Southeast Asia’s fintech market will explode from $38 billion today to $180 billion by 2030—but that’s just the beginning. The region’s embedded finance champions are positioned to capture massive shares of the $320 billion global opportunity, armed with battle-tested models, 438 million underbanked customers as proof points, and AI-powered platforms built for emerging markets worldwide.

This isn’t just another growth story. It’s the emergence of embedded finance as the dominant model for financial services delivery across Southeast Asia, where mobile-first, platform-centric ecosystems have leapfrogged traditional banking infrastructure. The convergence of embedded finance with AI-powered credit assessment and global expansion strategies represents the most significant opportunity in Southeast Asian fintech since the mobile revolution began.

The Embedded Finance Revolution: Beyond Payments to Platform Economics

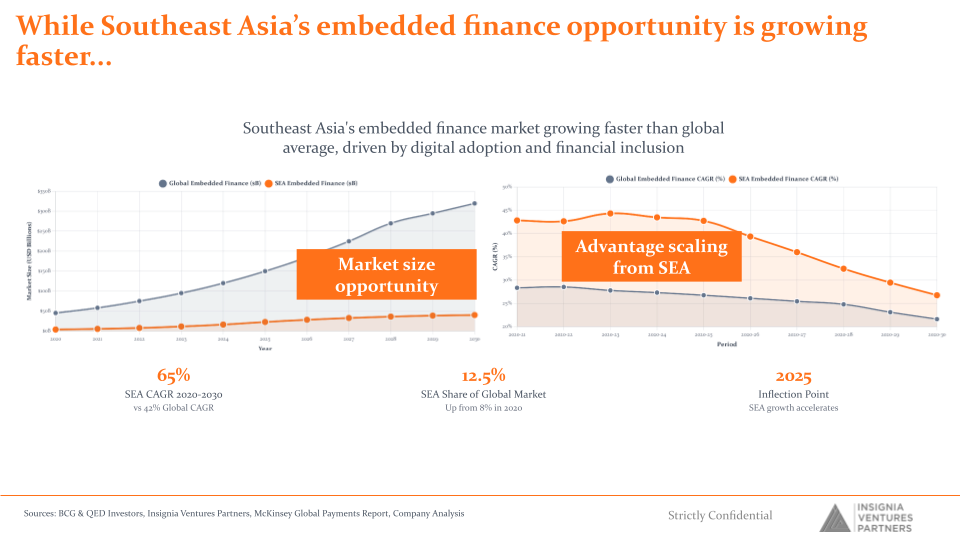

The future of fintech in Southeast Asia is embedded, and the numbers tell a compelling story. By 2030, embedded finance will account for 40% of the total digital finance market—a staggering $72 billion opportunity growing at 57.7% CAGR from its current 25% share of $9.5 billion in 2024. This isn’t merely an evolution; it’s a complete restructuring of how financial services integrate into daily life and business operations.

What makes Southeast Asia uniquely positioned for this embedded finance revolution is the region’s mobile-first, platform-centric ecosystem. Unlike mature markets burdened by legacy banking infrastructure, Southeast Asian markets have leapfrogged directly to digital-native solutions. Super apps like Grab and Gojek don’t just dominate transportation and food delivery—they’ve become comprehensive financial ecosystems where embedded finance is the primary model, not an add-on feature.

Consider Grab’s evolution from a ride-hailing app to a financial services powerhouse. Launched in 2016, GrabPay now serves 44.5 million monthly transacting users across eight Southeast Asian countries, processing $4.9 billion in on-demand gross merchandise value in Q1 2025 alone. But the real innovation lies in how Grab has embedded financial services throughout its ecosystem: GrabFin Credit provides AI-powered lending with $1.43 billion in customer deposits, GrabInsure offers micro-insurance products embedded directly into rides and deliveries, and GrabInvest rounds out the wealth management offering launched in 2023.

This embedded approach extends beyond super apps into vertical-specific solutions that address deep-rooted market inefficiencies. Take AwanTunai, which has revolutionized Indonesia’s $100 billion FMCG supply chain by embedding financing directly into inventory management systems. Since its founding in 2017, AwanTunai has maintained laser focus on supply chain financing for micro, small, and medium enterprises (MSMEs), achieving remarkable scale with 61 million monthly loan disbursements worth 1 trillion Indonesian Rupiah as of April 2025.

What sets AwanTunai apart is its recognition that embedded finance isn’t just about payments—it’s about embedding financial services into the operational fabric of businesses. By combining inventory purchase financing with proprietary enterprise resource planning (ERP) technology, AwanTunai captures valuable transaction data that enables accurate credit assessment even when traditional financial indicators are unreliable. This approach proved its resilience during the COVID-19 pandemic, when AwanTunai maintained a remarkable 3% non-performing loan rate while the industry average soared to 20-30%.

