met while consulting for a big data analytics company interested in entering the fintech space. During a lunch conversation, Rama shared his vision with Dino and described an experiment he had funded: a friend had gone into villages in Central Java and started lending at very low interest rates. The results were eye-opening—many farmers with access to low-cost credit were able to escape the poverty trap they were in.

For Dino, this was a compelling opportunity, despite his initial hesitation about starting another venture from scratch. What made the difference was Rama’s reputation as a “celebrity engineer” in Indonesia and his ability to bring along a significant portion of Gojek’s early engineering team. Together with Windy Natriavi, who brought operational expertise, they founded AwanTunai in 2017.

The founding team brought together over 40 years of combined experience in financial services and technology. This unique blend of banking knowledge, technological expertise, and operational experience would prove crucial in navigating the complex challenges of Indonesia’s financial landscape.

Years later, CFO Shilpa Gautam reflected on what drew her to join the company: “I was introduced to AwanTunai by one of its existing investors. At that point in time, I had obviously heard a lot about AwanTunai because they had just closed their Series A round with IFC as a lead investor. Everyone has tried their hand at lending into the microsegment, but this was one startup that really caught my attention because this was also IFC’s first investment in Southeast Asia and in fintech lending.”

Experimentation and Finding Product-Market Fit (2017-2019)

AwanTunai with micro-merchants. From KrAsia: https://kr-asia.com/awantunai-raises-usd-20-million-to-fund-indonesias-msmes-merchants

The early days of AwanTunai were characterized by disciplined experimentation. The company was driven by a data-first approach, where decisions were made based on field data rather than opinions. As Dino noted, “Myself as CEO, my opinion actually doesn’t count unless it’s backed up by field data.”

This disciplined approach to decision-making enabled AwanTunai to test a wide range of products and iterations in the field. Before settling on their flagship product, AwanTempo, the company experimented with ten different products in the space of two years. When data indicated that something wasn’t working or wouldn’t scale within their economic parameters, they moved on without becoming emotionally attached to any particular solution.

The team also resisted the temptation to prematurely boost their numbers through cash burning, a common practice among startups seeking to appeal to investors. Instead, they maintained the discipline to keep iterating until they found genuine product-market fit.

A critical insight emerged during this period: serving the unbanked or micro-merchants of Indonesia was a challenge that had defeated many organizations, including large financial institutions. From 1997 to 2007, the Indonesian central bank had pushed banks to serve this difficult segment with credit, with disastrous results—loss rates and non-performing loans (NPLs) were extremely high.

AwanTunai’s breakthrough came from understanding that transaction data could be used to differentiate good borrowers within what would traditionally be considered a “deep subprime” segment.

By installing point-of-sale (POS) or electronic data capture (EDC) hardware into traditional wholesalers—who typically recorded data with pen and paper—AwanTunai captured valuable offline transaction data. This data allowed them to underwrite purchase financing for the MSME customers of these wholesalers, as inventory levels were highly correlated with business performance.

“What AwanTunai is doing is digitizing the traditional supply chain, building a digital infrastructure in the FMCG space, and monetizing through embedded financing,” explained Gautam. “We are bringing about that change in the microsegment of Indonesia. And our vision is to provide very low-cost financing for micro and SMEs. I personally believe SMEs are the engine for economic growth and unsecured lending can unlock a massive amount of economic growth and prosperity.”

With this proprietary data acquisition model, AwanTunai launched AwanTempo in 2019, their flagship inventory purchase financing product. This solution allowed them to finance purchases for merchants at low-interest rates while generating good margins for the business and maintaining record-low NPLs (1% 90-day past due to date).

During this early phase, the company’s disciplined approach and focus on sustainable growth rather than rapid expansion attracted initial investor interest. Even then,while not yet in the form it is today, regional investors were attracted to AwanTunai’s ability to experiment and rethink financing. In 2018, the company raised a $4.3 million Series A round, led by Insignia Ventures Partners and AMTD Group.

Navigating the Pandemic: A Test of Resilience (2020-2021)

AwanTunai CEO and co-founder Dino Setiawan receiving an award from the Monetary Authority of Singapore for Singapore Fintech Festival

When COVID-19 hit Indonesia in early 2020, AwanTunai was servicing FMCG supply chains composed of principals, distributors, and small mom-and-pop retail shops. These businesses were already reeling from heated protests in Jakarta and heavy floods that had occurred in the span of a month.

While the pandemic severely impacted the financing sector, with recovery rates crashing and NPLs skyrocketing across the industry, AwanTunai demonstrated remarkable resilience. The company’s focus on catering to the needs of their ecosystem of suppliers and micro-merchants enabled them to quickly mitigate risks and position themselves for antifragility—not merely surviving the crisis but growing stronger because of it.

