This article by Insignia Ventures Head of Indonesia William Gozali and senior content strategist Paulo Joquino is the first in a three-part series on the emergence of a new wave of ecommerce enablers in this context of Indonesia’s rapidly evolving ecommerce market. Part 1 starts with a little “history” to better frame why this new wave has emerged the way it has. Part 2 (stay tuned) goes into the finer points of how startups are building these second-wave enablers and their many variations. Part 3 goes into how this wave will impact the competitive landscape and maturity of Indonesian ecommerce moving forward.

Highlights

- Because of the increasing complexity (more types of customer behaviors, transactions, and journeys) and diversity (more types of SKUs, industries) of ecommerce’s development, ecommerce enablers also have to meet evolving needs.

- With online marketplaces, simply connecting buyers and sellers would not be enough. There’s the issue of payments, logistics, as well as acquisition (or competition). So this first wave of enablers sought to solve these challenges.

- The diversification of ecommerce customers needing specific types or volumes of SKUs, diversification of still fragmented channels and enablers, as well as ecommerce volatility, have increased demand for more operations-based digital solutions, leading to the second wave of ecommerce enablers.

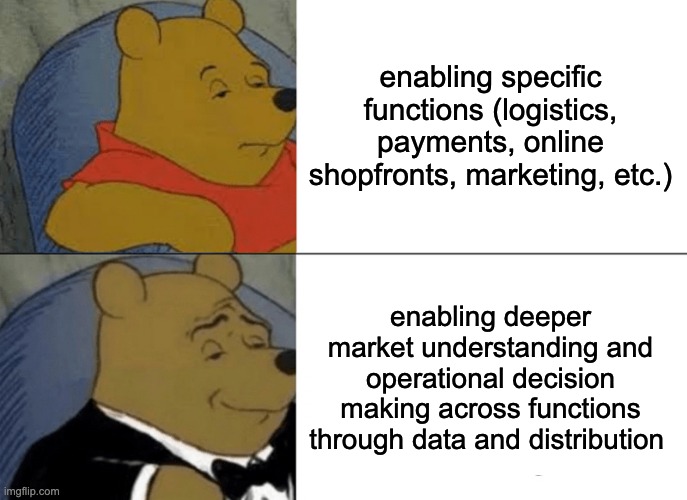

- The focus of second wave enablers is less on specific functions and more on market segment understanding through operational and financial data) and distribution ownership.

- Success for second wave enablers is measured by how deeply the success of the customers is tied to the platform.

In 2021, Indonesia’s ecommerce market ranked the ninth-largest in the world, at US$43 billion in revenue, surpassing Canada and landing just behind India, increasing by 32% from US$32 billion in 2020.

But as the ecommerce market of Indonesia grows, we’re seeing that is not just a function of end-consumer demand (i.e. they want to buy things online!) but also producers and every player in between participating in the ecommerce-first economy (i.e. all transactions facilitated online!).

Digitization is fast penetrating value chains and industries such that ecommerce platforms are not just facilitating transactions of simple two-sided B2C marketplaces but also multi-sided marketplaces, where sellers can also be buyers, and buyers can also be sellers in a large network of transactions.

Because of the increasing complexity (more types of customer behaviors, transactions, and journeys) and diversity (more types of SKUs, industries) of ecommerce’s development, ecommerce enablers also have to meet evolving needs, whether it’s for customers already using these digital products or for customers seeing the value in adopting them (the latter is an important point here we will get back to later).

