In recent years, Southeast Asia has become a vibrant hotspot for startups and innovation. Despite facing global headwinds such as economic uncertainties and the COVID-19 pandemic, the region’s startup ecosystem has shown remarkable resilience.

The funding landscape has not only weathered these challenges but also matured, entering a new cycle that appears promising for early-stage companies.

In this article, we delve into how this funding momentum is shaping startup innovation, competitive advantages, and growth opportunities in Southeast Asia, using insights from our private market statistics tool.

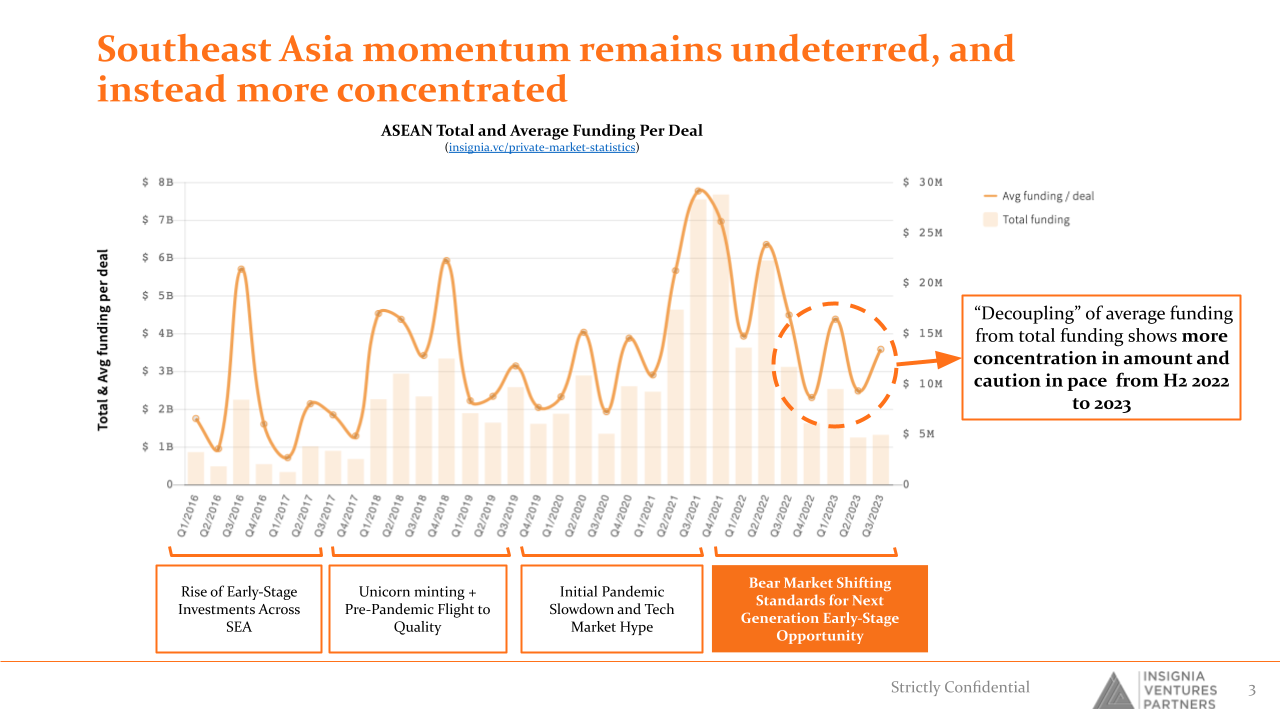

Southeast Asia Funding Momentum for Startups Remains Undeterred and More Concentrated

Contrary to initial apprehensions, the funding environment in Southeast Asia from H2 2022 to 2023 has shown a notable “decoupling” of average funding from total funding.

This suggests that investors are becoming more concentrated in their bets, putting larger amounts into fewer startups.

This increased focus is in line with a cautious optimism, reflecting an investment strategy that aims for quality over quantity.