Several strategic decisions proved crucial during this period:

- Risk Management: AwanTunai tightened its underwriting process to minimize potential defaults while ensuring continued funding to creditworthy micro-merchants. This conservative approach earned them the continued support of their lending partners.

- Supplier Support Program: The company worked with suppliers to implement a program that gave merchants breathing space to clear out unsold inventories and continue with AwanTempo-financed purchases at a sustainable pace.

- Upstream Expansion: Recognizing that suppliers in their network were also experiencing cash management difficulties, AwanTunai began extending credit lines to wholesaler suppliers. This move not only supported the cash flow of suppliers but also increased adoption of their micro-merchant services, as suppliers needed to transact SKUs via the AwanTunai app to receive loans.

- Digital Acceleration: AwanTunai fast-tracked product development to protect their field teams while still engaging with suppliers and micro-merchants. By Q2 2020, they had launched their first digital online product, where micro-merchants could not only access AwanTempo financing but also make cashless payments and order SKUs online through AwanToko.

“We’ve been quite contrarian in our approach,” Gautam reflected on this period. “Our philosophy has always been, we solve for risk before solving for scale.” This disciplined approach to risk management would prove to be a critical differentiator during the pandemic, when many lenders saw their loan books deteriorate rapidly.

The company’s resilience during this challenging period attracted significant investor confidence. In July 2020, AwanTunai raised US$20 million in debt financing led by private debt investor Accial Capital to support their expansion into wholesaler supplier financing. This funding came at a critical time when many lenders were pulling back from the market, highlighting investors’ faith in AwanTunai’s risk management capabilities and business model.

The results were impressive: despite going through what Dino described as “the worst credit cycle in recent history,” AwanTunai achieved a 97% recovery rate (only 3% NPL) and grew revenues by 600% while maintaining a near-pristine loan book.

Building on this momentum, AwanTunai raised a successive Series A equity round. It was announced in August 2021, at US$11.2 million, with participation from Insignia Ventures Partners, Global Brain, BRI Ventures, and OCBC NISP Ventura.

This equity fundraise was part of a larger $56.2 million A2 funding round that included both equity, demonstrating the company’s ability to attract diverse forms of capital even in a challenging market environment.

Following these rounds, AwanTunai expanded its team, highlighted by management hires including seasoned UK and India banking executive Shilpa Gautam joining as CFO and seasoned US tech executive Ying Li as Chief Science Officer (then CTO).

Scaling and Innovation: The App-less Revolution (2021-2024)

Building on their pandemic-era resilience, AwanTunai entered a phase of significant growth and innovation from 2021 to 2024. The company experienced an eightfold increase in the number of suppliers and a corresponding eightfold growth in embedded financing, reaching approximately 800 million annualized. Even more impressive was the 14-fold growth in transaction data captured by their ERP systems and a 14-fold growth in contribution margin.

“It’s only been two years, but it’s been 8x growth since I’ve joined,” noted Gautam, who came aboard as CFO during this period of rapid expansion. “So it feels like I’ve been here longer, and that’s a great thing, right? It feels like I’ve known Dino and Rama forever.”

A pivotal strategic shift during this period was moving away from a mobile app approach toward “app-less” solutions for tech-illiterate users. As Dino explained, “Risk management and scaling relied on utilizing a mobile app, which we found to be expensive and challenging in this micro tech-illiterate space.” The company realized that serving micro-merchants through an app-less solution might be more effective.

This insight led to significant growth in their ERP infrastructure and adoption at the middle layer of the supply chain. AwanTunai replaced incumbent systems and captured high-quality transaction data, which was crucial for their financing business. The company custom-built their system to detect fraud, an advantage that stemmed from starting as a lender with risk management in their DNA.

As Dino noted, “A lot of the e-commerce marketplace folks have scaled up their systems to optimize for GTV capture, and sometimes there’s a bit of a perverse incentive where if there’s some fraudulent GTV, it’s still captured because it’s driving up the valuation. But for us, since we started life off as a lender and risk management is part of our DNA, we custom built the system to detect fraud.”

“The value of solving risk before scale,” Gautam explained, “has been through our proprietary ERP solution capturing alternative sources of data to underwrite loans.” This approach not only protected AwanTunai during the pandemic but positioned them for significant growth afterward.

AwanTunai also invested in world-class talent for data science and risk management, securing patents for their technology. Their Chief Science Officer brought a nuanced perspective on artificial intelligence, noting that “artificial intelligence can’t beat a trained human” with structured data. This led to a focus on having experienced humans guide AI engine development with the right variables and proxies.

“Earlier this year, we hired a head of internal audit whose job is to create these controls across the right divisions, be it sales, treasury, or product,” Gautam shared. “We have very senior leaders from OCBC, from HSBC who’ve joined us. And they have been very instrumental in setting up this control framework.”

