Highlights

- “We went through the worst credit cycle in recent history and achieved a 97% recovery rate. So that’s 3% NPL in a very difficult environment. And to a certain extent, it is a testament to how fast we were able to adapt to the desperate situation, deploy our SaaS systems to control risk.”

- “Operating conditions changed dramatically in the space of one to two months and that advantage of speed, product deployment, being able to continue operating with a very substantial pivot in operational flows was one of the key highlights of our achievement there and the results speak for themselves.”

- “We look at the opportunities that the market presents to us. In 2020, the priority was very focused on risk management…Now we’re back to the original vision of digitizing the supply chain now, not only from a lending risk perspective but really now just to fundamentally capture a lot of valuable transaction data.”

- “Micro SME lending is a space that we’re going into that’s in a way, a blue ocean…what we’re doing with our banking partners is we’re opening up this new segment for them in terms of the larger SME lending…Banks simply have the lower cost of capital, but we can certainly compete on product structure and product speed specifically tailored for our suppliers.”

- “Given a lot of our painful experience with risk back in the early days, 2017 and 2018, we took a very disciplined view on risk in 2019. I wanted my team to be the FMCG risk management experts in the country before we start expanding out into different industry segments. And that really just played out for us…”

- “This is not the first time anyone’s tried to put some kind of SaaS solution into the downstream supply chain… And essentially it’s all failed because tech adoption is extremely difficult in Indonesia. And that’s why we really lead in with the low-cost working capital…And it’s the lending that actually pulls the SaaS adoption at this supplier level.”

- “Very few of these types of farm financing programs have actually worked out. And similarly the micro merchant space in Indonesia has been littered with a lot of failed banking programs. But given that we’ve solved it on the downstream, we certainly hope that we can also solve it for the upstream segment.”

- “We stayed true to the vision, knowing deep down that we should start solving the problems. And we certainly applied a disciplined approach to resolving the risk problems. Now we’re best-in-class in terms of risk management. In terms of lending capital, it’s now actually triple-digit in the millions. We certainly solved that particular supply chain issue.”

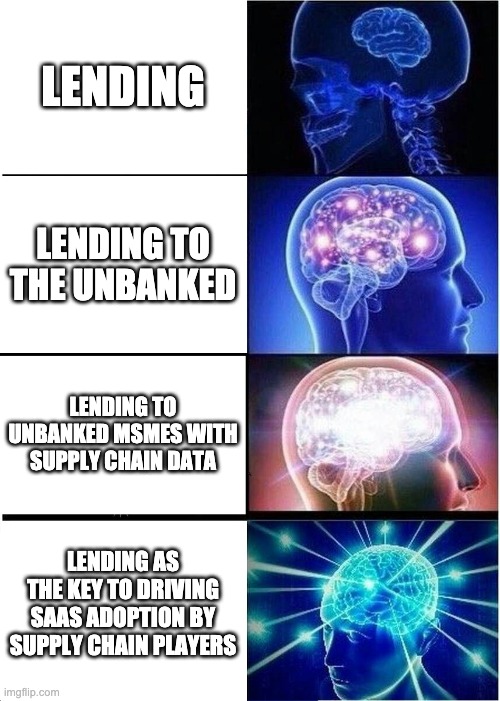

- “A lot of investors still see us as lenders, but honestly, the vision is digitizing the supply chain… It just so happens we monetize through lending because the monetization rate in lending is 20x greater than anything you can achieve on the SaaS side.”

We’re back with a returning guest, one of our very first actually, whom we had the pleasure of calling a little more than a year ago, the CEO and co-founder of Indonesian supply chain financing startup AwanTunai, Dino Setiawan. A year ago, AwanTunai was in the midst of dealing with the initial onset of COVID-19 and Indonesia, despite the difficulties of operating in the lending and financing industry, which was hit with high NPLs, Dino and his team managed to adapt quickly to the situation and turn it into a source of growth, launching several new products, extending financing to their suppliers all while keeping their NPLs low.

