Amidst headwinds in the global economy (we’re never getting tired of that word), Southeast Asia (SEA) continues to present a unique blend of challenges and opportunities for venture-backed startups and venture capital.

This article dives into these challenges and opportunities, from shifts in capital and talent flows, the changing dynamics and demands of fundraising, and innovations shaping the way companies of the future are being built.

As SEA becomes an increasingly attractive hub for entrepreneurship and investment, understanding these dynamics is crucial for building resilient companies.

Author’s Note: The following insights are taken from Yinglan Tan’s keynote presentation at the Techsauce Global Summit 2023.

Venture Capital POV on ASEAN Today: Still Ripe for Opportunity

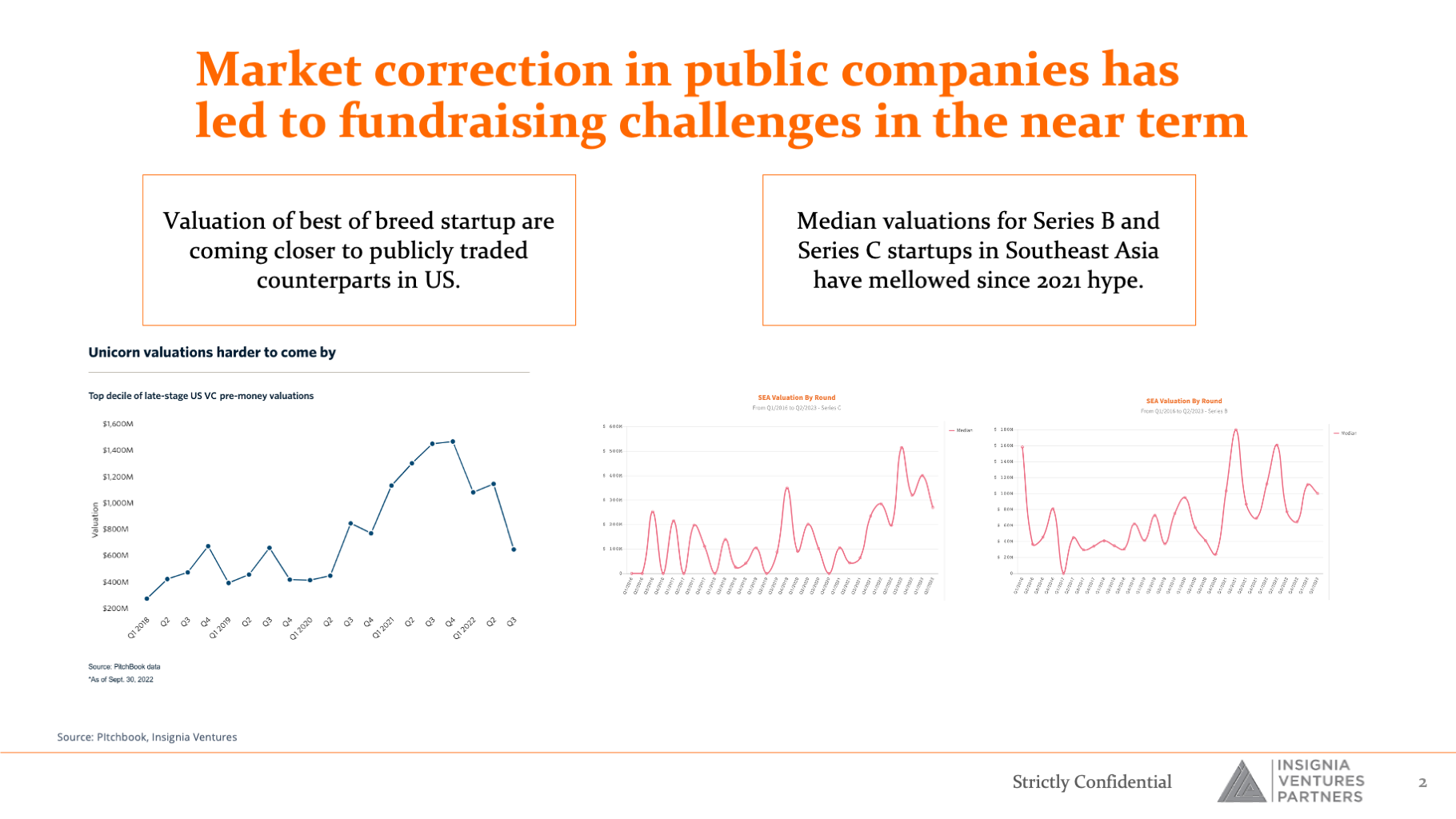

Market correction in public companies has led to near-term venture capital fundraising challenges.

The valuations of top-tier startups are now aligning more closely with publicly traded counterparts in the US. Median valuations for Series B and Series C startups in Southeast Asia have cooled since the hype of 2021 (Exhibit 1).

