Over the past five years, we’ve seen how the emergence of massively adopted horizontal (meaning product-agnostic) ecommerce marketplaces in Southeast Asia has sped up the process for these more vertical-specific or customer-specific players to emerge, enabling both (1) consumers to be more comfortable using digital platforms and more demanding when it comes to their digital experiences and (2) founders to spot areas where these big players are not able to optimize for customer experience and market education (because the scope of these marketplaces is so large).

This verticalized approach goes beyond the purely transactional ecommerce approach dominated by horizontal platforms, which has either proven (1) ineffective or impractical for the SKUs (like cars or property) or (2) insufficient for the target customers (like women’s healthcare products or rural Indonesia FMCGs). It often involves catering to the whole customer journey (pre- and post- transaction) or capturing adjacencies like logistics or market education that are ultimately the root of customer pain points.

What makes this evolution exciting for us as venture capitalists is that there continues to emerge in Southeast Asia areas or needs where the verticalized, digital-first platform is best suited to tackle pain points.

And no two verticalized platforms are the same. While we’ve covered this particular emergence in the past many times over, but this time around we cover in this article how the trajectories of these verticalized commerce platforms differ from each other and to some extent, are actually evolutions of each other, largely in response to both the gaps opened up by the horizontal marketplaces and the unique needs of their target SKUs or market segments.

In particular we cover four trajectories we’ve seen in some companies in the region:

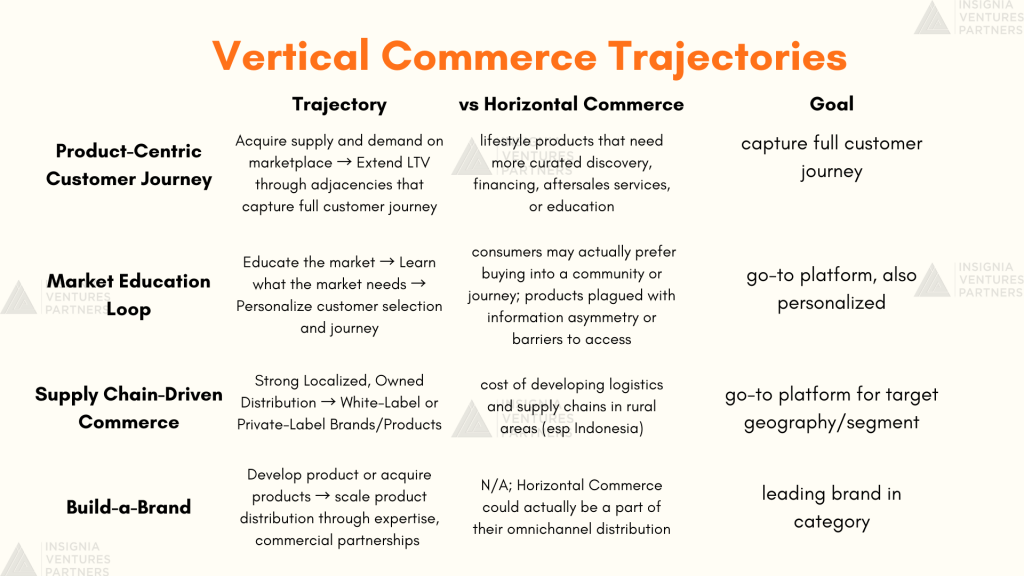

- Product-Centric Customer Journey: Acquire supply and demand on marketplace → Extend LTV through adjacencies that capture full customer journey

- Market Education Loop: Educate the market → Learn what the market needs → Personalize customer selection and journey

- Supply Chain-Driven Commerce: Strong Localized, Owned Distribution → White-Label or Private-Label Brands/Products

- Build-a-Brand: Develop product or acquire products → scale product distribution through expertise, commercial partnerships

Trajectory 1: Product-Centric Customer Journey

Acquire supply and demand in marketplace → Extend LTV through adjacencies that capture the full customer journey

This trajectory primarily addresses the reality that some products just can’t be sold effectively on generalist marketplaces and are best offered on dedicated platforms. There are products that revolve around needs that cannot just be solved by quick “add to cart” purchases (e.g. books) or multiple purchases at scale (e.g. groceries). Certain lifestyle products (e.g. property, vehicles, insurance) are best offered by marketplaces that are fully dedicated meeting the specific needs of consumers around these products. These needs could include more curated discovery, financing, aftersales services, or education.

These vertical platforms start first with a marketplace to capture distribution and users, before tackling adjacencies to extend customer lifetime value vis-a-vis acquisition costs (which can tend to cut on margins in a pure marketplace play).

From a monetization perspective, these adjacencies are brought in to not only increase margins and revenues, but also reduce operational costs (e.g. using AI or ML or data analytics to speed up discovery and create greater access to financing that lowers barriers to acquire customers).

The goal for these platforms is to simplify the whole transaction process around these specific products, starting with discovery (for buyers) or listing (for sellers, suppliers, partners) then the actual transactions, and finally the post-transaction customer experience.