Southeast Asia momentum remains undeterred, and instead more concentrated in fewer startups

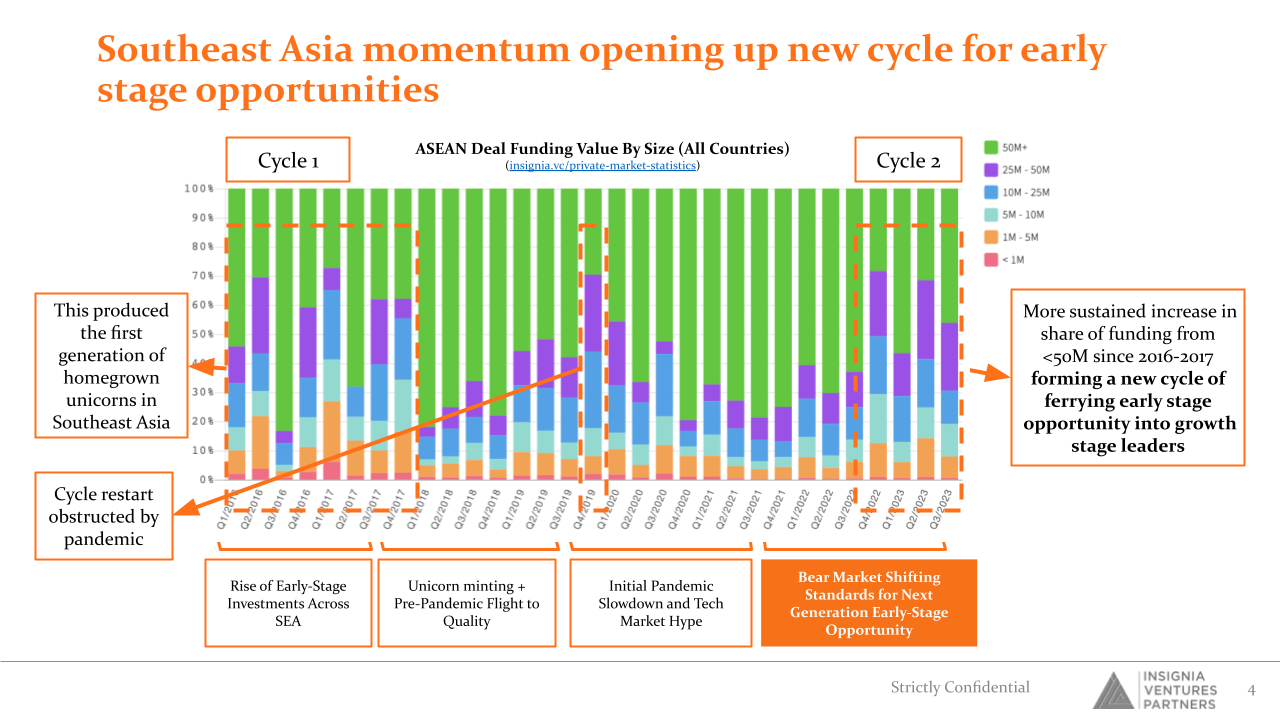

A New Cycle of Opportunities for Early-Stage Startups

The first wave of significant startup activity in Southeast Asia occurred between 2016 and 2017, giving birth to the region’s first generation of homegrown unicorns. A second wave seemed on the way for 2020 but was derailed by the pandemic.

However, the years 2022 and 2023 have seen a sustained increase in the share of funding for companies valued at less than $50 million. This trend is indicative of a new cycle, targeting early-stage startups with the potential to become growth-stage leaders.

Southeast Asia momentum opening up new cycle for early stage opportunities for startups