What’s more impressive is that they did not only grow themselves amidst the pandemic but also continued to support the growth of the micro-merchants and suppliers they serve. Now in 2021, Yinglan and I call Dino again to catch up on how they made it out of 2020 stronger than ever as a business and what they’re onto this year in terms of digitalization and SaaS adoption.

Timestamps

01:38 Dino updates on AwanTunai’s 2021 Q1;

03:41 Dino on speeding ahead their SaaS product development in 2020;

05:44 How AwanTunai prioritizes its product development and business lines;

09:20 AwanTunai’s outlook for the rest of 2021 and their relationship with banks;

12:08 Dino on sustaining high repayment rates through 2021;

14:00 Dino on lending as key to unlocking SaaS adoption for SMEs in rural Indonesia;

16:37 AwanTunai’s research on micro-farm financing;

18:08 Dino on staying true to the vision for AwanTunai’s next five years;

20:04 Rapid Fire Round;

Transcript

Yinglan: Thanks Paulo. Dino thanks for taking the time to come down to the show with us. If there was to be a winner for the prize of resilience in 2020, I have both hands up to vote for you. I think it’s been a great year. I mean, it’s a difficult year for most people, but in the course of last year you have grown your loan book multiple times, you finally got the P2P license, the full one, default rate is at an all-time low, and you have access to double-digit in millions debt line from a world-class fund. So great. And you receive a lot of awards from MAS, UNCDF, SME Finance Forum. So lots of good news around. Would love for you to bring us up to speed to what AwanTunai has been up to in the past quarter, since we had Windy on the show, you know, in December.

Dino: Hi thank you Yinglan glad to be back. It’s been an incredibly exciting year and as in times with business, sometimes luck just has a strange way of having a huge impact. As the pandemic hit, a lot of general lenders just ran into a lot of difficulties and we’re very, very fortunate to be solely focused on FMCG, basic necessities, and stable foods. So despite all the lockdowns, this particular supply chain simply stayed open — people need to eat. And out of the pandemic, what really developed within AwanTunai is a very strong focus on managing the risks.

We went through the worst credit cycle in recent history and achieved a 97% recovery rate. So that’s 3% NPL in a very difficult environment. And to a certain extent, it is a testament to how fast we were able to adapt to the desperate situation, deploy our SaaS systems to control risk. And 2020 was a difficult year. We had to cut budgets, but what we did with the budget that we had was really develop the SaaS systems to manage the risk. And that’s why we were able to grow revenues by 600% whilst maintaining a near-pristine loan book.

So one of the really exciting parts out of all this is that the team really delivered. It’s often been talked about that culture is very important and to be honest, I was a bit skeptical. I was like, “Yeah, okay. Culture is important, but you know, you read it in textbooks, you hear it in all those kinds of podcasts and TED talks.” But the pandemic was when I realized it really is important. The culture keeps the team together. The team battles for the company and that’s how we were able to really develop and deploy SaaS systems to control our risk. And now that we’re rolling into 2021, I’m very excited because of the foundations of the SaaS systems there, where we can get back to our primary original vision to digitize this whole supply chain.

“We went through the worst credit cycle in recent history and achieved a 97% recovery rate. So that’s 3% NPL in a very difficult environment. And to a certain extent, it is a testament to how fast we were able to adapt to the desperate situation, deploy our SaaS systems to control risk.”

Pivots can lead you on the right track

Paulo: Yeah, that’s great Dino. One of the words that I use to describe AwanTunai in the articles that I write is antifragile. Because given the situation that you’ve been in actually opened up opportunities for you guys to double down on digitalization. You launched AwanToko and AwanGrosir and extended financing to the wholesalers in your ecosystem — so the launching of all of these new products.

So I wanted to know how the adoption of these products has been since they launched last year and how have these products evolved as the users of these apps became more engaged. They start to spend more time on the app as opposed to doing these transactions offline. And do you have any interesting or remarkable stories from these micro-merchants or wholesalers that you work with who have benefited from these new products that you’ve launched?

