Author’s Note: This is the June edition editorial of our monthly Insignia Insights Newsletter. Sign up to our newsletter.

We’re halfway through 2023 and it’s clear from the numbers that have come in that funding has slowed, with Q1 dipping to a two year low (~2.0B in 2023 vs ~2.4B in 2020 and ~3.5B in 2021 (numbers from our public access private markets stats tool)), then the first half of 2023 marked funding down 65% to $4 billion compared with the first six months of 2022. Not to mention word of SEA Group’s investment arm closing shop reflecting this reality.

“Slowing down” in the startup and venture capital industry is often seen as a bad sign, but it can present an opportunity to re-focus and re-assess. Even the fastest cars need to decelerate for a moment to change direction or switch gears. With that in mind, we list down some numbers tied to “gears being switched” in the ecosystem that have emerged this H1:

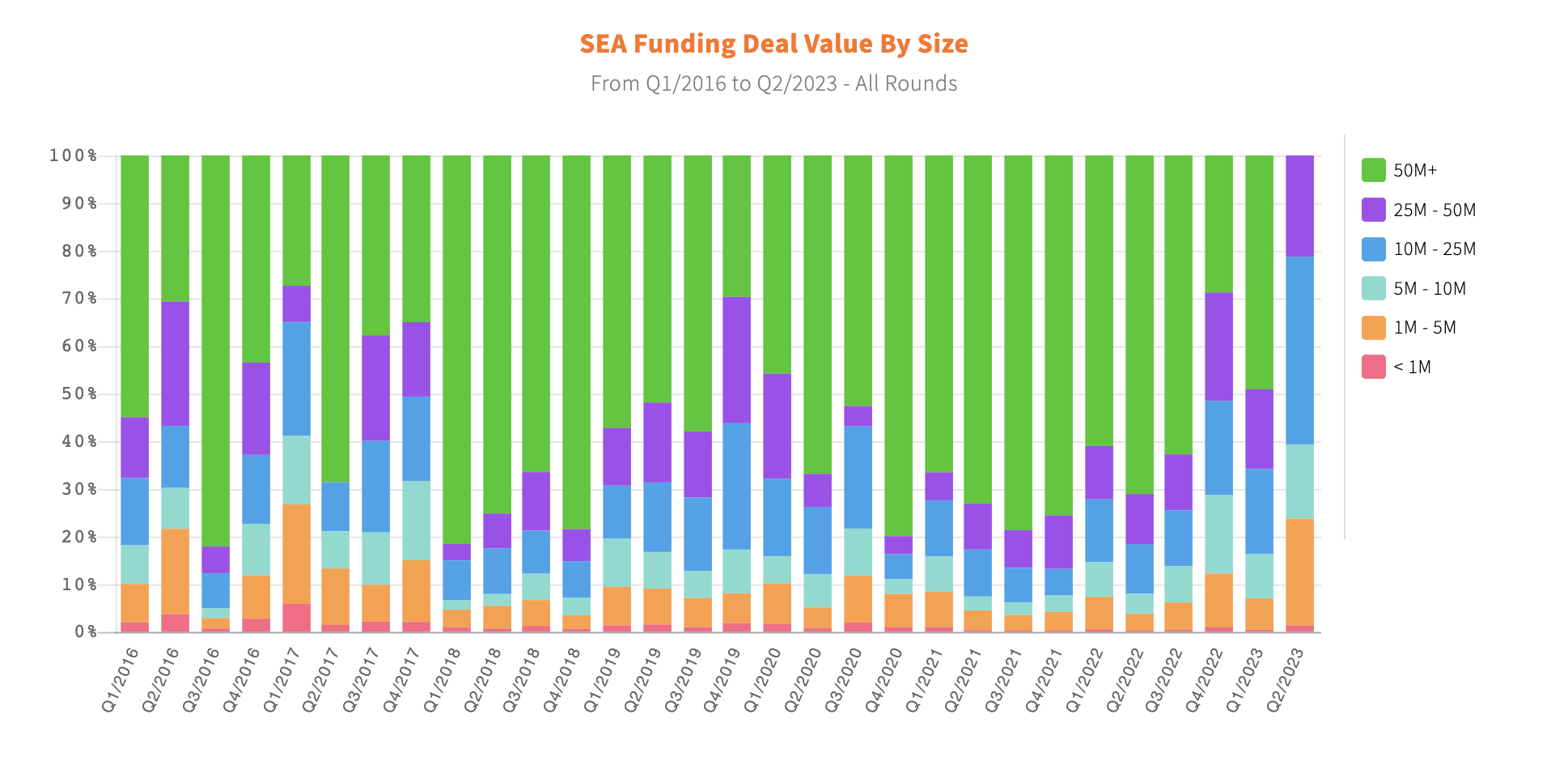

(1) 22.45%: Switch to early stage. According to our private markets stats tool (see exhibit below), this represents the share of US$1 to 5M range out of private funding rounds (roughly 70M USD) for Q2 of 2023, the highest it has been in a single quarter relative to other ranges since 2016. This points towards stronger activity in earlier stages as investors look to ride the cyclical nature of the markets and find the best companies to unlock the potential of the next bull market. Interestingly, the same could be said for the US$10M to 25M range, which could account for downsized growth rounds or bridge rounds.