The company’s growing success and innovative approach continued to attract significant investment. In March 2022, the International Finance Corporation (IFC), a member of the World Bank Group, invested $5 million in equity, as part of a US$8.5 million round, to finance AwanTunai’s supply chain-focused lending platform. This institutional backing provided not only capital but also validation of the company’s approach to financial inclusion.

Later on in March 2024, AwanTunai announced a US$27.5 million Series B round, led by Norfund, the Norwegian government’s investment fund focused on developing countries, MUFG Innovation Partners (MUIP) – the innovation wing of Japan’s MUFG Bank, and OP FinnFund, a Finnish impact investment firm.

Not long after this equity round, in July 2024, AwanTunai secured a IDR 300 billion (~US$17 million) debt facility from HSBC as part of the bank’s USD 1 billion ASEAN Growth Fund. This was followed by a substantial US$60 million debt financing round in December 2024, led by US-based impact-focused investor Accial Capital, marking their continued support for the company.

HSBC managing director and head of wholesale banking Riko Tasmaya (left to right), HSBC head of commercial banking for Southeast Asia Amanda Murphy, AwanTunai CFO Shilpa Gautam and Awan Tunai cofounder Rama Notowidigdo pose for a photo following an interview with The Jakarta Post in Jakarta on July 23, 2024. (HSBC/-). This article was published in thejakartapost.com with the title “”. Click to read: https://www.thejakartapost.com/business/2024/07/24/fintech-firm-awantunai-secures-rp-300-billion-debt-facility-from-hsbc.html.

Altogther, AwanTunai has raised more than US$175 million across all funding rounds (not including the debt facility).

“One thing which I personally found very useful was building relationships along the way,” Gautam reflected on the fundraising process. “Building these relationships with the right investors so that they become advocates of your companies to other investors.”

By 2023, AwanTunai had empowered over 35,000 SMEs through financing and was facilitating over US$3 billion in sales. Their ERP system provided order management, customer management, payment acceptance, and inventory management, effectively transforming suppliers and merchants in the downstream supply chain.

The company’s approach to talent acquisition was also noteworthy. Rather than competing solely on compensation, AwanTunai attracted world-class technical talent by offering interesting problems to solve. “Building Technology for the Tech Illiterate” served as a compelling hook for technical talent who found the challenge of getting user adoption, especially when the user is tech-illiterate or doesn’t even have a phone, to be an exciting problem to solve.

Throughout this period, AwanTunai maintained its focus on optimizing for a sustainable business model rather than just top-line growth. As Dino observed, “For the longest time, VCs dismissed the idea that lending could be profitable. Back in the easy money days, we were like the ugly duckling. But now we’re getting close to profitability, and hopefully, this is our moment in the spotlight.”

The company’s achievements were recognized on the global stage when Gautam represented AwanTunai at the World Economic Forum in Davos in January 2024. “In 2023, there were 6,000 startups invited to Founders Games from across 150 countries,” she explained. “Through various rounds, we were invited to Davos, where the finals were being held. So the top 12 companies selected from COP28 were to come to Davos, and AwanTunai won Founders Games, which was a fantastic moment for me. It really felt like all the hard work Dino, Rama, and the whole AwanTunai team had put in. We’re really doing something to change lives or really bringing about impact, which is financial inclusion in Indonesia. And this is a textbook example for FinTech lenders globally.”

Shilpa Gautam at Webit Davos Grand Finals

By 2024, AwanTunai had established itself as Indonesia’s leading supply chain financing and ERP platform, operating at the intersection of fintech and software. The company had proven that lending could be profitable in an industry long considered difficult to serve, while also driving digital transformation in Indonesia’s massive FMCG sector. However, with substantial venture capital now invested in the company, the question of whether their focused approach would be sufficient to deliver the returns expected by investors was becoming increasingly pertinent.

“We are building the next wave of financial inclusion in Indonesia,” Gautam asserted, “which will hopefully be a textbook example for financial inclusion globally.”

Key Learnings and Analysis

AwanTunai’s journey offers several valuable insights about financial inclusion, technology adoption, and strategic focus in emerging markets. This section examines eight key learnings that have emerged from their experience and analyzes their implications for the company’s future strategy.

(1) Data-Driven Discipline and Decision Making

AwanTunai’s success has been built on a foundation of disciplined, data-driven decision making. From the beginning, the company established a culture where field data, not opinions, drove strategic choices. As CEO Dino Setiawan noted, “Myself as CEO, my opinion actually doesn’t count unless it’s backed up by field data.”

This approach enabled AwanTunai to test multiple products and iterations rapidly, abandoning those that didn’t work without becoming emotionally attached to any particular solution. Their willingness to be guided by data rather than preconceptions or industry trends allowed them to discover unique insights about their market and develop solutions that addressed genuine needs rather than perceived ones.

