The most valuable humanoid companies won’t ship robots.

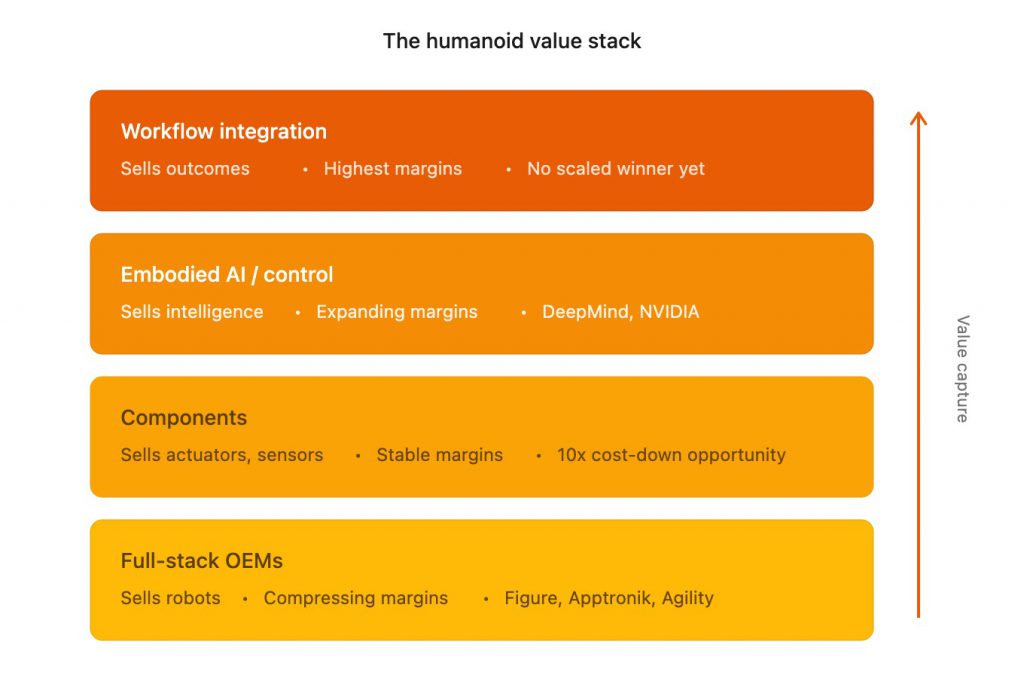

Every investor studying humanoids is asking the same question: which OEM wins the hardware race? They’re asking the wrong question. The humanoid market isn’t a race—it’s a stack. And the layer building robots is the worst place to capture value.

Hardware vs Workflow

Building a robot is hardware work. Making it useful is workflow work.

Locomotion, manipulation, object handling: the physics are hard, but they are physics. Workflow is different. It requires integration—connecting to the WMS, understanding shift schedules, fitting into processes built for people. The robot is a sensor. The workflow layer is the product.

A year ago, humanoid demos showed robots walking. Today, the deployments that matter—Digit at GXO, Figure at BMW—aren’t winning because of superior hardware. They’re winning because they’ve closed the loop: real deployments generating task data that makes the next deployment better.

In industrial automation, hardware captured most of the value. Fanuc and ABB built the robots; the software layer stayed fragmented. In humanoids, this will invert.