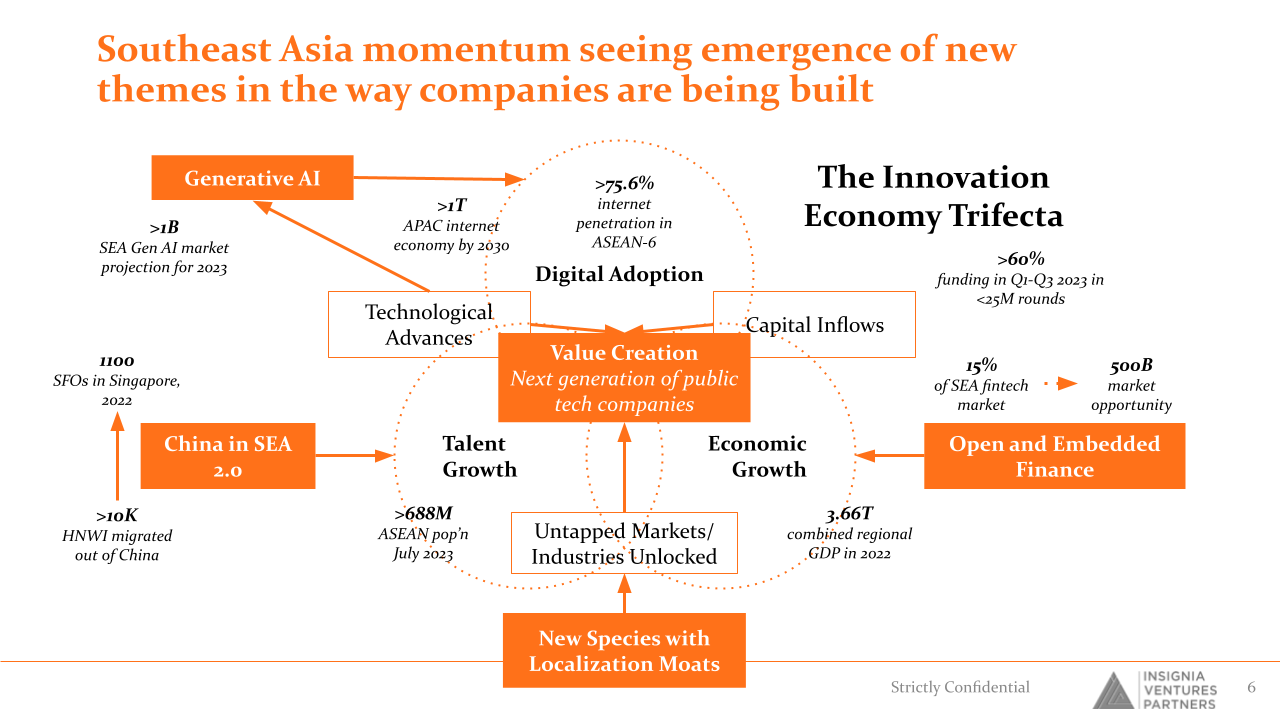

New Themes in Formation of Startups

We can look at the emerging areas of interest or trends coming out this early-stage interest in the region through the lens of what we call “the innovation economy trifecta”: digital adoption/penetration, tech + entrepreneurial talent growth, and economic growth (GDP/capita).

AI 2.0 technology

When it comes to digital adoption, we see this being radically transformed by generative AI, impacting the way consumers access products and services. For example, you can have insurance policies being designed for specific customers based on their lifestyle and behavior (we already see companies like Carro doing this to an extent with AI-driven usage-based insurance). Or you can have wealth management platforms being supported by autonomous AI agents acting in the place of advisors. Of course, this also extends to enterprise as well, with companies like WIZ.AI introducing the ability to build customized LLMs for specific businesses or operational use cases.

More in our AI Notes Series

China in SEA 2.0 founders

When it comes to tech and entrepreneurial talent growth, in Singapore in particular we see a new wave of Chinese entrepreneurs who are not just expanding their businesses into Singapore but actually making the country their HQ or base of operations. They are still leveraging their ties to Chinese capital and engineering, but ultimately the goal is to build a global company from Singapore.

This “China in SEA 2.0” will be important in maturing the competitive landscape in Southeast Asia, and also contribute especially to deep tech, which is a strong focus for investment in Singapore. This influx is also supported by a “capital exodus” from China into emerging markets, with more than 10K HNWI’s moving out of China over the past year (more than 13K expected in 2023), and SFOs in Singapore climbing up from 700 in 2021 to 1100 in 2022, with significant contribution from the Chinese market.

More in this podcast with Reuters correspondent Fanny Potkin

Fintech 2.0 startups

Then when it comes to economic growth, we see increasing activity and interest in open and embedded finance. Fintech is worth US$250B in Southeast Asia alone, and 15% of that is in embedded finance. Given just how many use cases there are in terms of being incorporated into B2B commerce (e.g., supply chain financing) and consumer journeys, this sector has the potential to grow into a half a trillion dollar opportunity over the next few years.

More in this “Fintech is Everywhere” article

Southeast Asia momentum seeing emergence of new themes in the way startups are being built

A CNBC interview with our founding managing partner Yinglan Tan also covers these themes.

The current funding momentum in Southeast Asia is much more than just an influx of capital; it signifies the maturing of an ecosystem. Investors are becoming increasingly discerning, and startups are benefiting from an environment that is more focused, more global, and more technologically advanced than ever before.

Given the talent and capital influx into Singapore, VC funding in Singapore and SEA can be seen moving further in three trajectories: more early-stage, more deep tech or deep tech adjacent, and more diversified in terms of industries.

More early-stage interest is a response to capitalize on the opportunity to grow next generation unicorns and market leaders. More deep tech interest is a response to an influx of mature, senior tech talent into the region. More diversified interest is a response to saturation in certain industries and markets and more entrepreneurs emerging out of industries that were not given as much attention before.

For early-stage companies, this is the time to innovate and set the stage for becoming the growth-stage leaders of tomorrow.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.