Implications for Future Strategy: AwanTunai’s data-driven culture positions them well for continued success in their current market. Their accumulated data about FMCG supply chains and micro-merchant behavior represents a significant competitive advantage that would be difficult for new entrants to replicate. By continuing to refine their data collection and analysis capabilities within this sector, they can further strengthen their market position and develop increasingly sophisticated products and services tailored to the specific needs of their customers.

If they eventually consider expansion, this data-driven approach would be a valuable asset in evaluating new opportunities. However, they would need to recognize that their existing data primarily relates to FMCG supply chains in Indonesia. Expanding to new sectors or geographies would require building new data sets from scratch, which could be time-consuming and resource-intensive. Any expansion strategy should include a clear plan for data acquisition and analysis in the new context.

(2) Ecosystem Thinking

Rather than focusing on individual pain points, AwanTunai has taken a holistic view of the FMCG supply chain ecosystem. They recognized that the challenges faced by micro-merchants were interconnected with those of wholesalers and suppliers, and that addressing these challenges in isolation would be ineffective.

This ecosystem perspective led them to develop solutions that created value for multiple stakeholders simultaneously. By installing their ERP system at wholesalers, they not only digitized operations for these businesses but also gained valuable transaction data that enabled them to provide financing to micro-merchants. During the pandemic, they extended this approach by providing credit lines to wholesaler suppliers, supporting the entire supply chain rather than just one segment.

Implications for Future Strategy: If AwanTunai maintains their current focus, this ecosystem thinking can be further developed within the FMCG supply chain. There may be opportunities to create additional value by addressing other interconnected challenges within this ecosystem, such as logistics, inventory optimization, or direct connections to manufacturers. By deepening their understanding of the entire value chain, they can identify new ways to create and capture value while strengthening their position as an essential partner for all participants.

If they eventually consider expansion, this ecosystem perspective would be a valuable lens for evaluating new opportunities. Rather than simply looking for adjacent markets, they might consider adjacent ecosystems where similar interconnections exist and where their approach to creating multi-stakeholder value could be applied. This might include other retail sectors, agricultural supply chains, or service-based industries with similar ecosystem dynamics.

(3) Building for Market Context

One of AwanTunai’s most significant insights has been the importance of designing technology solutions that match the capabilities and constraints of their users. Rather than assuming that all users would adopt smartphone apps, they recognized the reality of tech illiteracy among many micro-merchants and developed “app-less” solutions that were more accessible to this audience.

As Dino explained, “Risk management and scaling relied on utilizing a mobile app, which we found to be expensive and challenging in this micro tech-illiterate space.” This realization led to a strategic shift toward solutions that met users where they were rather than expecting them to adapt to more sophisticated technologies.

Implications for Future Strategy: If AwanTunai continues to focus on their current market, this principle of appropriate technology design will remain crucial. As they seek to reach more micro-merchants and digitize more of the supply chain, they will need to continue developing solutions that are accessible to users with varying levels of technological literacy. This might include further refinements to their “app-less” approach or new interfaces designed specifically for users with limited digital experience.

If they eventually consider expansion, this insight about matching technology to user capabilities would be a valuable differentiator. Many technology companies struggle to serve populations with limited digital literacy, creating potential opportunities for AwanTunai to apply their expertise in markets or segments that have been overlooked due to these challenges. However, they would need to carefully assess whether the specific approaches they’ve developed for FMCG micro-merchants would translate effectively to new contexts.

(4) Lending as a Gateway to SaaS Adoption

AwanTunai discovered that in their market, lending could serve as an effective gateway to broader technology adoption. While many companies have struggled to monetize SaaS solutions for MSMEs in emerging markets, AwanTunai found that offering financing first created a compelling value proposition that encouraged adoption of their broader technology platform.

As Dino observed, “A lot of investors still see us as lenders, but honestly, the vision is digitizing the supply chain… It just so happens we monetize through lending because the monetization rate in lending is 20x greater than anything you can achieve on the SaaS side.”

The monetization rate in lending is also significantly higher—approximately 20 times greater than what can be achieved on the SaaS side alone. This economic reality means that AwanTunai can subsidize SaaS adoption through lending revenues, creating a sustainable business model that delivers both financial inclusion and digital transformation.

Implications for Future Strategy: If AwanTunai continues to focus on their current market, this “lending as a gateway” model can be further optimized within the FMCG supply chain. They could develop additional SaaS features that create more value for their existing customers, increasing stickiness and potentially enabling them to capture more transaction data, which in turn improves their lending capabilities.

If they eventually consider expansion, this model could potentially be applied to other industries beyond FMCG where businesses face similar working capital constraints and technology adoption challenges. Industries such as agriculture, construction, or small-scale manufacturing might benefit from a similar approach. However, AwanTunai would need to carefully assess whether they have the necessary risk management capabilities and industry knowledge to successfully underwrite loans in these new sectors.