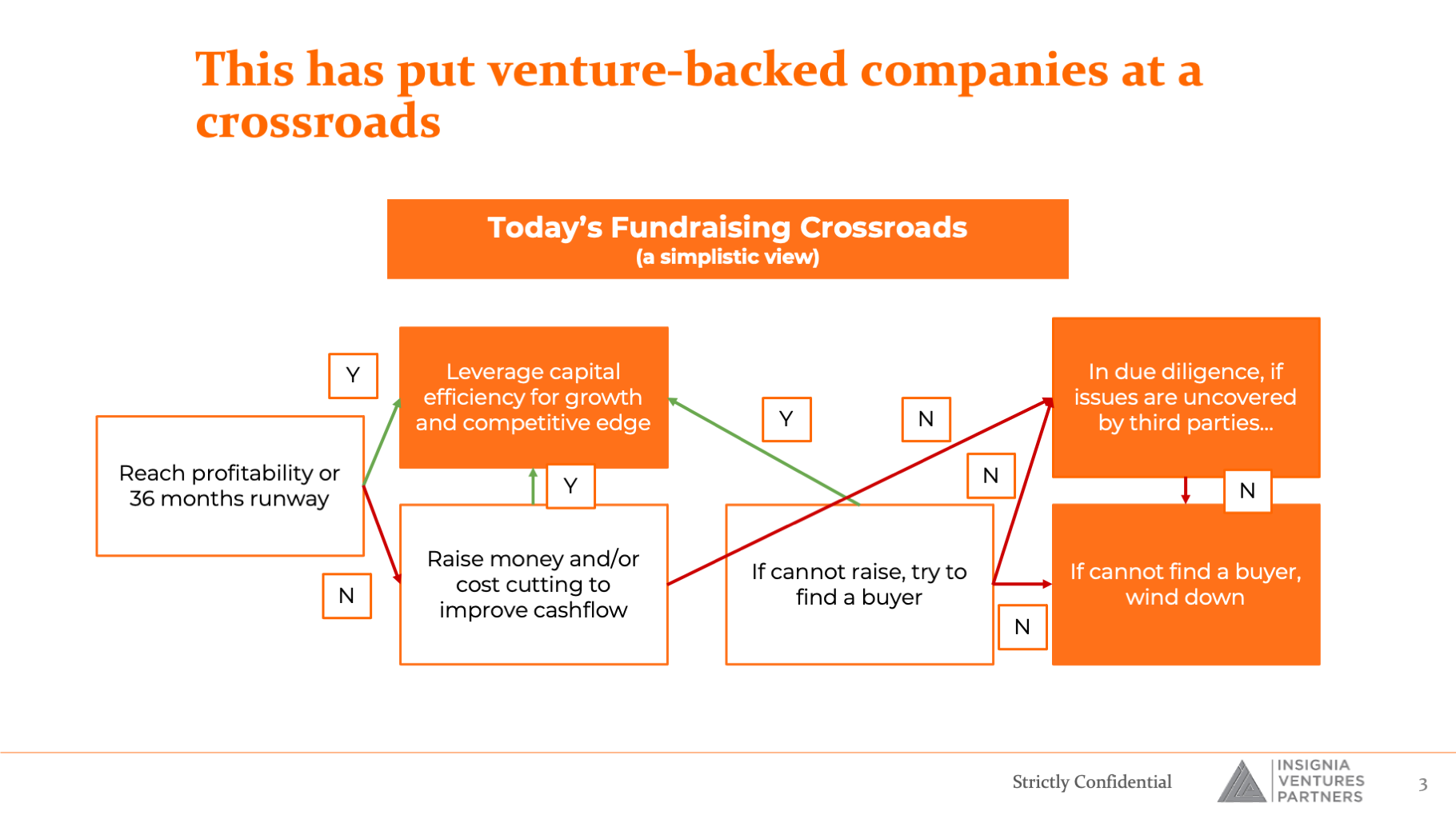

This trend has placed venture-backed companies at a critical juncture in fundraising (Exhibit 2). Companies unable to extend or raise their runway towards 36 months or more or reach profitability are forced to take severe measures to stay afloat. And in the midst of all this fundraising demand are more stringent expectations from investors that have led to due diligence red flags being raised after years of being unchecked.

Exhibit 1. Market correction in public companies has led to fundraising challenges in the near term. Taken from Pitchbook and our private market statistics tool.

Exhibit 2. This has put venture-backed companies at a crossroads. Taken from an article on cash flow management from earlier this year.

Inspite of (and to some extent, because of) the market correction and macroeconomic headwinds, the ASEAN opportunity remains compelling for investors globally.