Dino: Absolutely. 2020 is a testament to the true power of a startup. We were able to essentially take what was a fourth-quarter kind of a product roadmap, accelerate that and deploy it within the first quarter. And this was a physical function of our sales team shutting down.

We had national lockdowns. Our sales teams simply couldn’t be out there in the market. So we had to adapt very, very quickly in terms of how we run sales when we can’t have our field sales teams out there. Certainly, there are those that pivot towards telesales, but a lot of it was driven by us accelerating at throwing the MVP out there so that we could start operating digitally. This has always been on our roadmap, but we actually planned it more for fourth-quarter 2020, as opposed to once the pandemic hit. We just said that well, okay, non-digital sales are shutting down, so we need to get digital solutions out now and within weeks.

So that’s what I was really proud of in terms of the team. Operating conditions changed dramatically in the space of one to two months and that advantage of speed, product deployment, being able to continue operating with a very substantial pivot in operational flows was one of the key highlights of our achievement there and the results speak for themselves in terms of growing the book multiple times and growing revenue multiple times as well.

“Operating conditions changed dramatically in the space of one to two months and that advantage of speed, product deployment, being able to continue operating with a very substantial pivot in operational flows was one of the key highlights of our achievement there and the results speak for themselves.”

Paulo: Yeah given this product growth, and all of these fantastic results that you’ve just shared with us, I think our listeners would be interested to know amidst all of these opportunities that you’ve had. I think one of the difficult things that startups often have is the problem of which of these opportunities do you tap? How do you prioritize which services to roll out and which ones to launch, especially when you’re hard-pressed for time and in terms of other different constraints?

So how did you think about prioritizing your services to develop and launch on top of your financing foundation? How is Indonesia’s current situation now, in 2021, with the pandemic affecting AwanTunai’s product trajectory this year?

Dino: I’ll actually answer with a bit of an expansion on the previous question. A lot of the opportunities that we’ve capitalized on was simply that: opportunistic. With the onset of the pandemic what happened in the field was we never thought we would be providing financing to our suppliers, but as the first quarter of 2020 rolled on the banks simply stopped lending. So all of a sudden, a lot of our suppliers came to us requesting financing, and our financing was geared more towards the micro-segment.

So it’s certainly more expensive than SME bank financing and we were puzzled. Why are they coming to us? Until the feedback was that look — the opportunity presented itself. These healthy suppliers, which we have all the operational data on, their working capital supply was simply shut off. So that’s when we actually took a deeper look into the space, managed to deploy a product that’s very competitive, to the SME banking products on offer. Certainly not on pricing, but on a whole lot of other features, which actually saw tremendous growth in the second half of 2020 and even now.

And this comes back to your question in terms of how we are prioritizing. To a certain extent, we look at the opportunities that the market presents to us. In 2020, the priority was very focused on risk management. We certainly held the NPL monster bag at 3% per month in the first quarter of 2020.

And with the deployment of our systems, with our ability to spawn very quickly, post-April 2020 cohorts returned to 2019 levels. What essentially happened was in that first quarter of 2020, a lot of our micro-merchants were used to buying the same SKU mix day in, day out. And what happened during the pandemic as it hit was lockdowns changed fundamentally the consumer buying patterns. A lot of people were simply cooking at home. So there was a fairly large uplift in staple foods. And because incomes were very tight, there were a lot of layoffs. There was a real reduction in luxury goods, in cigarettes, in upper-end FMCG brands. And that’s what caused a lot of the lower performance anyway that we saw in the first quarter. Our merchants simply had unsold inventory. The good thing about our particular model is even though the inventory is slow-moving, eventually, it still sells.

So after 90 days of recovery efforts, they managed to sell off that inventory. And we ended up with a 97% recovery rate, which is tremendously outperforming the general lending sector out there. Now in terms of what we’ve been able to prioritize now, with budgets normalized, we’re back to the original vision of digitizing the supply chain now, not only from a lending risk perspective but really now just to fundamentally capture a lot of valuable transaction data. We have now reorganized our sales team to focus on merchants who may not necessarily be ready to borrow. They don’t need working capital, it’s a seasonal thing, or they may not essentially be approved by risk yet. There’s insufficient information, but with our budgets normalized, we can push for the adoption of the online orders, which capture a lot of valuable transaction data, which is then validated through the SaaS systems that we’ve now deployed within a lot of our supply network.