(5) Risk Management as a Core Competency

AwanTunai’s disciplined approach to risk management has been a defining feature of their success. From the beginning, they took a conservative view on risk, focusing on becoming “FMCG risk management experts in the country” before considering different industry segments. This focus paid dividends during the pandemic when they achieved a remarkable 97% recovery rate despite the severe economic disruption.

The company’s investment in world-class talent for data science and risk management, including securing patents for their technology, reflects their understanding that superior risk assessment is a fundamental competitive advantage in financial services. Their Chief Science Officer’s nuanced perspective on artificial intelligence—recognizing that AI models need to be guided by experienced humans with domain expertise—has shaped their approach to developing scalable risk engines.

As CFO Shilpa Gautam explained, “We’ve been quite contrarian in our approach. Our philosophy has always been, we solve for risk before solving for scale.” This approach has enabled AwanTunai to build a sustainable business in a sector that many others have failed to crack.

Implications for Future Strategy: If AwanTunai maintains their current focus, continuing to refine their risk management capabilities within the FMCG sector will further strengthen their competitive position. They can deepen their expertise, improve their risk models with more data, and potentially expand their lending parameters while maintaining their industry-leading low NPL rates.

Should they eventually explore expansion, they would need to recognize that risk management capabilities are often context-specific. AwanTunai’s expertise is currently concentrated in the FMCG supply chain, and expanding to new sectors would require building similar risk assessment capabilities from the ground up, which could be time-consuming and capital-intensive. Before any expansion, the company should carefully evaluate whether their existing risk models and expertise can be adapted to new contexts or whether they would need to make significant new investments.

(6) Sustainable Growth Over Hypergrowth

Throughout their journey, AwanTunai has prioritized sustainable growth over hypergrowth. They resisted the temptation to boost their numbers prematurely through cash burning, maintained discipline in their product development process, and focused on building a profitable business rather than maximizing vanity metrics.

This approach was sometimes at odds with prevailing venture capital preferences, particularly during the “easy money days” when many investors prioritized growth at all costs. As Dino noted, “For the longest time, VCs dismissed the idea that lending could be profitable. Back in the easy money days, we were like the ugly duckling.”

However, this focus on sustainability has positioned AwanTunai well for the current market environment, where profitability and capital efficiency are increasingly valued. As they approach profitability, their proven ability to grow while maintaining financial discipline will be a significant advantage in attracting both customers and investors.

Implications for Future Strategy: If AwanTunai continues with their focused approach, their emphasis on sustainable growth and path to profitability aligns well with current investor expectations. They can continue to scale within their existing market while maintaining their disciplined approach to risk and capital efficiency, potentially achieving profitability sooner than if they were to pursue aggressive expansion.

With substantial venture capital now invested in the company, AwanTunai does face increased pressure to deliver significant returns. This creates a tension between maintaining their disciplined approach to growth and meeting investor expectations for scale. If they eventually consider expansion, any strategy should carefully balance these competing priorities. The company might consider a “portfolio approach,” where a portion of resources is allocated to exploring new opportunities while the core business continues to grow sustainably.

(7) Talent Attraction Through Meaningful Challenges

AwanTunai’s experience in attracting world-class technical talent offers valuable lessons for their future growth. Rather than competing solely on compensation, they’ve found success by offering interesting and meaningful problems to solve. The challenge of “Building Technology for the Tech Illiterate” has proven to be a compelling hook for talented engineers and data scientists who want their work to have significant social impact.

As Dino explained, “One of the interesting realizations is that it’s not about the money. I mean, these are extremely expensive talents, right? But certainly, talents that we probably wouldn’t have been able to afford unless there was that X factor.”

This approach to talent acquisition and retention will be increasingly important regardless of AwanTunai’s strategic direction. By framing their work as not just a business opportunity but a meaningful challenge with significant social impact, they can continue to attract the caliber of talent needed to solve complex problems in financial inclusion and supply chain digitization.

Implications for Future Strategy: If AwanTunai maintains their current focus, they can continue to deepen their impact within the FMCG supply chain, creating increasingly sophisticated solutions for financial inclusion that present compelling challenges for top talent. As Gautam notes, “We are building the next wave of financial inclusion in Indonesia, which will hopefully be a textbook example for financial inclusion globally.” This mission-driven approach can help them attract and retain exceptional talent even while focusing on a single sector.

If they eventually consider expansion, they should ensure that any new markets or products present similarly meaningful challenges with clear social impact. Expanding too broadly or into areas perceived as less impactful could dilute this value proposition and make it harder to attract the specialized talent needed for success in new areas.

(8) Organizational Adaptability in Complex Environments

As AwanTunai has grown, the complexity of the organization has increased significantly. This growth has required the leadership team, particularly CEO Dino Setiawan, to develop new capabilities—understanding interdepartmental dependencies, knowing when to go wide versus when to go deep, and building systems that can scale with the business.