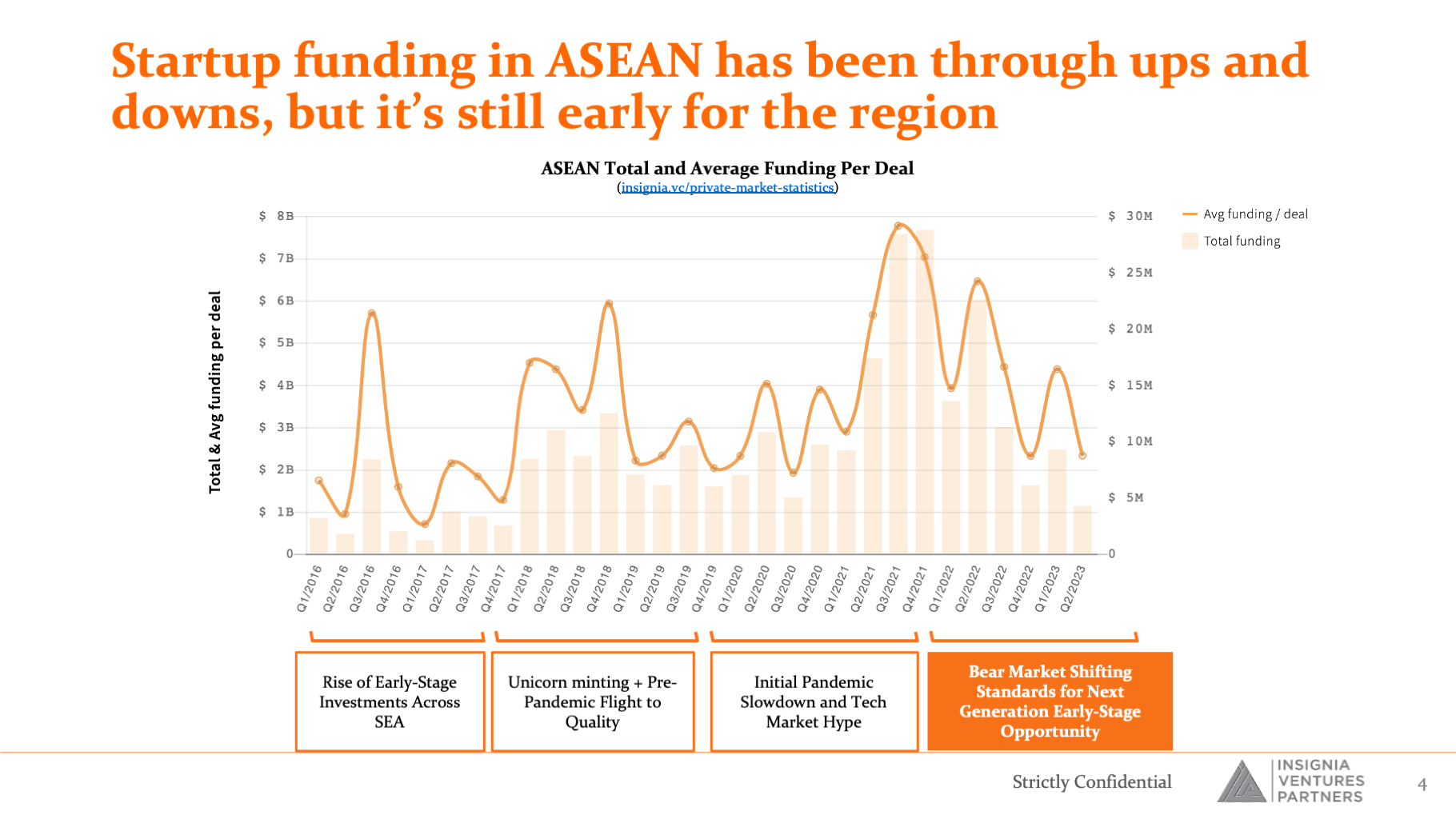

Startup funding in the ASEAN region has seen its ups and downs (Exhibit 3), but the region has only just experienced its first “bear market” cycle in these past few months. Global investors, in some cases precisely to diversify risk, continue to see Southeast Asia as a relatively greener spot in the world for capital allocation.