“We look at the opportunities that the market presents to us. In 2020, the priority was very focused on risk management…Now we’re back to the original vision of digitizing the supply chain now, not only from a lending risk perspective but really now just to fundamentally capture a lot of valuable transaction data.”

Paulo: It’s really exciting to know that you guys have gotten back on track as you said, in terms of your overall mission, really of digitalizing the supply chain in Indonesia and not just focusing on financing, but in terms of even lightweight inventory management and SKU delivery, all of those things.

And in terms of moving forward throughout this pandemic as clearly, it’s not abating anytime soon unfortunately. I wanted to talk about that in terms as well of the industry that you guys came from, which is the financing sector. And you talked a lot about how it has been a difficult time for that industry. And do you see that situation changing in 2021 this year? And you can talk a little bit how that would affect the MSMEs that you’re working with and how would that affect your core service as a supply chain financing company?

Dino: Sure. Well, across the board, we’ve seen on average, a 30% reduction in overall sales be it at the wholesaler level or downstream, even at the micro merchant level. Now we are starting to see the beginnings of some kind of turnaround within consumer spending but it’s still not broad-based yet. So frankly, the marching orders for the team is that we will assume COVID just goes on. It’d be the same for the next six to twelve months. We’re not gonna change what we did. We were still able to grow 600% in 2020, with how we were operating and we’ll simply continue that simply with the assumption that COVID continues. The bonus is should the vaccines get rolled out nationally, general economic recovery happens. That’s a bonus for us because then we’ll see general consumption pick up again. Our entire customer base will see a 30% uplift, as demand normalizes. But for now, in terms of all our budgeting, our planning, we’re simply factoring that COVID continues. How this may impact the whole micro SME market — to be honest, micro SME lending is a space that we’re going into that’s in a way, a blue ocean.

We’re not cannibalizing any of the bank markets. In fact, what we’re doing with our banking partners is we’re opening up this new segment for them in terms of the larger SME lending, certainly once the banks start opening up their financing again, and there are certainly indications of that anyway, certainly at the most senior government levels where they do want the banks to start deploying that capital even to kind of COVID impacted restructured loans. We’re starting to hear that at the most senior levels. But again, we’ve designed our product to not directly compete against the banks. I don’t see fintech’s role as competing against the banks. There’s this very large unbanked or underbanked segment in Indonesia, that’s you know, plenty of market share for all the fintechs. And that’s essentially what we focus on. We certainly don’t compete on pricing. Banks simply have the lower cost of capital, but we can certainly compete on product structure and product speed specifically tailored for our suppliers, which essentially, validates or justifies the premium in price that they pay for our financing.

“Micro SME lending is a space that we’re going into that’s in a way, a blue ocean…what we’re doing with our banking partners is we’re opening up this new segment for them in terms of the larger SME lending…Banks simply have the lower cost of capital, but we can certainly compete on product structure and product speed specifically tailored for our suppliers.”

Paulo: Right, yeah, I think it’s been interesting that the fact that you guys work in a blue ocean of sorts, actually makes it easier for you guys to be flexible in terms of how you work with the MSMEs in terms of financing.

And you’ve touched upon this already a bit, how you guys were able to work with the micro-merchants to keep repayment relatively high compared to the industry. It’s come back to 2019 levels, as you mentioned. What are your plans in terms of sustaining this, especially since you’ve mentioned that you’re still in pandemic mode this year?

Dino: Again, I’d reiterate like we got lucky. We really started our focus on FMCG back in 2019. One, it was a big enough segment: $80 billion per annum. Most of that in fact, more than 80% of that goes through the traditional kind of general trade route, as opposed to the 20% that goes through the modern retailer, which is the supermarket and modern convenience stores and e-commerce for that matter.

