We’ve covered in numerous articles like this one just how much Southeast Asia’s startup and venture capital landscape has grown and evolved in the past year, the drivers of which we can expect to continue fuelling the ecosystem in the next few years. But with any gold rush, as the opportunities increase, so do the risks and pitfalls, and in this article, we include the latter as well as some strategic considerations of how to deal with these pitfalls.

We cover them in three areas (demand, supply, and talent), and for each we identify some key opportunities, pitfalls, and some strategies or innovation to tap into these opportunities while managing the baggage of risk that come with it. We also include a case study for two of these areas.

Select insights in the article come from interviews for DealstreetAsia’s 2021 Q4 Deal Review and with The Ken on their Indonesian logistics piece.

Highlights

If you’re looking to learn the ropes, grow your network and gain a track record of investing in Southeast Asia, Cohort 3 of Asia’s first experiential venture capital accelerator, Insignia Academy, is still accepting applications.

Or are you ready to build a career backing unstoppable founders and building great companies in Southeast Asia? Reach out to us at career@insignia.vc to apply.

The more the merrier, but also more mistakes can be expected.

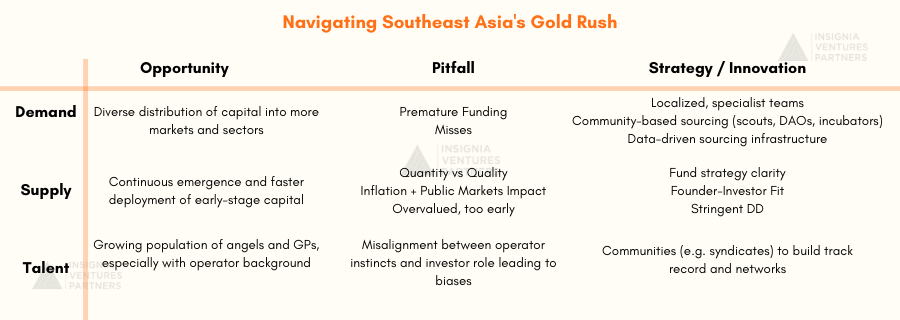

Opportunities

Diversification

- More sizable companies will continue to drive most of the contributions to this fundraising pie, but it will likely no longer be dominated by the pure e-commerce, ride-hailing, or payment plays the ecosystem has seen raise mega-rounds in the late 2010s.

- While Singapore and Indonesia can be expected to continue leading the fundraising pack, we also see Vietnam and the Philippines adding more to the pie (the drivers of which we wrote about here for Vietnam and here for the Philippines).

- Beyond the usual suspects of e-commerce and fintech, we also expect the continued growth in fundraising in the so-called “sunrise” sectors: SME enablers, Asia-first healthcare, and web3.

Verticalization

- In commerce, more startups in the region will emerge to cater to more specific market segments (e.g. parents).

- Internet economy/digitalization enablers will also verticalize as they race to create full-stack ecosystems or “operating software” for their target customers.

Infrastructure

- Moving forward, the O2O interface of most user experiences in Southeast Asia’s internet economy faces more capacity and efficiency issues as both users and tech companies come into the fold.

- This brings to the forefront of venture-backed scalability the work being done by infrastructure startups (e.g. open finance, agent-based networks, logistics/supply chain value propositions, cloud storage and data processing) as demand for their solutions increases exponentially.

- This also applies to web3 as more on-chain, consumer-facing use cases evolve the need for off-ramp, on-ramp interoperability becomes more compelling.

Liquidity

- With the increasing long-term upside of holding on to investments in tech companies even as they go public, VCs have been exploring ways to create more flexibility for them and their investors/LPs to keep investing (or not) in these companies, primarily decoupling the ability of the VC fund to invest in companies from the expectations and commitments of LPs (e.g. The Sequoia Fund).

- Another exposure to liquidity that is gaining traction is direct investments into cryptocurrencies or crypto funds. Traditional VCs in particular have had to learn (in many cases, the hard way) to adjust their fund structures to invest in these ventures, from token sales and air drops to crypto-native funds and a mix of these various strategies.

Pitfalls

- There is the tendency to make investments without fully understanding the ins and outs of the sectors, simply to catch the train before it leaves the station.

- On the other hand, having too much knowledge or experience in a sector could build up some “grass is greener on the other side” mentality that exposes one to potentially sizable misses as well.

- There’s the risk of running afoul of regulatory compliance especially through exposure to more unregulated assets.

Strategic Considerations

- It’s all about building up visibility and top-of-funnel through local investment teams and data-driven sourcing especially in an environment where cross-border travel is cumbersome.