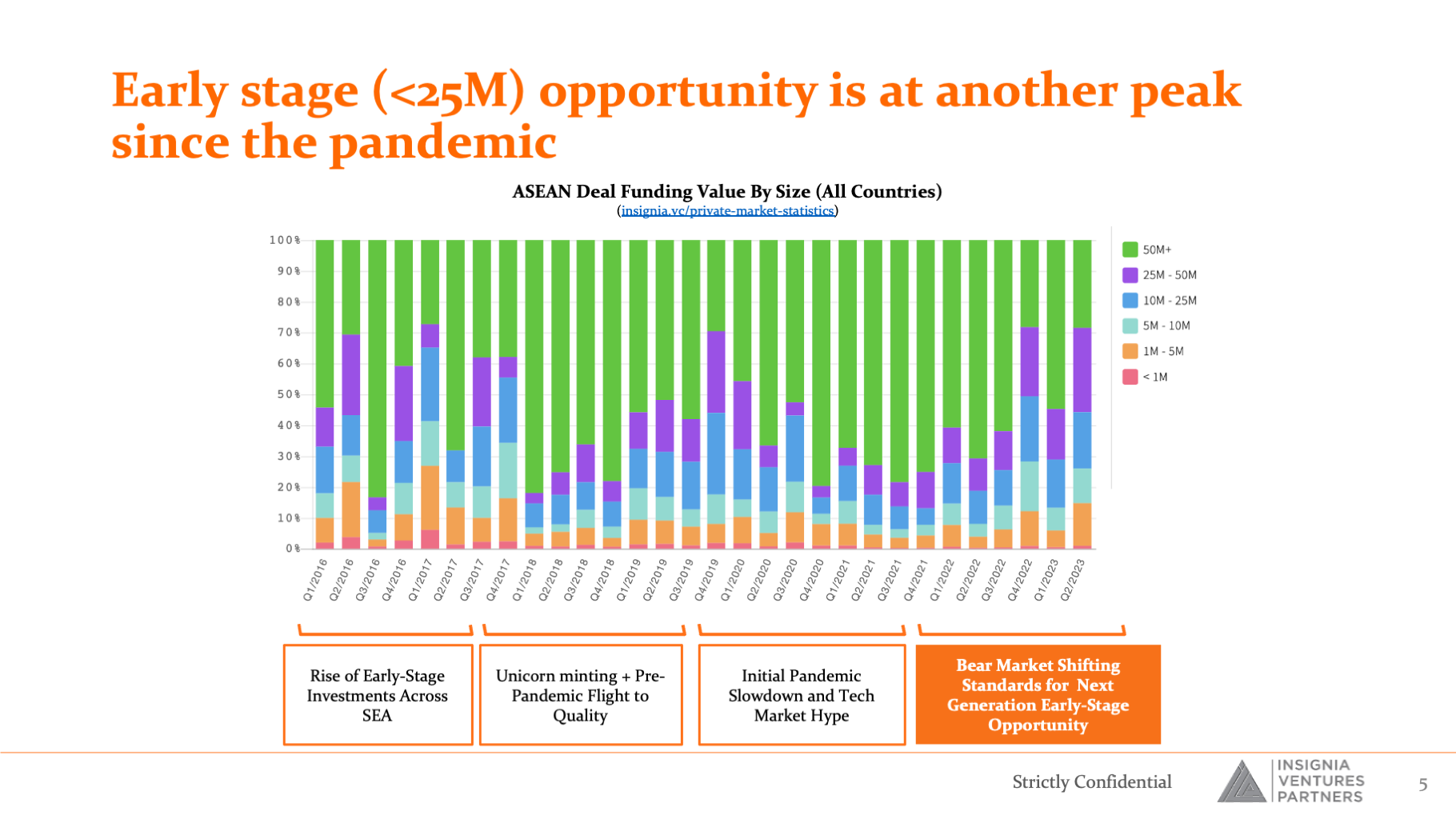

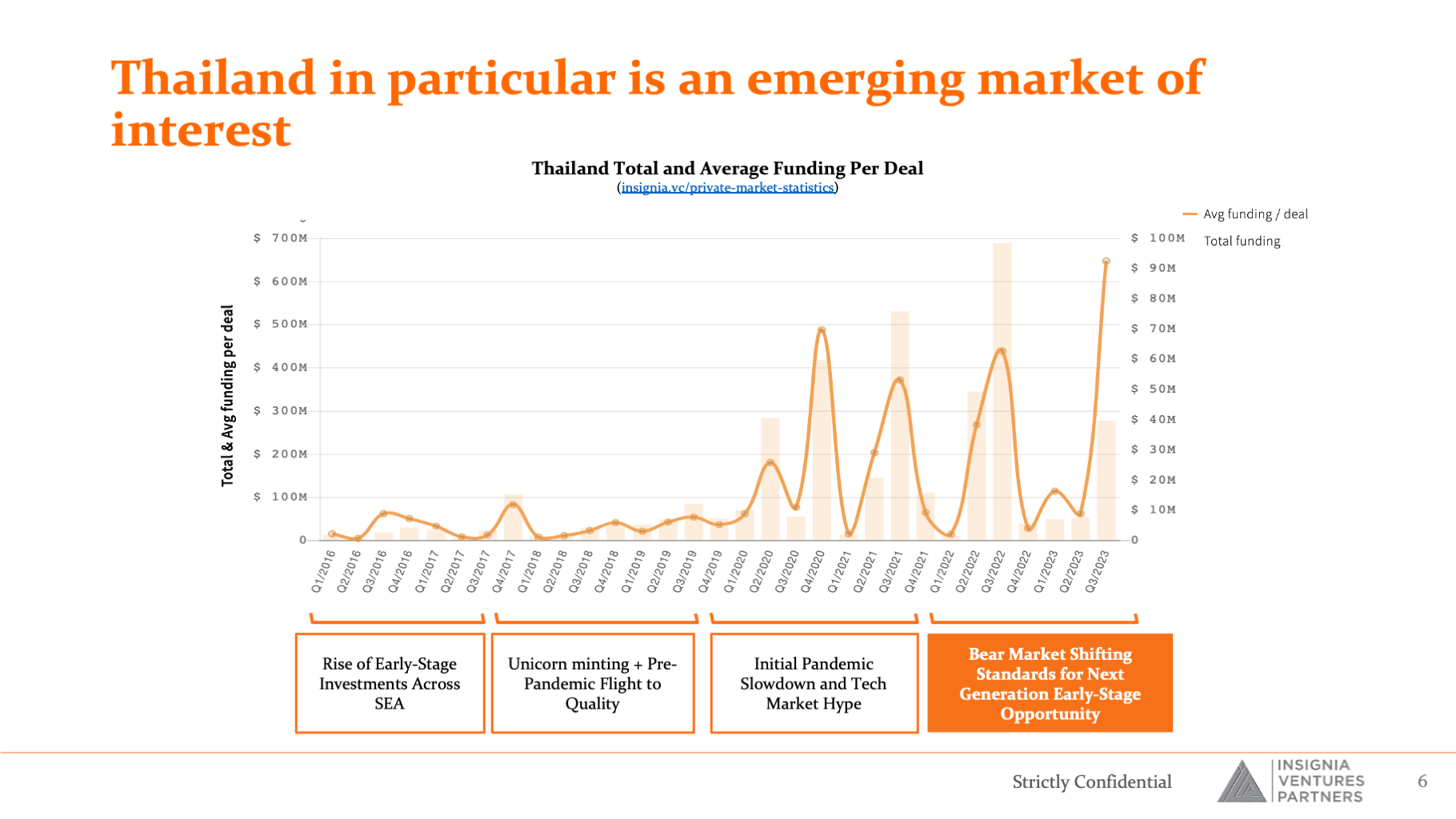

Early-stage (<$25M) opportunities are peaking again since the pandemic (Exhibit 4), with Thailand emerging as a particularly interesting market (Exhibit 5). We previously wrote about how Thailand exceeded Indonesia in share of fundraising earlier tis year.

Exhibit 3. Startup funding in ASEAN has been through ups and downs, but it’s still early for the region. Taken from our private market statistics tool.

Exhibit 4. Early stage (<25M) opportunity is at another peak since the pandemic. Taken from our private market statistics tool.

Exhibit 5. Thailand in particular is an emerging market of interest. Taken from our private market statistics tool.

Moreover, the fundamentals continue to drive the ASEAN digital economy forward, even amidst a bear market.