Examples:

Carro: started primarily as a used car marketplace but quickly evolved into an end-to-end platform covering multiple lines of business (B2B, C2C, B2C), as well as financing and aftersales businesses

Pinhome: started with a property transaction platform that now includes data analytics-powered discovery, financing and home services

Beyond commerce, this trajectory is also employed by startups looking to build full stack ecommerce enabler software, especially in niche industries where they need to amass data and distribution before introducing more software features or digital tooling.

Trajectory 2: Market Education Loop

Educate the market → Learn what the market needs → Personalize customer selection and journey

This trajectory builds on the reality that for certain products and services, consumers may actually prefer buying into a community or journey rather than individual products. This applies especially to beauty, fashion, education (supplementary), and health (prescription-less) products, where trusted experts and influencers are sought after to guide consumer decisions.

These platforms often have to focus on market education first or heavily alongside the commerce piece through content, thought leadership, community engagement, institutional parnterships, etc. This builds trust in their platform that it can indeed help consumers overcome certain information asymmetries or cultural stigmas surrounding the product or service.

These vertical platforms typically position themselves as “partners”, and this is something that horizontal marketplaces may have difficulty venturing into given the amount of market understanding and resources this requires (essentially setting up a whole business unit around a specific set of SKUs).

Because of this positioning, these platforms revolve less around a single product (as is the case for the first trajectory), but around a single experience (e.g. women’s health journey, parenthood, schooling) where it is possible to have multiple types of products.

The holy grail for these platforms is typically to cover as much of this experience as possible in its shapes and forms and hyper-personalize customer experience. This is where the concept of “market education loop” comes in.

With the platform educating the market on the products and how it relates to the target experience, they are building a relationship with customers that then educates the company on what is best to sell or prioritize in terms of introducing products or services on their platform.

These platforms also ultimately reduce cognitive load of the customers (and the status quo for these journeys are often characterized by stress).

Examples:

Prior to the launch of Singapore femtech Ease Healthcare’s app and services in the Philippines, they started with building a brand and community in the country, gaining exposure and partnering with key organizations and institutions

Before launching ecommerce services, Tentang Anak invested in building content and community on their app to get a better sense of what Indonesian parents were looking for their children and become a trusted brand in their growing user base of parents

Trajectory 3: Supply Chain-Driven Commerce

Strong Localized, Owned Distribution → White-Label or Private-Label Brands/Products

This trajectory builds on the lack of ecommerce penetration for specific goods in second-tier, third-tier cities and rural areas (especially in as large of a market as Indonesia), due to lack of infrastructure and monopolies in distribution increasing costs of even basic goods as well as the inconvenience that arises as these goods go from producers and suppliers to end consumers.

The battle here isn’t won on frontend customer experience but the backend or the supply chain efficiency. This means these vertical commerce platforms have to be able to build asset-light or low-cost strong distribution networks in their target markets. This stands in contrast to generalist marketplaces which may need to leverage a lot more resources in order to build out their own in-house distribution.

The goal of these platforms is to replicate this distribution network across cities and markets while also introducing their own white-label products into this network, becoming similar to the “supermarket model” sans all the store infrastructure because there’s either a digital-first and social or localized element to the network that doesn’t necessitate the same kind of customer experience we are used to in the traditional supermarket or department store.

Examples:

This agent-driven, localized supply chain is social commerce platform Super’s backbone, and powers more competitive pricing and better access to goods along with their group buying approach. Super has since launched two white-label brands and looks to do more following their Series C round.

Dishserve launched with a dark kitchen distribution network to take care of last-mile operations for F&Bs (packaging and heating), which has since opened up opportunities in terms of data and distribution for them to launch private-label brands.

Trajectory 4: Build-a-Brand

Develop product or acquire products → scale product distribution through expertise, commercial partnerships

This trajectory, instead of building dedicated marketplaces or tackling distribution in a way that horizontal marketplaces are unable, are instead focused on innovating the actual products or brands themselves. Rather than filling in a gap posed by the horizontal marketplaces, as is more of the case for the first three trajectories, this trajectory plays a different game altogether.

Their advantage is less in the innovation of the marketplace or innovation in distribution, but the innovation of the product and brand itself.

So these are often D2C brands or brand portfolios that aren’t as concerned about any particular type of sales channel as opposed to simply being as available as possible to as many channels as it makes sense for the business and the brand in question.

These vertical commerce businesses are still vertical in the sense that they are still focused on specific SKUs or specific market segments, but they differ from the previous three in that these companies have built-in expertise on the products or brands they are developing or the market segments they are targeting.

The goal of these businesses is for their brands to lead in the market — easier said than done as the challenge lies in really developing an omnichannel presence, which would involve investing in or building relationships with commercial partners,

Examples:

Float Foods recently launched their flagship brand of alternative protein whole egg OnlyEg, and they have since been partnering with chefs and restaurants to drive brand awareness and consumption of their brand, beyond purely selling egg products.

igloocompany, and in particular, their consumer brand, igloohome, grew to a global presence in over 100 countries through key distribution partnerships.

Rainforest, an ecommerce aggregator, is supporting the brands it acquires to scale and reach more moms — the market segment their portfolio of brands is centered around — through a combination of marketplace, financing, technology, and brand scaling expertise.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.