The embedded finance opportunity in Southeast Asia is further amplified by the region’s demographic dividend. With over 60 million MSMEs in Indonesia alone—representing 90% of the workforce—and a $165 billion MSME financing gap, the potential for embedded financial solutions to drive economic inclusion is unprecedented. These businesses don’t need another banking app; they need financial services seamlessly integrated into their existing workflows, supply chains, and customer interactions.

AI-Powered Credit: The Engine of Global Embedded Finance Expansion

The transformation of embedded finance from a regional phenomenon to a global force is being powered by artificial intelligence’s ability to democratize credit assessment and enable financial inclusion at unprecedented scale. This is where companies like Surfin demonstrate how AI-powered alternative credit scoring becomes the foundation for embedded finance platforms that can scale across diverse emerging markets.

Dr. Yanan Wu’s journey from nuclear physicist to fintech founder exemplifies this AI-driven transformation. Standing on a bridge in Jakarta in 2017, witnessing the stark wealth divide between luxury shopping districts and nearby slums, Wu recognized that traditional credit assessment methods would never bridge this gap. The solution lay in leveraging AI to create comprehensive credit profiles using alternative data sources—smartphone usage patterns, social media behavior, e-commerce activity, and digital footprints that traditional banks ignore.

Surfin’s proprietary credit scoring engine represents the future of embedded finance: a 360-degree profiling system that enables financial services to be embedded into any digital touchpoint where underserved consumers interact. This approach has scaled to serve 60 million users across nine markets globally, demonstrating how AI-powered credit assessment can transcend geographic and regulatory boundaries to create truly global embedded finance platforms.

The power of this model lies not in deploying identical algorithms globally, but in the universality of the AI-powered approach to alternative credit assessment. While the framework remains consistent—using alternative data sources to build comprehensive credit profiles—successful global expansion requires sophisticated localization strategies. The same AI methodology that assesses creditworthiness for a motorcycle taxi driver in Jakarta must be fundamentally adapted and retrained to evaluate a street vendor in São Paulo or a small retailer in Lagos, incorporating local data sources, regulatory requirements, cultural behaviors, and economic patterns specific to each market.

This localization challenge is where Surfin’s global success becomes particularly instructive. The company’s expansion across nine markets required developing market-specific algorithms that account for different smartphone usage patterns, social media behaviors, e-commerce platforms, and payment systems in each region. What remains universal is the AI framework for processing alternative data—but the data sources, weighting mechanisms, risk models, and decision trees must be carefully calibrated for local contexts.

As Wu notes on our podcast, “In fintech, we must embrace cycles. We must make decisions that ensure the business doesn’t overstretch itself. We can’t be blindly focused on growth—we must remain sensitive to the risks.” This philosophy of responsible expansion recognizes that each new market requires substantial investment in understanding local nuances, building partnerships with local data providers, and adapting algorithms to local regulatory and cultural environments. The AI advantage lies not in plug-and-play deployment, but in having a proven methodology for rapidly developing and iterating market-specific credit assessment models.

Surfin’s recent $26.5 million Series A funding round, led by Woori Venture Partners, validates the global potential of AI-powered embedded finance platforms. The company’s ability to cross-sell different financial products—from consumer financing to payments, wealth management, and credit cards—demonstrates how AI-powered credit assessment becomes the foundation for comprehensive embedded finance ecosystems that can compete globally.

The AI advantage extends beyond individual companies to the broader Southeast Asian embedded finance ecosystem. According to Insignia Ventures Partners’ analysis, Southeast Asian fintechs facilitate over $320 billion in transaction value and generate over $6 billion in revenue, with embedded finance representing a growing share of this activity. The region’s digital-first infrastructure creates natural advantages for AI integration, as these platforms can deploy machine learning algorithms across their entire technology stack without the constraints of legacy system integration.

Generative AI: The Operational Multiplier for Embedded Finance Platforms

Generative AI is transforming embedded finance platforms by creating operational efficiencies that traditional financial institutions cannot match. Carro exemplifies this transformation, using AI to revolutionize automotive financing through its Genie Finance arm.

At Carro, AI powers the entire financing journey—from initial application to underwriting and ongoing customer management. The company’s proprietary AI models analyze vast datasets collected from vehicle transactions, driving patterns, and maintenance records to make credit decisions that traditional banks simply cannot match in speed or accuracy. This capability is particularly valuable in Southeast Asia’s fragmented automotive market, where conventional credit scoring often fails to capture the true creditworthiness of potential borrowers.