The region’s population as of H1 2023 is inching close to 700 million. Internet penetration in ASEAN sans Laos, Myanmar, and Timor-Leste has cross 75% with 400 million internet users. The region’s combined regional GDP in 2022 reached 3.66 trillion USD. And importantly, dry powder has accumulated significantly in the APAC region, with 676B USD as of Q1 2023, up 20% from last year. The trifecta of a digital economy — growing population, infrastructure penetration, and GDP/capita — combined with dry powder to fuel supply meeting demand, remains a compelling story for Southeast Asia.

5 Implications of Challenges and Opportunities for Building Resilient Companies in Southeast Asia

The region faces several challenges and opportunities, including:

- Valuation Adjustments: Resulting in a tighter fundraising market.

- Investor Expectations: Raising the bar as investors hold significant uninvested capital.

- Technological Advances: The rise of Generative AI has brought AI, ML, data science, and automation back into the spotlight.

- Diversification of Resources: This includes supply chains, capital allocation, and talent into SEA.

- Continued Opportunities: There is ongoing emerging market potential in Southeast Asia amidst economic headwinds.

These factors suggest that fundraising now favors companies that are financially robust and capital efficient. Finance leaders who enhance governance capabilities are increasingly sought after, and there is an era of monetization innovation underway to unlock new markets and create sustainable businesses. We dive into these five implications below:

(1) Fundraising Today Favors the Financially Robust and Capital Efficient

Before: Startups could raise funds with just a pitch deck, growth was the primary goal, 12-18 month runways were sufficient, and there was less pressure to live up to valuation premiums.

Today: A pitch deck is not enough. Growth must come with positive unit economics, and traction must align with product-market-pricing fit. Longer fundraising cycles are needed, and companies must be either profitable or have significant runway (>36 months). Valuation premiums are penalized unless justified by sustainable growth, and without audited financial statements, funding is unlikely.

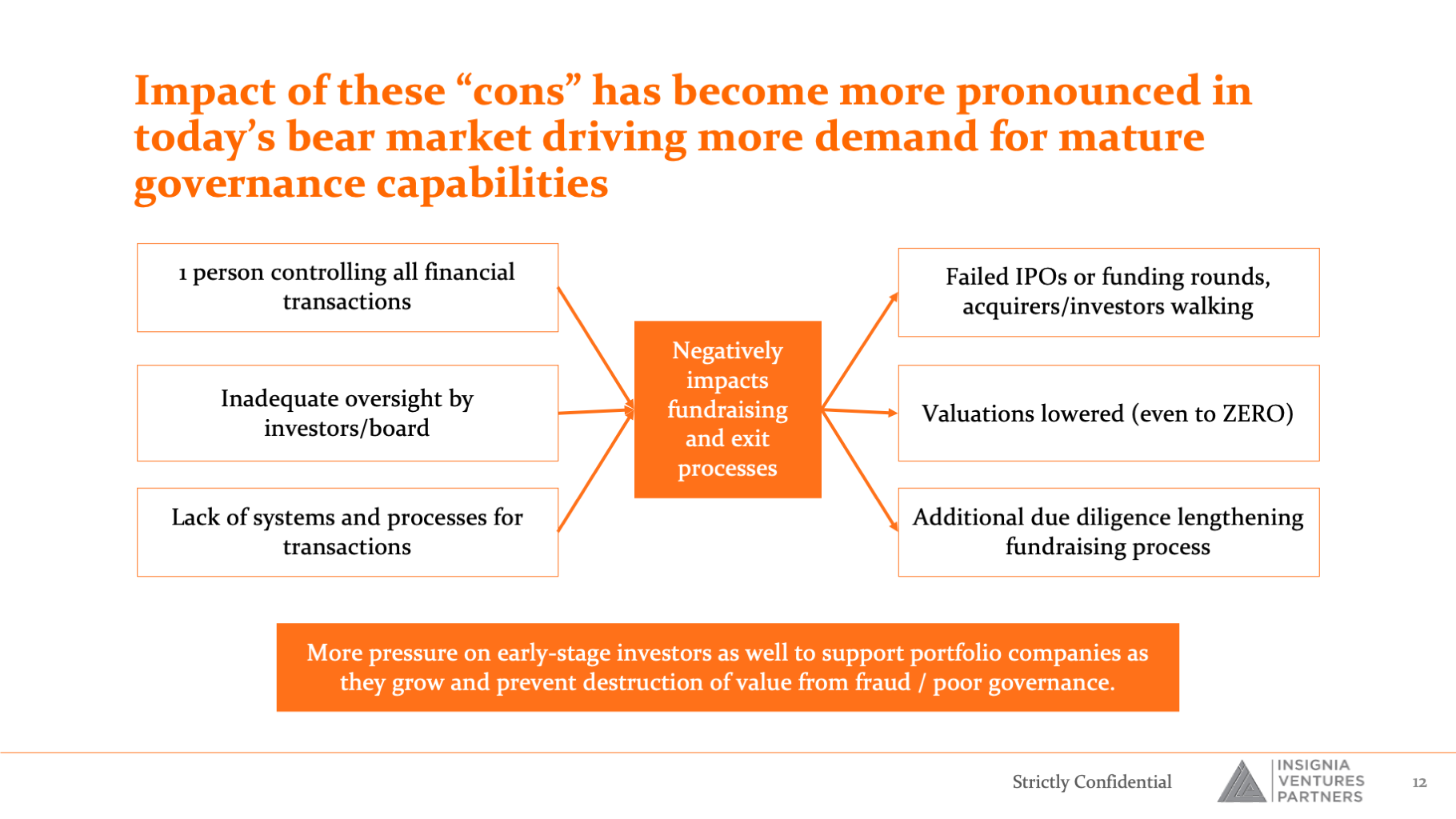

(2) Financial Professionals are in Demand, Especially Those Who Can Strengthen a Company’s Governance Capabilities

Investors are cautious, and companies lacking audited financials from recognized audit firms are unlikely to get funding. The 31 funds that raised $4.14B in SEA in 2022 demonstrate the strength of available capital from venture capital alone. This reality has increased demand for financial leaders skilled in audit requirements and financial controls, a move to ensure better governance and compliance, especially as companies grow and scale.