This organizational adaptability will be crucial regardless of whether AwanTunai maintains their current focus or eventually explores new opportunities. The company’s culture of discipline and data-driven decision making provides a strong foundation for managing increasing complexity while maintaining their core values and customer focus.

Implications for Future Strategy: If AwanTunai continues to focus on FMCG supply chain financing, they will still face increasing organizational complexity as they scale within this market. Continuing to develop their management systems, team capabilities, and organizational processes will be essential for managing this growth effectively.

If they eventually consider expansion, these challenges would be magnified significantly. Before pursuing ambitious expansion plans, AwanTunai should assess their organizational readiness and potentially invest in building the necessary management systems and team capabilities. This might include developing a more formalized approach to new market entry, creating dedicated teams for exploring new opportunities, or implementing stage-gate processes for evaluating and scaling new initiatives.

The Strategic Crossroads: Deepening Focus vs. Expansion

The eight learnings above highlight that AwanTunai has viable strategic options whether they choose to maintain their focused approach on FMCG supply chain financing or eventually explore expansion opportunities.

On one hand, there are compelling reasons to maintain their current focus. As CFO Shilpa Gautam points out, “Just within this space, there is a hundred billion of inventory that flows through three levels. So it’s US$300B of flows that we are looking to finance. There still is a lending gap of about US$50B in total assets, which we can easily look to solve.”

This suggests significant room for growth even within their existing market. Their deep expertise in FMCG supply chain financing, proprietary data advantages, and disciplined approach to risk management have created a sustainable competitive advantage that would be difficult to replicate in new markets. Continuing to focus on this sector could allow them to achieve profitability sooner and establish an even stronger position in a massive market.

On the other hand, as a venture-backed company with over $177 million in funding, AwanTunai may eventually face expectations for expansion beyond their initial focus area. Their unique capabilities in data-driven decision making, ecosystem thinking, and building technology for tech-illiterate users could potentially create value in adjacent markets. If they do consider expansion, the learnings suggest a measured approach—perhaps following natural connections within their existing ecosystem rather than making dramatic leaps into unrelated markets.

What’s clear is that regardless of which path they choose, AwanTunai’s future success will depend on maintaining the disciplined, data-driven approach that has defined their journey thus far. As Gautam emphasizes, “We’ve been quite contrarian in our approach. Our philosophy has always been, we solve for risk before solving for scale.” This principle should continue to guide their strategic decisions, whether they’re deepening their current market position or potentially exploring new horizons.

Conclusion

AwanTunai stands at a strategic crossroads that is emblematic of successful venture-backed startups that have achieved product-market fit in a specific niche. The company has built a remarkable business by maintaining a disciplined focus on supply chain financing for MSMEs in Indonesia’s FMCG sector. Their deep understanding of this market, proprietary data advantages, and sophisticated risk management capabilities have enabled them to succeed where many others have failed, creating substantial value for both customers and investors.

With over $177 million in funding across multiple rounds, AwanTunai has demonstrated its ability to attract capital and scale its operations within its chosen market. The company’s journey from experimentation to resilience during the pandemic and now to significant growth showcases the power of their focused approach. Their innovative “app-less” solutions for tech-illiterate users and their insight that lending can be a gateway to SaaS adoption represent genuine innovations that have transformed how financial services are delivered to underserved segments.

However, the very success that has brought AwanTunai to this point now presents them with a fundamental strategic question: Is continuing to focus exclusively on FMCG supply chain financing in Indonesia sufficient to deliver the growth and returns expected of a venture-backed company of their scale? Or should they begin to explore expansion into new products, customer segments, or geographic markets?

The answer is not straightforward. On one hand, their current market remains vast and underpenetrated, with significant room for continued growth. Their competitive advantages are deeply rooted in their specialized knowledge and capabilities, which might be diluted by premature diversification. On the other hand, the expectations placed on venture-backed companies often include achieving scale and returns that may eventually require looking beyond their initial focus area.

The key learnings from AwanTunai’s journey suggest that if they do choose to expand, they should do so in a way that leverages their core strengths: data-driven decision making, ecosystem thinking, appropriate technology design, and disciplined risk management. Potential expansion paths might include:

- Vertical expansion within their existing customer base, offering new financial products or services to the MSMEs and suppliers they already serve

- Geographic expansion to bring their proven model to similar FMCG supply chains in other regions of Indonesia or Southeast Asia

- Adjacent market expansion to sectors with similar characteristics to FMCG, where their existing capabilities might provide competitive advantages

- Strategic partnerships that allow them to enter new markets while leveraging the domain expertise and distribution channels of established players

Ultimately, AwanTunai’s strategic decision will need to balance multiple considerations: the vast opportunity still available in their current market, the expectations of their investors, the capabilities and preferences of their team, and their mission to drive financial inclusion and digital transformation in Indonesia. What is clear is that the disciplined, data-driven approach that has defined their journey thus far should continue to guide their strategic decisions, whether they choose to deepen their current market position or explore new horizons.