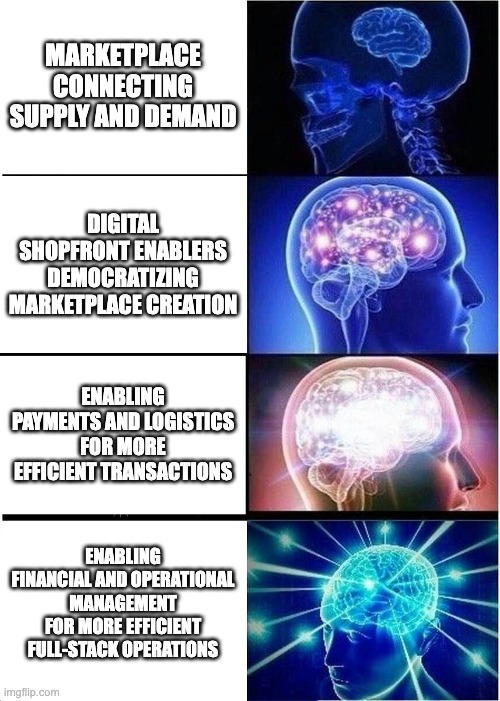

And in meeting these evolving needs, the lines are blurring between marketplaces and enablers. Some companies that started out as marketplaces may find it more cost-effective to build enablers internally or do M&A transactions to acquire the capabilities they need. Other companies that started out as enablers may be able to leverage data they acquired to eventually facilitate the connections between supply and demand themselves.

In this three-part series, we tackle the emergence of a new wave of ecommerce enablers in the context of Indonesia’s rapidly evolving ecommerce market. Part 1 starts with a little “history” to better frame why this new wave has emerged the way it has. Part 2 (stay tuned) goes into the finer points of how startups are building these second-wave enablers and their many variations. Part 3 goes into how this wave will impact the competitive landscape and maturity of Indonesian ecommerce moving forward.

First Wave Ecommerce Enablers: Keeping Buyers and Sellers on Digital Marketplaces

The first wave of enablers was born out of the marketplaces like Bukalapak, Tokopedia, Shopee, etc that emerged at the first half of the 2010s (or even earlier for some of the single-product marketplaces), connecting buyers and sellers on a single platform.

This wave was highlighted by limited SKUs on these marketplaces, mostly revolving around tickets (standardized, virtual goods), electronic gadgets (standardized, physical goods, more efficient online), fashion items (non-standardized, physical small dimension goods), furniture (non-standardized, physical large dimension goods, foods (perishable goods). The last item in this list was an opening opportunity for the likes of GrabFood, GoFood, ShopeeFood and spurred the food delivery funding wave in the latter half of the 2010s.

With online marketplaces, it was clear that simply connecting buyers and sellers would not be enough. First, there was the issue of payments. While more consumers were comfortable with cash-on-delivery, this has been (and continues to be) a longstanding pain point for sellers and even the marketplaces themselves. The roots of cash-on-delivery are not only tied to the use of “cash” per se but also the reality that many buyers did not have the credit or access to vehicles that would allow them to make alternative types of payments.

Then there was the issue of logistics, which did not just involve last-mile delivery or getting the goods to the consumer’s doorstep, but also first-mile or supporting sellers to organize and ship out orders as well as middle-mile or getting goods across provinces, regions, and even countries.

As Shipper CTO Marvinus Arif shares on our podcast in 2022, the ecommerce boom has seen increased demand for end-to-end logistics solutions, but it’s not as simple as signing on a fulfillment and delivery partner in a market as fragmented as Indonesia. As it turns out, logistics is also inherently tied to cash flow and therefore payments as well.

“When the pandemic hit, we have witnessed a strong demand for our fulfillment service, but on the other hand, not every business is prepared in terms of resources and capabilities. So two main questions emerge. One is how ready is the business for this sudden change? And the second is how long will the demand last if they decide to invest in more, let’s say warehouse capacity or building the tech capabilities in-house?

So we can see that basically, business owners need more at this time. And to answer those questions Shipper decided to strengthen two key areas. One is in integration. And then the second is pricing models.

So for any integrations, our customers can select their integrations based on their needs, so they don’t need to overinvest in something that they have already done or built in-house. The second is the pricing model where our modules come with a flexible or pay-as-you-go model that enables our clients to use Shipper with a small initial investment. So I think by focusing on those two areas, we believe that we can help our merchants to scale efficiently with less.”