For the longest time, startups have differentiate themselves from corporates in terms of finance functions more suited towards speed and raising capital, oftentimes foregoing maturity of compliance and monitoring. While this has provided room for startups to navigate early stage spending limitations and uncertainty, while being primed for agility and adaptability and a focus on growth and strategy, it comes with cons as well.

Understaffed, inexperienced finance functions have made the transition to growth challenging, especially in a market where it is more difficult to raise as a growth company. The lack of focus on compliance and governance capabilities have made businesses prone to scaling risks. This has negatively impacted the fundraising and exit processes of companies in today’s market (Exhibit 6).

Exhibit 6. Impact of these “cons” has become more pronounced in today’s bear market driving more demand for mature governance capabilities

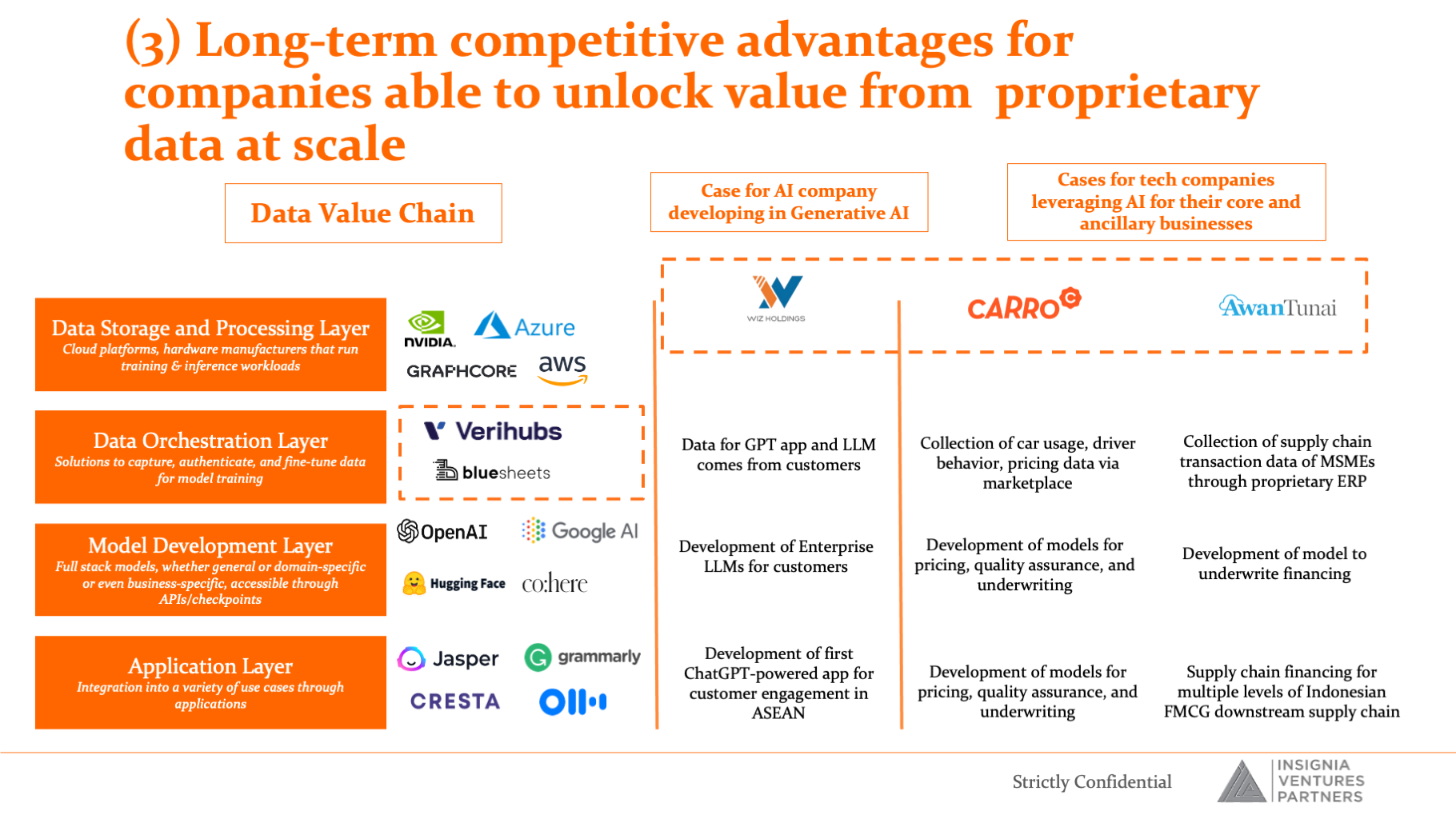

(3) Long-term Competitive Advantages for Companies Able to Unlock Value from Proprietary Data at Scale

The demand for fine-tuned, secure, and reliable AI is driving the development of the data value chain (i.e., the industry of storing, processing, training, and developing models and apps on top of data sets). This not only enables better tech applications for Gen AI use cases (i.e., the next generation of AI/ML models) as in the case of WIZ.AI with their voice AI solutions, but also empowers companies beyond Gen AI (Exhibit 7) like Carro or AwanTunai tapping into their proprietary data sets. Southeast Asia’s Gen AI journey is still unfolding, but the foundation is present and awaiting activation (Exhibit 8).