As CFO Shilpa Gautam emphasized, “We are building the next wave of financial inclusion in Indonesia, which will hopefully be a textbook example for financial inclusion globally.” Whether through focused depth or measured expansion, AwanTunai is well-positioned to continue their mission of transforming Indonesia’s FMCG supply chain and creating meaningful impact for the millions of MSMEs that form the backbone of the country’s economy.

Exhibits

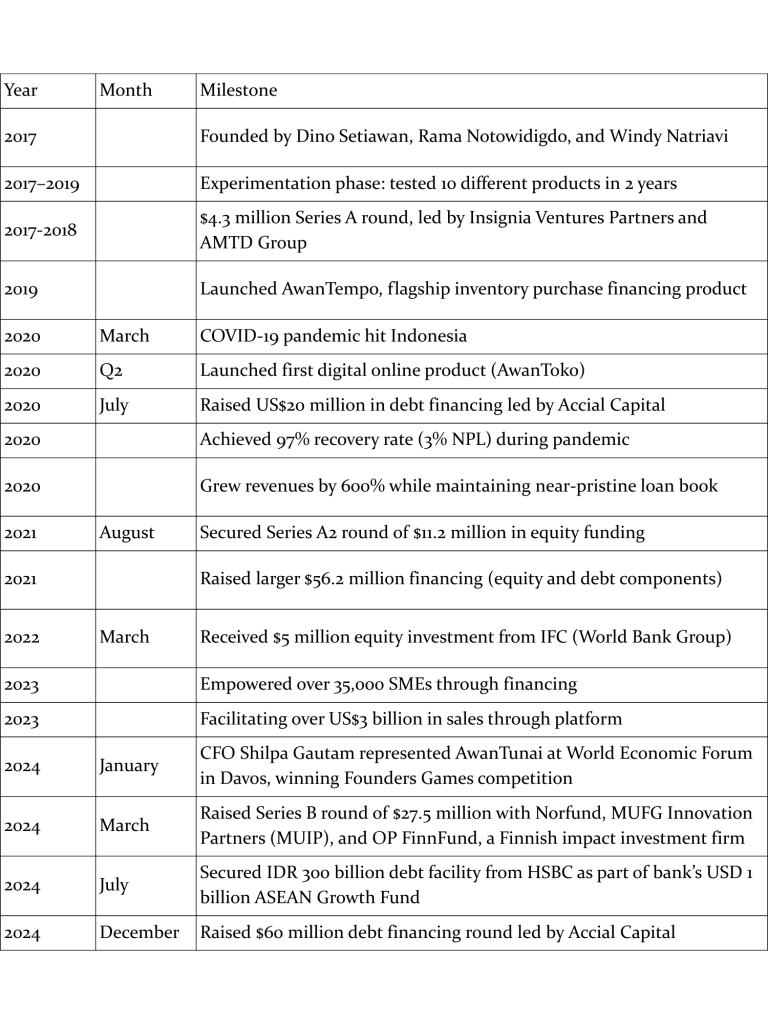

Exhibit 1: AwanTunai Growth and Fundraising Timeline

AwanTunai Timeline from Case Study

Exhibit 2: AwanTunai’s Reach in Indonesia

AwanTunai’s reach from AwanTunai website

Exhibit 3: Key Industry Statistics Indonesia’s FMCG and MSME Sector

MSME Landscape

- Number of MSMEs in Indonesia (2024): 66 million

- Self-employed workers in Indonesia (2024): Over 30 million

- MSME business index (Q3 2024): 102.6, indicating continued expansion

- MSMEs contribution to Indonesia’s GDP: More than 60%

- Percentage of Indonesian businesses that are MSMEs: More than 99%

- Workforce employed by MSMEs: More than 90%

Financial Inclusion

- Unbanked or underbanked adults in Indonesia: Almost 50% of the adult population

- Credit-to-GDP ratio (end of 2023): 31.4%, well below peer countries in the region

- Indonesia’s population (2024): Over 273 million people spread across thousands of islands

FMCG Market

- Indonesia’s FMCG market size: Approximately US$100 billion

- FMCG market growth (2024): Projected 5% value growth compared to 2023

- FMCG market resilience: 5.7% year-on-year increase in market value in Q2 2024 despite inflation

- Total inventory flows through three levels of FMCG supply chain: US$300 billion

- Lending gap for FMCG MSMEs: Approximately US$50 billion in total assets

Digital Transformation

- MSMEs in services sector: Approximately two-thirds of all MSMEs

- Indonesia’s economic growth (Q2 2024): Persistent at 5.05% level

- Digital infrastructure development: Key focus on supporting digital transformation of 64 million MSMEs

- FMCG sector digitalization: Rapid growth fueled by shifting consumer preferences and technological adoption