- Specialist teams with operator backgrounds will be in greater demand to quickly bring firms and funds up to speed with fast-emerging, previously niche sectors or to bolster portfolio growth as early-stage companies verticalize getting into growth stages.

Mini-Case Study: Logistics as Gateway to Verticalization of SME enablers

Logistics as a venture-backed space in Southeast Asia has boomed in recent years thanks primarily to the increased demand for ecommerce services. While logistics as an industry is not confined to ecommerce alone, from the venture capital view in Southeast Asia, the thesis has largely been that logistics is an enabler for ecommerce. By backing the digitalization of logistics, we are investing as well in the maturity of ecommerce, in particular the capabilities of the supply side of ecommerce to meet the expectations of customers. Investing in logistics effectively grows the pool of brands and businesses that are then able to tap into this demand for low-cost but highly efficient deliveries.

Compared to other industries, scaling in the logistics industry in a highly fragmented market or region, especially as it involves offline components across multiple locations, can cost more and thus require more funding. Consolidation is also an eventual progression for logistics as it is digitalized and pain points are addressed, which leads to more concentrated funding. That said, logistics in Southeast Asia is still miles away from Amazon-level in terms of speed and scope, especially outside of metropolitan cities and urban areas.

As more logistics startups have emerged in the market, we’ve seen a progression from more new players in the last-mile to more new players in the first-mile segment. The momentum has been largely moving upstream, from serving end-customers to serving businesses. End-customers have typically been easier to convert to digital adoption, but the pandemic has forced digitalization onto the table for many businesses, and this includes logistics management as well. At scale, logistics tech startups can be expected to cover more and more of a good’s journey from seller to buyer, not just for the sake of doing so, but because it contributes to retaining and growing with their customers as well.

While we have invested in a range of logistics startups, the underlying focus has always been to find startups that are able to build networks fast, whether that means acquiring customers, securing partnerships, or building out capabilities. Scale as an asset-light logistics startup is all about leveraging owned networks. Owned networks can unlock new revenue streams and flywheels more easily, as Shipper has progressed from first-mile 3PL aggregation to microfulfillment and then warehousing as well. From a leadership network, we also need to invest in founders who have either the prior experience and credentials or existing industry network to tap into as they build the network for the business as well.

Read more about Shipper’s network approach to scale in this case study

Becoming an ecommerce enabler or a full-stack logistics provider is not mutually exclusive, though of course it is magnitudes easier said than done. Consolidation will be the name of the game as logistics startups scale; we can expect more acquisitions over the next decade by both startups looking to capture the whole value chain and traditional players looking to digitalize. From a technology standpoint, just as fintechs rebundle services to become full banking propositions or finance operating software for their customers, an important component for these logistics startups at scale will be to unify the various aspects of their (offline) logistics stack with their own “operating software” for logistics.

Similar to how ecommerce has evolved from generalist marketplaces to specific verticalized platforms and D2C, we can expect that logistics will also verticalize as more startups address the specific pain points of supply chain inefficiencies in different sectors. We can also expect the flywheel of services around logistics to expand, especially in terms of financing or insurance, and more layers of digital infrastructure to be built on top of the basic management software as more digital data becomes available in the industry.

Southeast Asia is the gift that keeps on giving, but too much of anything can lead to problems

Opportunity

- The Southeast Asia bandwagon has become its own thing. Competition for investments has undoubtedly increased thanks primarily to the success of regional unicorns and tech startups from the region that went public, strengthening the growth narrative of Southeast Asia’s internet economy. This narrative may not be so sustainable given the ongoing slump of the public markets compared to its record bull season in 2020 and 2021, but the magnetic pull of the region or the “Southeast Asia bandwagon” is already there for investors and has become a thing of its own separate but not entirely unaffected by public market performance.

- Early-stage startup investors increasingly comfortable with remote/arm’s-length investing (especially those with sizable funds and more widespread allocation). This growth trajectory has been met with newfound ability and willingness of global investors to make investments almost entirely remotely and more investors like family offices or late-stage funds previously not so active in early stage investing also making early commitments.

- We’ve all seen the clamor of global investors to lead sizable rounds of some of the big and fast-emerging players across categories. There’s also been more early-stage investment activity from family offices, late-stage funds, and global angel syndicates that had not been as active in the region or in early-stage investments before.

- Early-stage investments /can/ close much faster today mainly because early-stage startups have more options to reach their target raise or even get oversubscribed and geography is not as much of a challenge as it was before. Whether or not these funding sources are quality enough for the business or the right fit for founders’ markets is another discussion entirely.

