Fintech Business Hours Call

Before you jump into this. Two important things:

- I am launching fintech business hours. For the past year or so, I have spoken with a number of fintech entrepreneurs who have just launched their businesses or are still working on their ideas. Most entrepreneurs reach out seeking advice on market opportunity, business model, fundraising, etc…or simply to exchange notes on the fintech landscape in Southeast Asia. Either way, I want to dedicate a regular monthly slot for these conversations and invite any fintech founder for a chat here.

- I’d appreciate it if after registering for a chat to please contribute to the COVID19 relief efforts in India by donating to a charity of your choice (some curated examples here to help guide you if needed: https://donate.indiacovidresources.in/)

Thanks and enjoy the post!

“Cash Rules Everything Around Me, C.R.E.A.M. Get the Money!” – Wu Tang Clan

Highlights

- A combination of health crisis, economic shutdown, government-sponsored interest and loan moratoriums around the region have sent (cash!) recovery rates crashing, NPL skyrocketing and SME lenders back to the drawing board to revisit the fundamental question of lending: information asymmetry.

- Technology has enabled SME lenders to augment underwriting signals, either for more effective credit scoring or to open up risk models with previously weak signals. Whether new tech-enabled signals (e.g. social media, telco data) have tremendously improved credit models fundamentally across all segments remains a question at this point.

- Information asymmetry is only solved by a lender during underwriting. Transaction-based lending offers a way to solve it continuously and offer borrowers credit leveraging more leading signals as opposed to the lagging indicators most lenders use.

- Transaction-based (as opposed to underwriting) SME lending platforms capture a meaningful share of the business generated by borrowers on these same platforms, creating a complete picture of their borrowers’ financial health.

Throwing yesterday’s models through the windows

“One of the main advantages that [insert lender’s name] has over their competitors is the amount of data that their [2/3/5/10]-year history provides. They have taken a closer look at their underwriting models which now is leveraging machine learning even more and adding [insert aptly-named and possibly statistically irrelevant variables]…to meaningfully decrease portfolio’s risk and increase returns for investors.”

Most if not all digital lenders over the past 4-5 years have touted a version of this pitch to showcase a certain competitive advantage built around tech. Yet, over a year ago, the COVID19 pandemic came crashing on tech-enabled underwriters, teams scrambled to adjust to “post-COVID19 risks”, and tighten up (or stop altogether) any new loan origination until further notice.

A combination of a health crisis, economic shutdown, government-sponsored interest, and loan moratoriums around the region have sent (cash!) recovery rates crashing, NPL skyrocketing and SME lenders back to the drawing board to revisit the fundamental question of lending: information asymmetry.

How do we know what we need to know?

At its core, a lender allocates capital it receives on a risk-adjusted basis to the borrowers it acquires. The lender needs to pull as much information as possible from that borrower as well as third-party sources to reduce information asymmetry and better underwrite risk.

The lender assesses borrowers based on a number of signals, and comes up with a risk score that reflects the borrower’s probability of default, this process is usually done using an internal scorecard (previously trained on multiple borrowers’ cohorts). Depending on the score assigned, the borrower is rejected, or approved for a loan of a certain amount, tenor, and interest rate. (In practice a two-step process is usually in place to pre-approve and build a full scoring profile later but I digress…).

Let’s talk about these signals for a moment. In some (mostly developed) jurisdictions, lenders can use credit bureaus or credit reference agencies to pull reliable credit scores assigned to particular borrowers based on their credit history. Adding to that first signal, others such as bank statements, invoices, time in operations, company’s size/turnover if you are serving SMEs, lenders built a reasonably accurate internal risk score.

The “beauty” of technology is the ability to augment further these signals by either:

- accessing proprietary data sets that can improve these signals further than publicly available information. In effect for the same borrower, the model predicts a lower probability of default using this proprietary data. Since there is a lower probability of default, a lender can offer a borrower a lower interest rate compared to competitors, therefore gaining market share

- accessing proprietary data sets that can make a risk model work where previously the signals were too weak to come up with an accurate risk score. Lenders can now underwrite the risk of a new category of borrowers that was previously shut down from credit markets, therefore expanding the market

New proprietary signals can deepen and broaden the ability of lenders to offer economically viable loans to a greater number of borrowers.

The jury is still out on most new signals

Digital lenders born in the last decade have experimented with new third-party signals such as social media, and telco data to improve credit scoring with varying degrees of success. In recent years, authorities have cracked down on the usage of such data for the purpose of credit scoring with data protection laws in effect across most countries in Southeast Asia.

Some lenders were collecting data to credit-score but some leveraged the same data points while servicing loans, calling acquaintances of their consumers’ borrowers, or even posting threatening messages on their social media accounts.