Supply Chain Challenges

- Traditional FMCG supply chain: Multiple layers from manufacturers to distributors, wholesalers, and retailers

- NPL rates during pandemic: Industry average of 20-30% vs. AwanTunai’s 3%

- Key challenges: Working capital constraints, lack of technological infrastructure, information asymmetry

- Financing barriers: High interest rates, stringent collateral requirements, cumbersome application processes

Exhibit 4: AwanTunai’s Performance Metrics

Key Performance Indicators (2023)

- Number of SMEs empowered through financing: Over 35,000

- Total sales facilitated through platform: Over US$3 billion

- Growth in number of suppliers (2021-2023): 8x increase

- Growth in embedded financing (2021-2023): 8x increase, reaching approximately 800 million annualized

- Growth in transaction data captured by ERP systems (2021-2023): 14x increase

- Growth in contribution margin (2021-2023): 14x increase

- NPL rate during pandemic: 3% (vs. industry average of 20-30%)

- Revenue growth during pandemic: 600%

Sources:

- Statista (2024): MSMEs in Indonesia statistics

- Indonesia Financial Sector Development Report (Q3 2024)

- World Economic Forum (2024): Indonesia financial inclusion report

- Asia Small and Medium-Sized Enterprise Monitor (2024)

- OECD Economic Surveys: Indonesia (2024)

- AwanTunai company data and interviews

Teaching Note

Get a pdf copy of the teaching note by messaging us on LinkedIn.

References

- “Data, Discipline, and Decision Making with AwanTunai CEO and co-founder Dino Setiawan.” Insignia Ventures Partners. April 13, 2020. https://review.insignia.vc/2020/04/13/data-discipline-and-decision-making-with-awantunai-ceo-and-co-founder-dino-setiawan/

- “Elements of Antifragility: A Case Study on Indonesian SME supply chain financing startup AwanTunai.” Insignia Ventures Partners. April 6, 2021. https://review.insignia.vc/2021/04/06/elements-antifragility-case-study-indonesian-sme-supply-chain-financing-startup-awantunai/

- “Dino Setiawan, CEO of AwanTunai on revisiting a year of resilience and lending as the key to supply chain SaaS adoption in Indonesia.” Insignia Ventures Partners. April 28, 2021. https://review.insignia.vc/2021/04/28/dino-setiawan-ceo-awantunai-revisiting-a-year-of-resilience-lending-unlocking-supply-chain-saas-adoption-indonesia/

- “The Year After Lending.” Insignia Ventures Partners. June 1, 2021. https://review.insignia.vc/2021/06/01/the-year-after-lending/

- “Call #123: How app-less drives tech adoption, data wins world-class talent, and scalable risk engines unlock growth with AwanTunai CEO and Co-Founder Dino Setiawan.” Insignia Ventures Partners. April 18, 2023. https://review.insignia.vc/2023/04/18/season-5-episode-12-call-123-awantunai-dino-setiawan/

- “How a supply chain financing & ERP platform has been digitizing an >US$100B industry in 5 Numbers.” Insignia Ventures Partners. May 12, 2023. https://review.insignia.vc/2023/05/12/awantunai-in-5-numbers/

- “AwanTunai secures $27.5m in Series B funding to transform Indonesia’s cash economy.” Fintech Global. March 14, 2024. https://fintech.global/2024/03/14/awantunai-secures-27-5m-in-series-b-funding-to-transform-indonesias-cash-economy/

- “Call #161: How this Indonesian fintech is setting new standards for financial inclusion globally with AwanTunai CFO Shilpa Gautam.” Insignia Ventures Partners. May 2, 2024. https://review.insignia.vc/2024/05/02/season-6-episode-11-call-161-shilpa-gautam-part-1/

- “AwanTunai CFO Shilpa Gautam on the making of a fintech CFO.” Insignia Ventures Partners. May 8, 2024. https://review.insignia.vc/2024/05/08/season-6-episode-12-call-162-shilpa-gautam-awantunai-cfo-part-2/

- “Indonesia’s MSME-focused fintech AwanTunai: Digitizing the FMCG supply chain.” Insignia Ventures Partners. March 15, 2024. https://review.insignia.vc/2024/03/15/indonesia-msme-awantunai/

- “Number of micro, small and medium enterprises (MSMEs) in Indonesia from 2013 to 2022.” Statista. 2024. https://www.statista.com/statistics/1546194/indonesia-number-of-msmes/

- “Indonesia Financial Sector Development Report.” World Bank Group. Q3 2024.

- “Indonesia Financial Inclusion Report.” World Economic Forum. 2024.

- “Asia Small and Medium-Sized Enterprise Monitor.” Asian Development Bank. 2024.

- “OECD Economic Surveys: Indonesia.” Organisation for Economic Co-operation and Development. 2024.

Subscribe to read the full case study. Send us a message to our LinkedIn company page to get the Teaching Note as well for discussion and classes.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.