Southeast Asia’s fintech market stands at an extraordinary inflection point. According to UnaFinancial’s latest analysis, the region’s fintech market is projected to surpass $1.073 trillion in 2025, representing an 18.3% year-over-year increase from $907 billion in 2024 [1]. This is not merely a story of market growth; it represents a fundamental transformation where the convergence of embedded finance and agentic AI is unlocking unprecedented opportunities across the region’s diverse economies.

The evolution from single-purpose applications to intelligent, autonomous financial agents marks the next frontier in Southeast Asia’s fintech journey. This transformation promises to redefine financial services for hundreds of millions of consumers and businesses, building upon a foundation that has already demonstrated remarkable resilience and innovation.

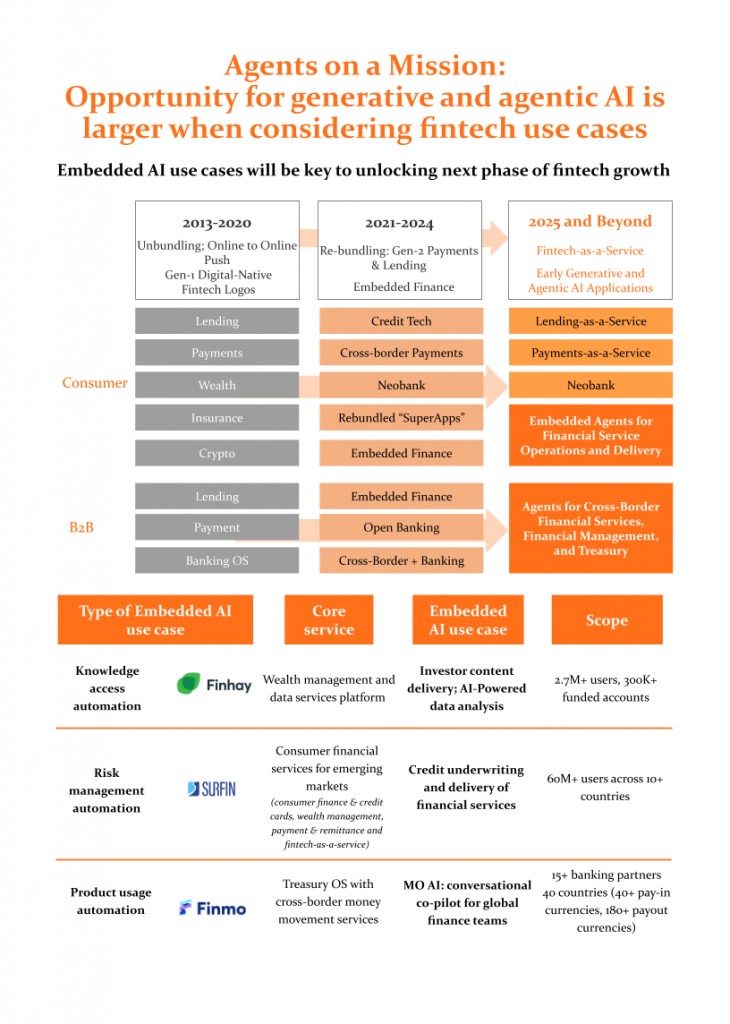

The Three-Phase Evolution: From Unbundling to Agentic Intelligence

The journey of fintech in Southeast Asia can be understood through three distinct evolutionary phases, each representing a fundamental shift in how financial services are conceived, delivered, and consumed.

| Fintech Evolution in Southeast Asia | 2013-2020: Unbundling | 2021-2024: Re-bundling & Embedding | 2025 & Beyond: Agentic AI |

|---|---|---|---|

| Consumer | Gen-1 Digital-Native Logos (Lending, Payments, Wealth) | Gen-2 Payments & Lending, Neobanks, SuperApps | Lending/Payments-as-a-Service, Embedded Agents |

| B2B | Foundational Services (Lending, Payment, Banking OS) | Embedded Finance, Open Banking, Cross-Border | Agents for Cross-Border, Treasury, & Financial Management |

This evolutionary trajectory highlights a clear progression from standalone products to deeply integrated, intelligent solutions that are predictive, personalized, and increasingly autonomous. The current phase represents the dawn of truly agentic financial services, where AI systems can operate independently to achieve complex financial objectives.

Market Dynamics: Resilience Amid Global Uncertainty

The region’s fintech ecosystem has demonstrated remarkable resilience in 2025. According to Tracxn’s H1 2025 report, Southeast Asian fintech companies raised $776 million in the first half of 2025, representing a 31% increase from the $593 million raised in H2 2024 [2]. While this represents a 22% decline from the $1.0 billion raised in H1 2024, the recovery trajectory is notable given the global fintech funding challenges.

The funding dynamics reveal a maturing ecosystem. Late-stage funding reached $558 million in H1 2025, up 113% from H2 2024 and 22% from H1 2024, indicating strong investor confidence in established players [2]. Singapore continues to dominate the regional landscape, accounting for 88% of all Southeast Asian fintech funding in H1 2025, reinforcing its position as the region’s financial technology hub.

The Embedded Finance Revolution: A Trillion-Dollar Transformation

The engine driving this transformation is embedded finance, which represents a fundamental shift from standalone financial products to seamlessly integrated financial services within existing digital ecosystems. The broader Asia-Pacific fintech market, of which Southeast Asia is a critical component, is projected to grow from $59.67 billion in 2025 to $415.42 billion by 2033, at a compound annual growth rate (CAGR) of 27.45% [3].

This growth is powered by the region’s unique demographic and technological advantages. Unlike mature Western markets burdened by legacy banking infrastructure, Southeast Asia’s mobile-first, platform-centric ecosystems have enabled a leapfrog approach to financial services delivery. Here, financial services are not merely add-ons; they are woven into the operational fabric of digital commerce, transportation, and social interaction.