Finally, there was the issue of acquisition (or competition) — how could sellers stand out in a sea of increasing online brands and SKUs to reach more customers and drive more conversion?

Bringing SKUs online is one thing, but retaining both buyers and sellers on these platforms turned out to be another affair entirely. And so this first wave of enablers sought to solve these challenges, emerging largely concurrently with the first generation of ecommerce marketplaces but only receiving massive venture capital funding in the latter half of the 2010s.

We saw the first iteration of Indonesia’s Shopify close to a decade ago in the website builder and the agencies built to help brands succeed in their online selling through channel diversification. Services include official store management, digital marketing, customer service, supply chain management and fulfillment. Back then the focus was still primarily on building omnichannel presence, visibility, and distribution.

The Challenges of Complexity and Diversification in Indonesia’s Ecommerce Boom

Now as we brought up earlier in this article, we’re seeing diversification of ecommerce customers needing specific types or volumes of SKUs. This is not just individual consumer demand, but also demand for businesses like retailers or wholesalers.

B2B textile trading platform building the OS for Indonesia’s fashion industry Wifkain CEO and co-founder Sara Sofyan shares on our podcast in 2022 the value of having a dedicated platform for the fashion industry.

“Textile itself is a very different product than all the other generic products like FMCG and everything that currently is being scaled by other startups. I think the complexity and also the detailed information in textile is very, very important, to be captured, for the consumer’s consideration to buy the items as well as for the merchant to actually manage their warehouses.

And that detailed information they’re very different from the generic products and provides a very limited available platform or technology in the market for us to use. And hence the challenge for us was to actually customize and build things that will be used and suitable enough for the merchant and the textile product itself.

The next challenge is the adoption level, because the textile suppliers are very, very, comfortable in terms of the old way of doing business, the conventional way of bookkeeping, recording, and order processing. And it becomes the strategy for us to actually onboard and activate the merchant in a progressive stage.

It’s very difficult to push them to adopt or digitize things from zero to something that is very advanced and hence the strategy will be to get the right, progressive stages, for them to be unlocked into a more advanced feature at the right time and at the right point of the usage behavior as well.

So I think that is most important. The technology itself is the enabler, but the core and also the important [thing], as well as the challenge, is to get that adoption level from the merchant side, looking into their comfort level into the old way of doing it. Once we actually get successful in digitizing them, then hopefully we also get that stickiness in terms of having comfort in using our technology.”

We reshare this quote from Shipper COO and co-founder Budi Handoko’s podcast with us in 2021, talking about how they have had to diversify their offerings as their own customer base evolved as well.

“Small businesses and large businesses that have different problems. For small businesses, their problem is actually, how do they scale up? How do they make sure that they actually focus on the marketing, focus on the sales or adding new products without worrying about the logistics piece?

Meanwhile, for the larger businesses, all they want is efficiency. They start looking into efficiency. They start looking into data integrity. They start looking into real SLA. They start looking into the satisfaction of the customer as well. So we’ve worked with different larger businesses. One of the examples is Matahari.com, where we actually manage all their ecommerce fulfillment, from our facility in Balaraja. And the metrics that we are talking about are different from the smaller sellers. And a lot of those are mostly just because they’re different business scales.

So I think besides serving these small to medium enterprises, we also serve the larger customers which require warehousing. These businesses also have two kinds of businesses: ecommerce fulfillment, which is normal traditional ecommerce, but they also have their other fulfillment, which is a B2B business. So that is also another sector where we add value to our customers, so that they actually don’t need to rent big, full warehouses for their B2B businesses. They can run a small portion at our shared warehouse, but they can still run their B2B businesses, while using our service too.”