“At Carro, we want to provide the best experience for customers applying for financing,” explains Zi Yong Chua, Carro’s COO, on our podcast. “The process involves assessing a customer’s credit profile, which traditionally required extensive manual review of documents and financial records. Our Gen AI implementation has transformed this process, reducing loan application processing time from days to minutes while simultaneously improving risk assessment accuracy.”

The impact of this AI-powered approach extends beyond just speed. Carro’s models enable dynamic, personalized financing offers based on specific vehicle characteristics and customer profiles. For example, the system can instantly adjust loan terms based on a vehicle’s projected depreciation curve, maintenance history, and the applicant’s driving behavior—factors that would be impossible to incorporate in real-time without advanced AI capabilities.

This level of sophistication has allowed Carro to pioneer innovative financing products like distance-based and behavioral-based insurance premiums, where rates are determined by actual usage patterns rather than static demographic factors. The company’s AI systems continuously monitor vehicle performance data, enabling proactive maintenance alerts that reduce default risks by preventing major mechanical failures before they occur.

The business impact has been substantial. Genie Finance has become one of Carro’s most profitable business units, with AI-powered efficiencies driving both top-line growth and bottom-line results. The company reports a 40% reduction in operational costs for loan processing while maintaining loan performance metrics that outperform industry averages. Most importantly, this AI-driven approach has enabled Carro to serve customer segments that traditional auto financing would consider too risky, expanding financial inclusion in the automotive sector.

Carro’s success demonstrates how embedded finance platforms can leverage Gen AI to create virtuous cycles of data acquisition and service improvement. Each transaction generates new data points that further refine the AI models, creating an expanding competitive advantage that becomes increasingly difficult for traditional financial institutions to overcome.

Beyond the $180 Billion: Southeast Asia as a Launchpad for Global Embedded Finance Dominance

While the $180 billion Southeast Asian opportunity by 2030 represents a massive market in its own right, it’s crucial to understand that this figure represents just the beginning of the global expansion potential for the region’s embedded finance champions. The convergence of embedded finance with AI-powered credit assessment and operational efficiency creates unprecedented opportunities for Southeast Asian fintech companies to build global platforms that extend far beyond their home markets—and the numbers reveal just how significant this global opportunity truly is.

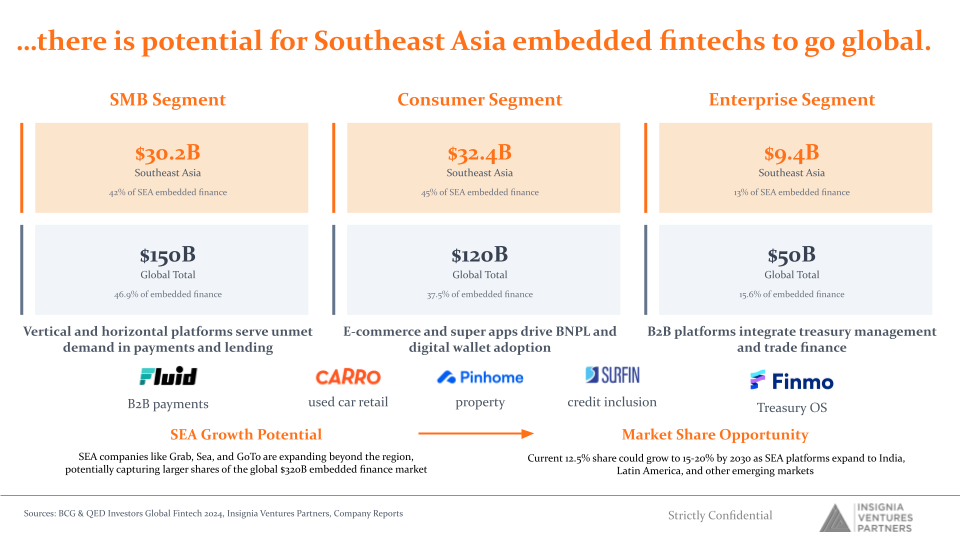

The embedded finance market globally dwarfs even Southeast Asia’s impressive projections. Across three key segments, the global opportunity represents a market that is 4-5 times larger than Southeast Asia’s domestic market, creating a compelling case for regional expansion by companies that have proven their models locally.

In the SMB segment, Southeast Asia’s $30.2 billion opportunity (representing 42% of the regional embedded finance market) sits within a global market worth $150 billion—meaning that Southeast Asian companies have access to a market nearly five times larger than their home region. This segment is particularly promising because vertical and horizontal platforms that serve unmet demand in payments and lending face similar challenges across emerging markets worldwide.