The market composition in 2024 provides insight into this embedded approach. Digital Payments and Transfers dominated with 46.8% of total market volume, followed by Digital Commerce at 27.5%, and Digital Banking at 18.5% [1]. This distribution reflects the reality that financial services in Southeast Asia are increasingly contextual and embedded within broader digital experiences.

The Dawn of Agentic AI: Three Archetypes of Automation

As embedded finance establishes the infrastructure, agentic AI emerges as the intelligence layer that transforms static services into dynamic, autonomous systems. The market has identified three key archetypes of embedded AI use cases that are already gaining traction: knowledge access automation, risk management automation, and product usage automation.

Knowledge Access Automation: Democratizing Financial Intelligence

Vietnam’s Finhay exemplifies the power of knowledge access automation in wealth management. The platform has leveraged AI to create news summaries, sentiment analysis, and stock analytics that lower barriers to quality financial information. This approach has proven remarkably effective, with Finhay contributing to over 15% of new account openings in Vietnam’s market in 2023 [4].

With over 2.7 million users and 300,000 funded accounts, Finhay’s success demonstrates the market demand for AI-powered tools that democratize access to sophisticated financial analysis. The company’s recognition as the Best AI/ML Smart Investment Platform in 2023 by IBS Intelligence validates the effectiveness of embedding intelligence directly into investment workflows.

Risk Management Automation: Expanding Financial Inclusion

The challenge of credit assessment for the unbanked and underbanked represents one of the most significant opportunities for agentic AI in Southeast Asia. Companies like Surfin are pioneering risk management automation by analyzing alternative data points to serve over 60 million users across more than 10 countries.

This approach is particularly crucial in a region where traditional credit histories are often scarce or non-existent. By leveraging AI to process smartphone usage patterns, social media behavior, and e-commerce activity, these platforms can create comprehensive credit profiles that enable financial inclusion at unprecedented scale.

Product Usage Automation: Intelligent Treasury Operations

For businesses navigating the complexities of multi-currency, cross-border operations, Finmo represents the cutting edge of product usage automation. The Singapore-based company’s MO AI conversational co-pilot enables finance teams to manage real-time cash flow, forecasting, and cross-border payments using natural language interfaces.

As David Hanna, CEO of Finmo, explains, “MO AI reflects the kind of meaningful innovation we aim for at Finmo – solving real-life treasury challenges with intelligent, usable tech” [5]. The platform serves 15+ banking partners across 40 countries, supporting 40+ pay-in currencies and 180+ payout currencies, demonstrating the scale at which intelligent automation can operate.

The Road Ahead: Opportunities in the Agentic Era

The transition to an agentic AI-powered financial landscape presents transformative opportunities across multiple dimensions. The fastest growth in 2025 is projected to occur in Digital Lending, with a 40.1% increase (+$8.7 billion), fueled by increasing credit availability in rural and underserved areas [1]. This growth trajectory aligns perfectly with the capabilities of AI-powered risk assessment and automated lending decisions.

Digital Payments & Transfers will continue their momentum with 20.1% growth (+$85.2 billion), while Digital Commerce is expected to grow by 18.6% (+$46.5 billion) [1]. These sectors represent prime opportunities for embedded AI agents that can optimize payment routing, detect fraud in real-time, and personalize financial experiences at scale.

The next wave of innovation will be defined by “Fintech-as-a-Service” models, where specialized AI agents for lending, payments, and financial management become the new standard. For businesses, this means access to sophisticated, autonomous agents that can manage treasury operations, optimize cross-border transactions, and provide strategic financial insights without human intervention.

Building the Intelligent Financial Future

As we advance through 2025 and beyond, the mission for fintech innovators becomes increasingly clear: to build the intelligent, autonomous agents that will power the future of finance. The convergence of embedded finance and agentic AI represents more than a technological evolution; it is a fundamental reimagining of how financial services are created, delivered, and consumed.

The companies that will succeed in this new paradigm are those that can harness the power of AI to build more inclusive, intelligent, and autonomous financial systems. With Southeast Asia’s fintech market on track to exceed $1 trillion in 2025 and the broader Asia-Pacific region projected to reach nearly $60 billion, the opportunities for transformative innovation have never been greater.

The agents are indeed on a mission—not just to automate existing processes, but to create entirely new possibilities for financial empowerment across Southeast Asia’s dynamic and diverse economies.

References

[1] Finews Asia. “Southeast Asia Fintech Market Set to Surpass $1 Trillion in 2025.” August 29, 2025. https://www.finews.asia/finance/43896-south-east-asia-fintech-growth-unafinancial

[2] Tracxn. “SEA FinTech hits $776M in H1 2025; Singapore leads with 88% share.” July 9, 2025. https://w.tracxn.com/report-releases/sea-fintech-semi-annual-funding-report-h1-2025

[3] Market Data Forecast. “Asia-Pacific Fintech Market Size, Share & Growth, 2033.” September 16, 2025. https://www.marketdataforecast.com/market-reports/apac-fintech-market

[4] Insignia Business Review. “AI Notes #17: What We Learned about leveraging AI/ML for a smart investment platform from Finhay.” February 18, 2024. https://review.insignia.vc/2024/02/18/ai-notes-17-finhay-smart-investment-platform/

[5] Finmo. “Singapore Fintech Finmo Launches MO AI, a Conversational Co-Pilot for Global Finance Teams.” June 19, 2025. https://finmo.net/newsroom/singapore-fintech-finmo-launches-mo-ai-a-conversational-co-pilot-for-global-finance-teams

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.