Whether these new signals have tremendously improved credit models fundamentally across all segments remains a question at this point. And even if some companies have witnessed such improvements, massive economic shocks such as the ongoing pandemic will invariably render the scorecards built on these signals much less relevant.

The issue that emerges is that information asymmetry is only solved by a lender at a certain point in time (during underwriting), instead there should be a way to solve it continuously and offer borrowers credit in a truly dynamic way leveraging more leading signals as opposed to the lagging or snapshot indicators most lenders use at the moment.

What if we could underwrite without having underwriting?

What if a lender could be directly plugged into the businesses it serves by offering a suite of services that enable a dynamic and real-time view of their financial health?

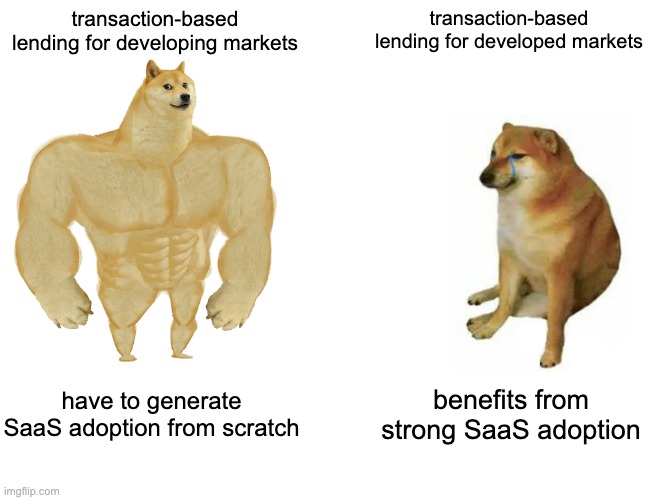

Enter transaction-based lending. Popularized in other markets by payment platforms such as Stripe, Square, or StoneCo, horizontal marketplaces such as Amazon or Alibaba, and vertical SaaS solutions such as Toast that have each launched lending products to leverage proprietary, transaction-level data. These platforms have combined a transaction, payment, and lending stack that allow them to have an accurate picture of the borrowers’ financial health.

Yet, building a similar 360 view of a business in Southeast Asia remains a challenge as most businesses conducted by SMEs remain conducted offline. Conversely, players in developed markets have benefited from a relatively stronger SaaS (and payment) adoption to layer on lending.

SEA lenders are now looking to re-invent their businesses by offering a mix of payments, transaction, book, and business management along with lending. This combination enables them to leverage new signals to offer lower interest rates while reducing portfolio losses creating a powerful winning equation.

What if a lender could be directly plugged into the businesses it serves by offering a suite of services that enable a dynamic and real-time view of their financial health?

Our portfolio company AwanTunai has embedded its lending products into its clients’ operations, pulling in real-time, and in an automated way relevant and precise signals to underwrite better. AwanTunai enables its clients to manage their supply chain efficiently, order inventory and sell their products, process orders, accept payments, finance their inventory, and extend credit to their clients all from one platform.

The data captured through the platform helps AwanTunai better acquire, better underwrite, and better service its loans in a cost-efficient manner. Why is that? Payment data provided helps shorten the underwriting process to an instant, real-time cash-flows assessment and access to inventory and AR/AP ledgers help identify customers with high intent for (re-)financing and target them with personalised offers. The underwriting process is also improved as signals are now real-time, and granular enough to adapt to fast-changing micro and macro-level conditions. What all lenders and borrowers would want in pandemic scenarios.

Finally, the loan servicing becomes more seamless with more leading signals. A real-time assessment of the business post-disbursement helps send the right notifications at the right time for the borrowers to repay, identify borrowers that are on the verge of missing payments and offer an automated way to restructure loans.

Towards the holy grail of real-time cash flow-based lending

The ongoing pandemic has reset the playing field for lenders in Southeast Asia. Most lenders have experienced for the first time a drastic economic downturn challenging the assumptions behind their underwriting. Most of the signals collected by lenders are only proxies for the real cash-flow situation of the borrowers (i.e whether they will be able to repay their loans).

A broader set of payment and transaction-related features will help lenders accumulate enough real-time data to accurately predict the need for financing and possibly pre-approve some borrowers for future financing. Lenders would also not need to acquire potential lenders at high customer acquisition cost and try to determine intent and probability of default. For borrowers, they would not have to go through a time-consuming and still paper-based process (for SMEs that is).

Samir Chaibi is a seasoned investment professional whose experience ranges from investment banking to venture capital. He has served as board director on numerous startups across the globe and has also been a founder himself. He now focuses on finding the next big thing in fintech and SaaS in Southeast Asia.

Hit him up for a chat at samir@insignia.vc if you are a founder building a fintech, proptech, or SaaS startup in Southeast Asia!