So it’s a very large space, very much underserved given the lack of any kind of digitized infrastructure out there. We talk about face-to-face transactions as they purchase inventory and cash payments. This is really a blue ocean that we play in. Now, we got lucky, because we actually focus on FMCG and staple foods and we were actually considering restaurants and cafes should we go into that then the pandemic hit, and clearly, that entire segment was significantly impacted adversely given the lockdowns.

And so given a lot of our painful experience with risk back in the early days, 2017, 2018, we took a very disciplined view on risk in 2019. I wanted my team to be the FMCG risk management experts in the country before we start expanding out into different industry segments. And that really just played out for us, because when the pandemic hit, we were simply in the FMCG segment, $80 billion per annum, that simply stayed open throughout all the lockdowns.

“Given a lot of our painful experience with risk back in the early days, 2017 and 2018, we took a very disciplined view on risk in 2019. I wanted my team to be the FMCG risk management experts in the country before we start expanding out into different industry segments. And that really just played out for us…”

Paulo: Yeah. You call it luck, I call it serendipity. I mean, you were lucky, but at the same time you were also prepared to really meet the fact that you are in that segment, and making the most out of it.

And Hendra, who we’ve interviewed for our first episode this season mentioned that the next wave of digitalization coming to Indonesia after the ojeks, the taxis, online shops, travel agencies, payments will be for the country’s rural merchants and restaurants or the warungs. Right and being in, I would say, a similar space, albeit from a supply chain perspective, with financing and now more SaaS solutions. How do you see this wave of digitalization evolving in Indonesia? You mentioned that it’s still a bit of a blue ocean and what are the market conditions to consider that could influence this wave of digitalization?

Dino: I definitely feel this digitalization of the micro-merchants out there is inevitable. It will happen. The issue is, well, who’s going to figure it out. Because I think SaaS adoption is tough in Indonesia. And this is why you see that a lot of the Chinese business models simply didn’t work in Indonesia. The user base is very different. This I think is where our approach is a little bit more nuanced. We leverage the supply relationships that we’ve achieved by building a fairly large supply network out there.

We’re providing our suppliers with a lot of SaaS solutions. That’s in a way driven by lending. This is not the first time anyone’s tried to put some kind of SaaS solution into the downstream supply chain. Many have tried — all the major principals, even some of the major banks that will try it. And essentially it’s all failed because tech adoption is extremely difficult in Indonesia. And that’s why we really lead in with the low-cost working capital. Everybody needs that in this particular segment. And it’s the lending that actually pulls the SaaS adoption at this supplier level. And that’s how we build our supply network. And from there, a lot of these suppliers have very tight relationships with their customers. These are like micro-merchants. And this relationship is what we leveraged because there’s already trust established there.

The micro-merchants listen to their suppliers and when we offer a much better way for the suppliers to operate, essentially digitizing a lot of their orders, where historically a merchant would write the order by hand, messy handwriting, maybe photograph that using WhatsApp and then send it to the supplier. Now it’s all essentially digitized through an app. So that simplifies a lot of the fulfillment functions that happen at the supplier. It runs through our POS system that we also provide to the suppliers. And the synergy there is when all that data starts coming into our system.

It makes those customers bankable, those micro-merchants that were historically simply not bankable due to a lack of any kind of credit history data or any kind of digitized transaction data, be it bank transfers or anything like that. Now, all of a sudden through AwanTunai become, able to access the low-cost bank capital that we deploy through our platform.

“This is not the first time anyone’s tried to put some kind of SaaS solution into the downstream supply chain… And essentially it’s all failed because tech adoption is extremely difficult in Indonesia. And that’s why we really lead in with the low-cost working capital…And it’s the lending that actually pulls the SaaS adoption at this supplier level.”

Paulo: Yeah, it’s really amazing that you guys are really working towards something that as you’ve said, a lot of people have failed to really make significant progress in and that you guys continue to see progress in that. And one of the things I think has enabled AwanTunai to make that work is really this ecosystem. Right now, it is currently composed of three parties: AwanTunai plus micro-merchants plus suppliers that you work with. One thing I was wondering is moving forward how will this ecosystem grow? Will you guys move more upstream? And what does this ecosystem look like for AwanTunai moving forward?