Exhibit 1: The Humanoid Value Stack

Where Value Accrues First

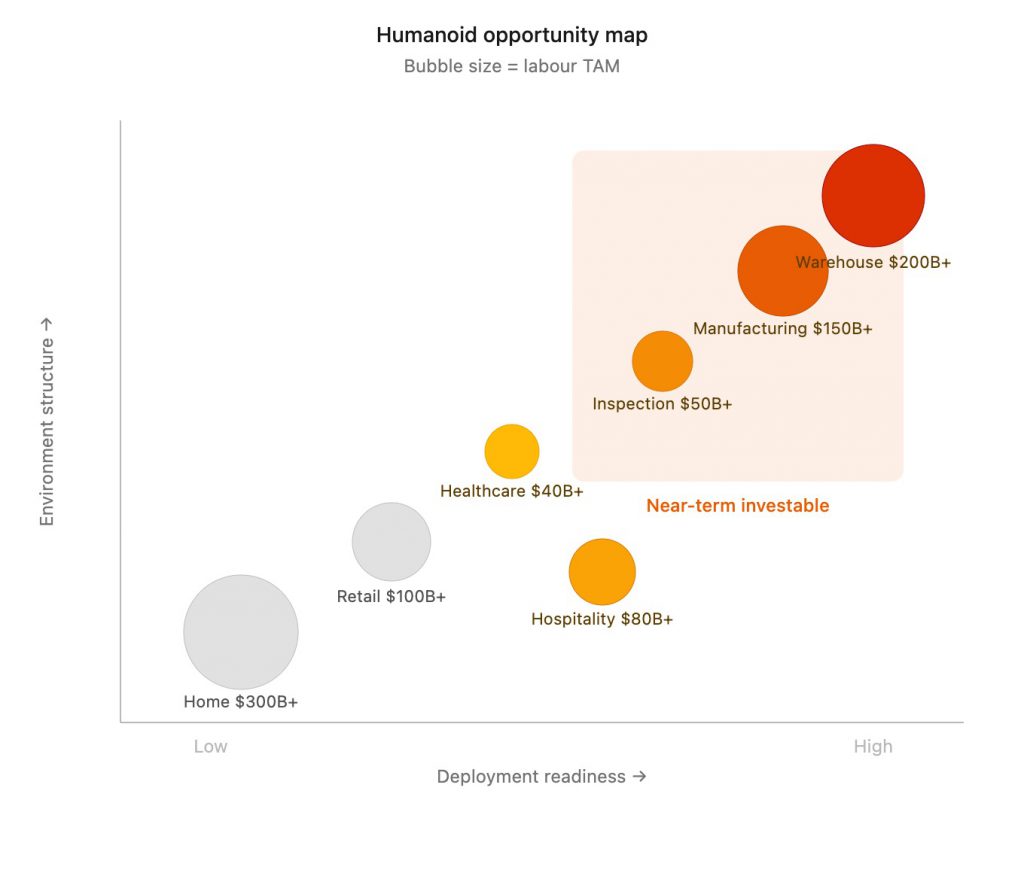

Not all workflows are equal. Plot them on two axes: deployment readiness and environment structure. The pattern is clear.

Near-term value sits in high-structure, high-readiness environments: warehouse logistics ($200B+ TAM), manufacturing material handling ($150B+), hazardous inspection ($50B+). These aren’t the most exciting applications. They’re the most fundable—because the ROI is measurable and the safety constraints are manageable.

Home assistance is the largest TAM ($300B+) but the lowest readiness. Consumer applications are years away.