Given this diversifying nature of consumers, there has also been a diversification of fragmented channels and enablers beyond simply setting up a digital shopfront or customer-facing marketing. These new enablers range from using better tech to scaling manual backend operations (e.g. handling cashflow and suppliers) to scaling online-to-offline touchpoints (e.g. optimizing for the right offline buyers). The competitive landscape has shifted attention towards retaining businesses on top of enablers. The value creation here is not just to digitize but to sustainably grow on top of digital sales channels.

Finally, it’s important to note that ecommerce is not a dynamic business, easily affected by inflation and seasonality, more so than most other sectors, and the impact of external factors could range significantly from SKU to SKU. This means that more sophisticated tools need to be in place to more effectively enable sellers to navigate the ups and downs of ecommerce.

At the end of the day, ecommerce growth is not just about selling goods or putting inventory online or digital marketing, it’s also about having a full stack of operations, given competition and existing horizontal platforms. Value-added services are needed more than ever before. SMEs themselves are not just selling but also buying, need to maintain good cashflow and flow of goods.

Second Wave Ecommerce Enablers: Tech Backbone for Commerce Operations

So we call this second wave of ecommerce enablers and their goals to build a full stack of support around their core offering for their target customers as the “OS or Operating Software for X” trajectory.

It’s not just stretching out a hand to help, but providing an entire backbone for running specific businesses. It’s likely less focused on specific functions like payments-only or first-mile fulfillment-only, as lines are also blurring across functions with logistics also going into fintech and marketplaces going into logistics and fintech, etc.

The focus, and therefore how these enablers are able to differentiate and build competitive advantages, is more on market segment understanding (i.e. operational and financial data) and distribution in these segments. Examples of these market segments are FMCG SMEs, wholesalers, fisheries, or even fashion businesses.

The goal for the “OS for X” trajectory is to become the “default” or “go-to” stack of tools that are essential in running a business in a specific value chain segment or industry segment. It means providing a comprehensive platform that allows businesses to run on top of it and becomes the enabling factor that unlocks growth potential. It is no longer about digitizing transactions but entire operations for businesses.

That means success for these types of growth trajectories is measured by how deeply the success of the customers is tied to the platform. Are customers growing precisely because of the operating software the company has built for them? Or is it actually hindering them or “dead weight” tech? Or are they growing because of other factors, rendering the OS irrelevant?

Wifkain’s Sara Sofyan shares the story of one of their early customer merchants on our podcast and how they enabled better access to financing. “We worked with one of our key merchants for over a year now. And before the first order when we actually worked with them, their factories were very underutilized. It’s not really good for their financial books and also the growth of the factory itself.

Once we engaged with them and we kept on building up orders with them, connecting them into a wider distribution network, now we actually already contribute almost 25% over their full capacity. So that actually unlocked an additional revenue of 25%, which is huge.

What is also interesting is that we recognize that the factories already use ERPs that can provide transparency to all parties, such as the suppliers, us at Wifkain, as well as the consumers. What’s really interesting is that the data and also the recording of information are being optimized by us and also our FinTech partners to actually provide a much richer credit assessment.

So it’s not only that the data can provide pre-approved or easier access to financing to the buyers. It also provides the opportunity of getting a lot easier working capital for the factories. So as we’re currently speaking, the fintech is currently undertaking an assessment to provide the working capital facility to the factories, which previously had very limited access to funding from any financial services companies.”

Stay Tuned for Part 2!

Of course, a tech startup doesn’t become the operating software for its target market overnight. In part 2 of “OS for X” series, we look more deeply into the strategies these startups use to ride this “OS for X” trajectory, using on-the-ground case studies from some of these “OS for X” companies in Indonesia.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.

William Gozali is the Head of Indonesia at Insignia Ventures Partners (IVP). Prior to joining Insignia, William was a founding member of two Indonesian corporate venture capital firms, MDI Ventures (by Telkom Indonesia, 2015), and BRI Ventures (by BRI Group, 2019). Working together with Indonesia’s largest telco and largest bank gave him deep knowledge and understanding on how to crack the Indonesian market.