Dino: Well, as I mentioned earlier, for now, we’re simply under the assumption that COVID is going to be around for the foreseeable future. So we’re certainly staying focused on FMCG and staple foods. It’s still an $80 billion segment. But we do have research projects upstream. Because we do a lot of work with the United Nations, we were actually introduced to the Swiss Capacity Building Fund. So we actually have Swiss government money funding a research project to see whether our downstream financing solution works in the upstream where you get those agricultural aggregators, who source supply from hundreds of tiny micro farmers. So it’d be an amazing project if it succeeds because micro-farm financing has historically had a very difficult history. Very few of these types of farm financing programs have actually worked out. And similarly the micro merchant space in Indonesia has been littered with a lot of failed banking programs. But given that we’ve solved it on the downstream, we certainly hope that we can also solve it for the upstream segment. And that literally means millions of micro-merchants, be it micro retailers or micro farmers.

“Very few of these types of farm financing programs have actually worked out. And similarly the micro merchant space in Indonesia has been littered with a lot of failed banking programs. But given that we’ve solved it on the downstream, we certainly hope that we can also solve it for the upstream segment.”

Paulo: Now I’d like to sort of zoom out and ask you as a CEO given all of the things that you’ve been through in these past three years. And it certainly has been I would say like a roller coaster ride in terms of going through many different iterations to launch AwanTempo and then going through the pandemic and then coming out stronger than ever. And now looking forward to going back to your core mission and doubling down on that. So what are the lessons that you’ve learned as a CEO these past three years? And where do you see AwanTunai in the next five?

Dino: I really see this journey as a marathon. And then that helps your mindset because then you start pacing yourself so you literally don’t mentally burn out. Because as you say, it’s a roller coaster ride. And I think what certainly helps in keeping this vision — that there’s a vision where you’ve got your whole organization culturally bought into achieving this vision and you start solving the problems. There’s just a never-ending supply of problems out there, but what I’ve learned is we have solved — let’s say we go back two and a half years ago. What’s simply seen as insurmountable problems — we hadn’t solved risk yet, NPLs were horrendously bad back then. We hadn’t solved a source of lending capital yet. We only had one institutional lender and sales and distribution was an issue. It was almost the case that, well, okay, do we just change business models out of this, but we stayed true to the vision, knowing deep down that we should start solving the problems. And we certainly applied a disciplined approach to resolving the risk problems. Now we’re best-in-class in terms of risk management. In terms of lending capital, it’s now actually triple-digit in the millions. We certainly solved that particular supply issue. And in terms of the sales we overcame a lot of the operationally difficult conditions. During the pandemic, we set up the infrastructure that now is set for scaling in 2021. So really pace yourself, keep disciplined. You’d get there in the end.

“We stayed true to the vision, knowing deep down that we should start solving the problems. And we certainly applied a disciplined approach to resolving the risk problems. Now we’re best-in-class in terms of risk management. In terms of lending capital, it’s now actually triple-digit in the millions. We certainly solved that particular supply chain issue.”

Paulo: Right. One problem at a time. And to wrap things out, I think we didn’t get to try this the first time you were on On Call with Insignia. So this is going to be pretty new for you. So we have this new segment, rapid-fire round where we ask some quick questions and you can just fire back with snappy answers, one-liners, and the sort. So let’s get started.

Top Three Skills of a CEO?

Dino: Without a doubt, decision-making under uncertainty, patients keeping you cool, and really open, honest, genuine communication. Your team can spot you when you’re selling propaganda. You want to be authentic.

Favorite book/movie/podcast?

Dino: It’s an old one, which probably shows my age. It’s Contact, based on the book by Carl Sagan. It treated the audience with intelligence. It’s probably one of the best kinds of alien contact movies out there. No spaceships and all that, very believable, very realistic.

What’s one misconception people have about driving financial inclusion in Indonesia?

Dino: This one’s a pet peeve of mine. There are some folks out there who say that all right I’m serving the unbanked, but I’m going to charge them 500% interest. In my mind, that’s not financial inclusion.