From our public access private markets statistics tool: https://www.insignia.vc/private-market-statistics

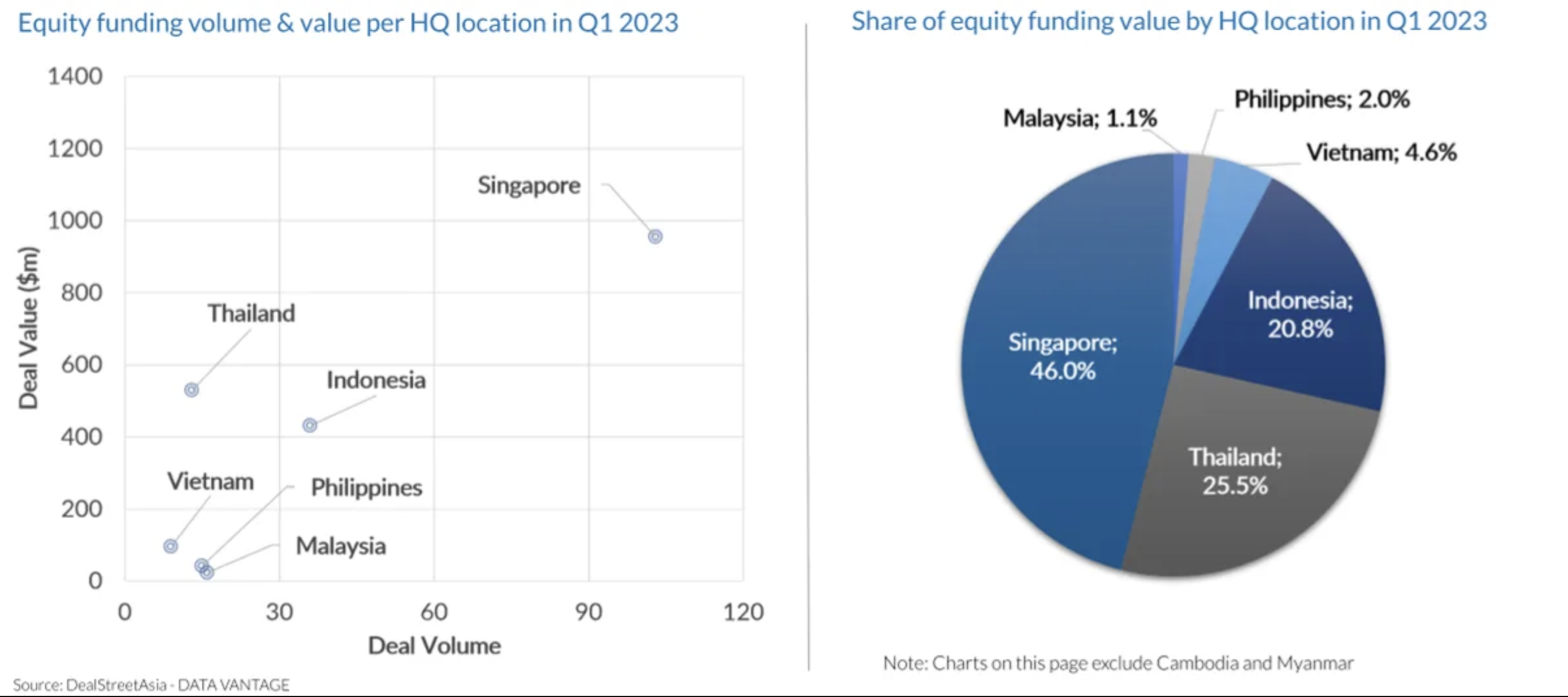

(2) 25.5%: Switch out of Indonesia? According to DealstreetAsia’s Q1 report, this represents Thailand’s share of equity funding value by HQ location (vs SG, VN, ID, PH, and MY). It’s noteworthy because it beats Indonesia’s 20.8% for the first time. As this only covers a single quarter, it is likely that the tighter deployment of capital and higher standards of investors are stretching out fundraising cycles in Indonesia. While this won’t take the spotlight from Indonesia (thanks market size), it does spread out the interest to other ASEAN markets where local companies might be looking to expand regionally or globally.

From DealstreetAsia’s SE Asia Deal Review Q1 2023: https://www.dealstreetasia.com/stories/se-asia-funding-q1-2023-340955

(3) 14x: Switch to data ecosystem play for moats and profitability. The growth in data capture by supply chain financing AwanTunai’s ERP platform since 2021. While a unique example, the success they have seen leveraging this data capture to lend over hundreds of millions of dollars to MSMEs, in an industry that has long been plagued by financing challenges even by tech players, points towards quality data sets and data ops as an increasingly important moat for companies. This is especially the case for companies looking to effectively tap into AI to automate and scale operations and value propositions.

Another example: In Carro’s latest statement on its financial results for FY 2023, management pointed towards ancillaries as a key driver for profitability (financing, insurance, aftersales) — ancillaries that were possible to unlock thanks to quality data sets on car transactions, driver behavior, etc. acquired and analyzed by AI.

(4) >48 Million: Switch to SEA’s young demographics for global jobs. With a population of 97 million, Vietnam has more than 50% under the age of 30. This youthful demographic poses opportunity for talent, with the government targeting to create 1.3 million IT jobs by 2025. This article by HR platform Recruitery goes into how markets like Vietnam continue to show potential for APAC jobs amidst cost-cutting, with examples from global companies like Bosch and Samsung moving their engineering and R&D to Vietnam. This continues a theme that has been going on since before the pandemic, with supply chain diversification followed by talent redistribution.

Editor’s Note: The content of this article is for informational purposes only, should not be taken as legal, tax, or business advice or be used to evaluate any investment or security, and is not directed at any investors or potential investors in any Insignia Ventures fund.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.