Exhibit 2: Humanoid Opportunity Map

Who’s Winning

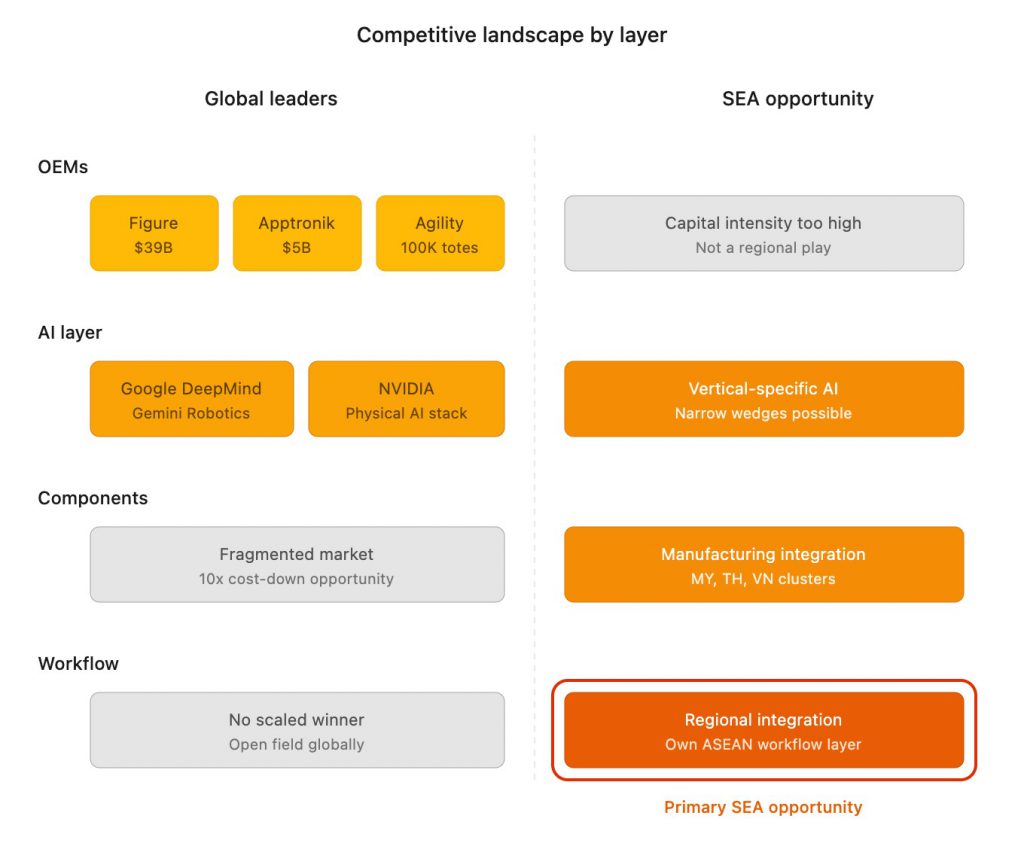

At the OEM layer, three companies have moved beyond demos.

Figure AI ($39B valuation) has the strongest enterprise positioning—BMW deployment is the clearest signal that humanoids are moving from pilots to production. Apptronik ($5B) is more commercially grounded, with Mercedes-Benz partnership focused on logistics and manufacturing. Agility Robotics is arguably the furthest along in actual commercial deployment—100K+ totes moved at GXO is the strongest public proof point in the sector.

At the intelligence layer, the elephants are moving. Google DeepMind (Gemini Robotics) and NVIDIA (Physical AI stack) are building the foundation model and simulation infrastructure that will power most humanoids. The startup opportunity is vertical-specific embodied AI—but defensibility is uncertain.

At the workflow layer, no scaled winner has emerged. This is the open field.

Exhibit 3: Competitive Landscape by Layer

The Southeast Asia Position

The region won’t produce a Figure or a Boston Dynamics. The capital intensity and talent concentration required for full-stack humanoid development don’t exist here.

But the workflow layer is wide open.

Southeast Asia has a $22B+ warehouse automation market growing to $58B by 2030. It has manufacturing density in Thailand, Vietnam, and Malaysia that global OEMs will underserve. Singapore is positioning as a reference site—HTX’s S$100M embodied AI commitment includes a dedicated robotics centre launching mid-2026.

The playbook: own workflow integration regionally. Become the company that makes global OEMs’ robots actually work in ASEAN facilities. Integrate with local systems. Build the deployment and service infrastructure that global players won’t prioritise.

That’s not a consolation prize. In a stack where hardware commoditises and intelligence consolidates, the integration layer is where regional defensibility is possible.

What We’re Looking For

Post-pilot, pre-scale. Repeatable deployments with paying customers, not letters of intent. Workflow ownership—companies selling outcomes, not equipment. Hardware optionality—can work with multiple OEMs as the market matures.

The returns in humanoid robotics won’t go to the company with the most impressive demo.

They’ll go to the company that makes the demo irrelevant.

Where do you see value concentrating—the robot, the software, or the integration layer?

If you’re building in embodied AI, humanoid robotics, or industrial automation in Southeast Asia—reach out.