Advice for early-stage fintech founders in Southeast Asia?

Dino: So I would say that there’s a real force multiplier here for top talent. Actually I just had a conversation with an Indonesian US graduate who was thinking of coming back and given the talent shortage in this region, having high caliber talent like that come back. You bring a real force multiplier. When I was in Silicon Valley and it was so hot, everybody came from Stanford, MIT, or Harvard. There was nothing special, but in Indonesia, wow, you can definitely achieve a lot more impact in this region.

Anything you’d like to share/promote?

Dino: A lot of investors still see us as lenders, but honestly, the vision is digitizing the supply chain. And that means having micro-merchants stop writing their orders by hand and actually going through the app, having suppliers who are again used to using pen and paper, kept very opaque books, ready to digitize, ready to become a modern business. That’s our true vision. It just so happens we monetize through lending because the monetization rate in lending is 20x greater than anything you can achieve on the SaaS side. That’s my key point: we’re digitizing the supply chain.

“A lot of investors still see us as lenders, but honestly, the vision is digitizing the supply chain… It just so happens we monetize through lending because the monetization rate in lending is 20x greater than anything you can achieve on the SaaS side.”

Paulo: I think that’s a really great point to make, especially with startups, you come to a first product-market fit, like in your case with financing, but then that’s really not the end of the road. There’s a bigger mission out there and a lot more to achieve and build and deliver to your customers.

Thanks for coming back a year later, actually the date when we recorded the first one was April 1st, actually. So it’s not that far off. Yeah. And maybe, you know, like every year you just come back on and I think that it’s a good sign that every time that you come back, there’s always something new that’s going on with the AwanTunai. It’s just a sign of growth for you guys. And having gone through the initial impact of the pandemic and coming out stronger than ever because of it, it’s definitely an inspiring story for the founders that are listening in can actually learn from and excited to see where you’re taking AwanTunai, along with Windy, who’s been on the show and been glad to talk with her as well, and then the rest of the team, as you’ve called them dedicated employees of AwanTunai. So definitely a privilege to have met you since 2019, I started covering your story. And I think that the first article that I actually wrote on our blog was on AwanTunai. And it’s come full circle sort of seeing how much you’ve grown. So definitely a privilege to have been a part of that.

Dino: Yeah. Look, I mean, not only am I grateful for a dedicated team, but I’m also grateful for Insignia as a dedicated investor.

Paulo: Thanks Dino for coming back a year later, having gone through the initial impact of the pandemic on your industry and coming out stronger than ever because of it — definitely an inspiring story the founders listening in can learn from. And excited to see where you’re taking AwanTunai along with Windy and the rest of the team. Definitely a privilege to have met and partnered with you on this journey.

About our guest

Dino Setiawan is the CEO and co-founder of AwanTunai. He is a finance veteran with more than a decade of experience spanning several countries which includes a tenure as VP for Investments at Morgan Stanley among other roles at major financial institutions. After finishing his Master’s at the Stanford Business School in 2011, he started off his entrepreneurial journey running his own fintech venture in Silicon Valley, SimpleFi, before returning to Indonesia as a regional fintech consultant. Together with ex-Gojek execs Rama Notowidigdo and Windy Natriavi, he later co-founded AwanTunai, an Indonesian fintech startup providing accessible financing to micro-merchants by digitizing the FMCG supply chain.

Dino Setiawan is the CEO and co-founder of AwanTunai. He is a finance veteran with more than a decade of experience spanning several countries which includes a tenure as VP for Investments at Morgan Stanley among other roles at major financial institutions. After finishing his Master’s at the Stanford Business School in 2011, he started off his entrepreneurial journey running his own fintech venture in Silicon Valley, SimpleFi, before returning to Indonesia as a regional fintech consultant. Together with ex-Gojek execs Rama Notowidigdo and Windy Natriavi, he later co-founded AwanTunai, an Indonesian fintech startup providing accessible financing to micro-merchants by digitizing the FMCG supply chain.