Read more about our views and learnings from exploring the AI spaces with our AI Notes series.

Exhibit 7. Long-term competitive advantages for companies able to unlock value from proprietary data at scale. Taken from our AI Notes #2.

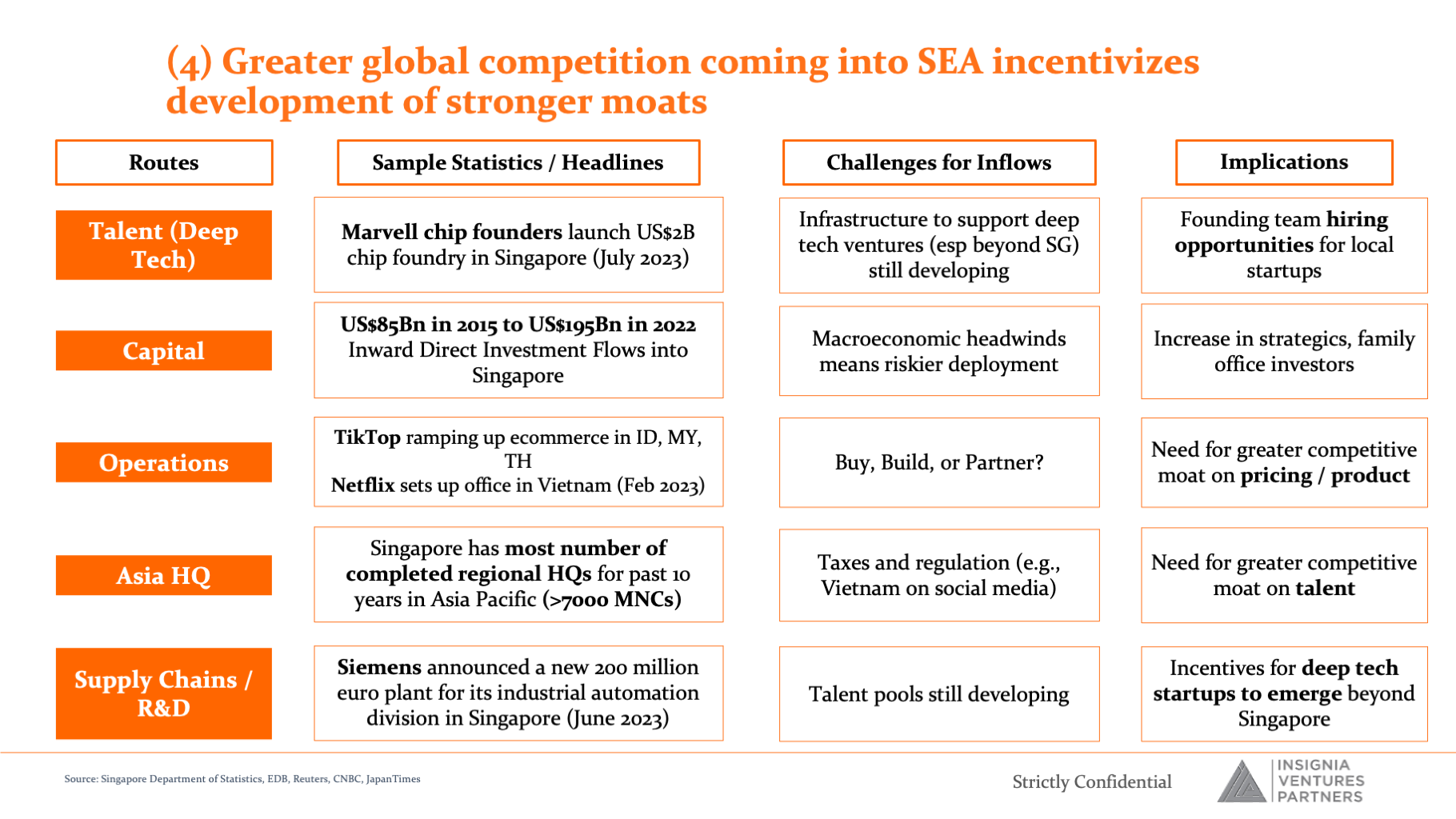

(4) Greater Global Competition in SEA Incentivizes Development of Stronger Moats

In Southeast Asia, there is a shift in global talent and capital flows from opportunistic moves to infrastructure set up and competitive expansion. Opportunistic / strategic talent and capital flows include entrepreneurs setting up new ventures in SEA, HNWIs setting up family offices in Singapore, and specific strategic / growth investments by global companies (Alibaba, Tencent, Meta, Google).

Now competitive / infrastructure talent and capital flows have seen more global companies setting up HQs in Singapore, R&D centres in Vietnam, more global funds setting up offices in Singapore, expanding presence across SEA (TikTok, Shein, Netflix, etc.)

The implications for startups are the following (Exhibit 8):

Exhibit 8. Greater global competition coming into SEA incentivizes development of stronger moats. Taken from a previous article on the topic.