- Regulators across the region have played a key role in this surge, including incentivizing more investors to set up shop locally or founders to explore previously unregulated sectors (i.e. sandboxes for licenses).

- Given that new funds continue to be raised and more foreign funds are progressively taking interest in Southeast Asia, it is unlikely that funding will dry up significantly.

Pitfall

- The increasing demand and supply of early-stage capital forces the question of quantity (allocation more across a market) vs quality (allocating more along a company’s growth) for early-stage investors: which strategy aligns best with the capabilities / advantages of the firm vis-a-vis the common goal to generate outsized returns? That said there are firms that have the fund bandwidth to do both.

- The public market slump (driven primarily by rate hikes) could see some of the more late-stage investors slide away from early-stage risk and push, and the inflation could also adversely impact revenues and runways for specific sectors as well, forcing a 2020 dejavu moment where bridge rounds or flat rounds become high in demand.

- The stakes are higher for failure when startups are overvalued too fast vis-a-vis their capabilities to scale. If the business is able to catch up, then all is good and well, but in the more likely case that it is not, then things could easily fall apart. It will not affect investors with a larger spread as much but other funds may have to make some tough decisions long-term.

- Given the amount of oversubscribed rounds and valuation markups in early stage rounds over the past year, there’s also the risk of growth post-Series A to slow down and less because of any gap in the funding value chain but more of an inability for these growth stage investors to participate.

Strategic Considerations

- It becomes more important than ever to have clarity with fund strategy (going back to the pitfall mentioned earlier of balancing quantity vs quality). It’s also less about investing in the best startup and more about being the right investor for the best startup.

- Just as discussion amidst the fallout of WeWork’s initial IPO attempt revolved around greater scrutiny and focus on paths to profitability, inflation and public market slumps are reviving this discussion. But the truth is these considerations should never really leave the table. After all, the best place for companies to raise money from is their customer base.

As more operators and unicorn mafia become first-time angels or GPs, community is key to reduce the risks

Opportunity

- When it comes to talent growth, there is a maturing of the talent pool in the ecosystem, in terms of both founders and operators driving the rapid growth of their companies. These startup leaders are coming from a variety of backgrounds, from the region’s growing unicorn mafia to the corporate leaders bringing their operational abilities into the startup world.

- Given the record number of startups that raised unicorn rounds in 2021 or even crossed into the hundreds of millions in valuation, there’s clearly a growing pool of startups that have reached the kind of growth that’s attractive to both regional and global investors, or that have unlocked untapped value in fast-emerging sectors (e.g. crypto) that these same investors have been looking to dive into.

- The cycle of unicorn creation also puts Southeast Asia in a period of time where there are a lot more first-generation (2010s minted) unicorn mafia who are not just looking to start companies but also angel invest or shift to venture capital.

- Population of operator investors and operator partners in the region can only be expected to increase as the ecosystem matures.

Pitfalls: For fresh operators or founders going into investments, it’s easy to conflate operator instincts with one’s investor role, which could lead to heavy biases (e.g. coachable founders vs independent ones, grass-is-greener mentality, etc.)

Considerations

- Collaboration is key and we can expect the formation of more syndicates, funds of funds, and platforms to accommodate a diversity of operator expertise looking to invest. Even DAOs are not out of the question as a tool for operators to also back on-chain projects specifically.

- More first-time or aspiring investors will be looking for communities to build track record

Case Study: Scout programs are not enough

In Southeast Asia we realized that simply recruiting scouts and connecting with angels is not enough, as we write in this article on Insignia Ventures Academy. The ecosystem’s depth of local investor talent and connectivity is not yet as mature as the likes of Silicon Valley was when Sequoia first introduced their scout program in the early 2010s. This realization contributed to our decision to start Insignia Ventures Academy as a way to nurture and support the next generation of angels and venture capitalists as they build their track record and experience in investing.

Read more about Insignia Ventures Academy

It started as a 12-week program to deep dive into the world of venture capital but has since also expanded into a community that has been valuable for us not just as a way to gain visibility into the growing pool of startup founders, but also a source of leadership talent for our firm and even our portfolio companies, given the predominantly corporate, finance, and tech backgrounds of our participating venture fellows. The potential for Insignia Ventures Academy as a program and community goes beyond the traditional scout program.

If you’re looking to learn the ropes, grow your network and gain a track record of investing in Southeast Asia, Cohort 3 of Asia’s first experiential venture capital accelerator, Insignia Academy, is still accepting applications.

Or are you ready to build a career backing unstoppable founders and building great companies in Southeast Asia? Reach out to us at career@insignia.vc to apply.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.