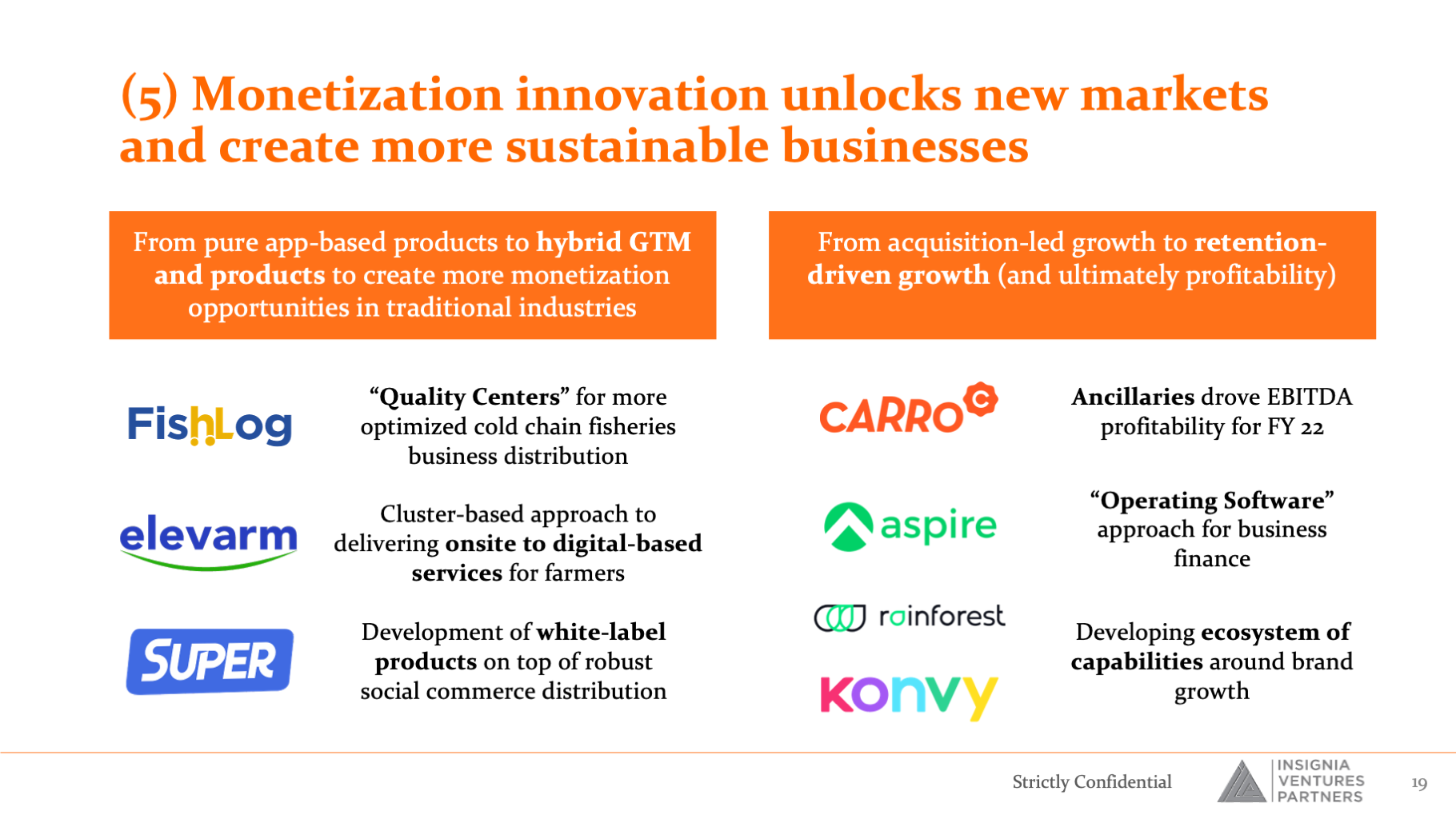

(5) Monetization Innovation Unlocks New Markets and Creates More Sustainable Businesses

As the region has built up various ways of acquiring users into the digital economy over the past decade, the biggest question is now how to monetize and ensuring sustainable retention. Combined with venture funding expectations (see Implication #1), the market is ripe more than ever before for more monetization innovation. Two significant shifts in product distribution are leading to more effective monetization:

(1) Hybrid Distribution Models: Transitioning from pure app-based products to combinations of go-to-market strategies.

This unlocks more adjacencies and stronger retention to build on these adjacencies down the line.

For example, upstream smallholder farmger agritech Elevarm has a cluster-based approach to delivering onsite to digital-based services for farmers, or social commerce for rural Indonesia Super has invested in the development of white-label products on top of robust social commerce distribution.

(2) Retention-Driven Growth: Moving from acquisition-led growth to a focus on retention and profitability.

For example, AI-driven auto retail group Carro leverage ancillaries to drive EBITDA profitability for FY 23 (all the way through Q1 for FY 2024 with its best quarter yet), OS for business finance Aspire with its “Operating Software” approach for business finance that recently saw profitability, and beauty brand platform Konvy, and ecommerce house of brands for moms and kids Rainforest: developing an ecosystem of capabilities around brand growth.

These changes represent a maturing and dynamic landscape in Southeast Asia, with implications for startups, investors, and markets alike. The themes of resilience, innovation, and adaptability stand out, promising an exciting future for the region.

Exhibit 9. Monetization innovation unlocks new markets and create more sustainable businesses

In the ever-changing landscape of the global economy, Southeast Asia (SEA) presents a unique blend of challenges and opportunities for startups and venture capital (VC) firms. This article dives into the current market trends, outlining how public company valuations are influencing the startup scene, the changing dynamics of fundraising, and the strategic innovations shaping the future. As SEA becomes an increasingly attractive hub for entrepreneurship and investment, understanding these dynamics is crucial for building resilient companies.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.