AwanTunai exemplifies the power of embedded finance in the SMB segment, having mastered FMCG supply chain financing in Indonesia’s complex market. While the company remains focused exclusively on the Indonesian market with no current plans for international expansion, their success has attracted global investors who recognize the model’s effectiveness. AwanTunai’s approach to combining inventory purchase financing with proprietary enterprise resource planning (ERP) technology creates a powerful data advantage that enables accurate credit assessment even in challenging markets. This data-driven approach to embedded finance has proven remarkably resilient, maintaining a 3% non-performing loan rate during the COVID-19 pandemic while the industry average soared to 20-30%.

The consumer segment presents an even more compelling global expansion story. Southeast Asia’s $32.4 billion consumer embedded finance market (45% of regional embedded finance) represents just over one-quarter of the $120 billion global opportunity. This segment is driven by e-commerce and super app adoption of buy-now-pay-later and digital wallet solutions that have proven global applicability. Portfolio companies like Carro, which has revolutionized used car retail financing, and Pinhome, which has embedded financing into property transactions, demonstrate models that can scale across any market where consumers need flexible financing options for major purchases.

Pinhome’s approach exemplifies the power of embedded finance in creating seamless customer experiences. As CEO Dayu Dara Permata explains on the podcast, “Mortgage entry points that are attached to the brokerage home-search journey are right there in the listing. As they are scrolling through the listings, they can see their mortgage availability, which banks are available for this particular listing, and what’s going to be the monthly installment for them.” This integration of financing directly into the property search experience has enabled customers who were previously rejected by traditional banks to secure mortgages through Pinhome’s AI-powered matching system.

Perhaps most intriguingly, the enterprise segment—while representing the smallest portion of Southeast Asia’s embedded finance market at $9.4 billion—sits within a $50 billion global market, offering more than five times the expansion potential. This segment focuses on B2B platforms that integrate treasury management and trade finance, exemplified by companies like Fluid (B2B BNPL) and Finmo (Treasury OS). These enterprise-focused solutions address universal business needs that transcend geographic boundaries, making them particularly well-suited for global expansion.

Fluid’s rapid growth demonstrates the global potential of B2B embedded finance. The Singapore-based platform has achieved 10x growth over the past 12 months, serving over 3,000 businesses across Singapore and Malaysia with tens of millions in disbursements. According to Insignia Ventures Partners’ analysis, 80% of Singapore’s SMEs have expressed interest in installment payment options for small businesses, indicating strong market demand that exists across emerging markets globally. Fluid’s AI-powered approach to B2B payments and financing addresses the $21.9 billion Southeast Asian B2B financing market while building capabilities that can scale to serve similar needs in other regions.

The global expansion thesis is further strengthened by Southeast Asia’s unique position as a testing ground for embedded finance innovation. As noted in the market analysis, SEA companies like Grab, Sea, and GoTo are already expanding beyond the region, potentially capturing larger shares of the global $320 billion embedded finance market. The current 12.5% share that Southeast Asian platforms hold could realistically grow to 15-30% by 2030 as these platforms expand to India, Latin America, and other emerging markets.

This expansion potential is not theoretical—it’s already happening. The market share opportunity analysis shows that Southeast Asian platforms are well-positioned to capture significant portions of global embedded finance growth, particularly in markets with similar demographic profiles, mobile-first adoption patterns, and financial inclusion challenges. The combination of proven business models, battle-tested technology platforms, and deep understanding of emerging market dynamics positions Southeast Asian fintechs as natural leaders in the global embedded finance revolution.

What makes this convergence particularly powerful is how embedded finance creates distribution channels and customer touchpoints that enable financial services to reach previously underserved populations at scale. AI-powered credit assessment provides the risk management capabilities needed to serve these markets profitably. Generative AI enhances both embedded finance and credit assessment by improving operational efficiency, automating compliance, and personalizing customer experiences across diverse markets and regulatory environments.

The result is a new category of financial services companies that combine the reach of embedded finance, the precision of AI-powered credit assessment, and the efficiency of AI-enhanced operations. These companies don’t compete with traditional banks on their terms—they create entirely new categories of financial services that traditional institutions cannot easily replicate, particularly in emerging markets where legacy infrastructure is limited.

Conclusion: From $180 Billion to Global Embedded Finance Leadership

As we look toward 2030 and the $180 billion Southeast Asian digital financial services market, it’s important to recognize that this figure represents not just a destination, but a launching pad for global embedded finance dominance. The companies that will capture the largest share of this regional opportunity—and then leverage it for global expansion—are those that successfully integrate embedded finance with AI-powered credit assessment and operational efficiency into cohesive platforms that serve real customer needs profitably and at scale.

The evidence from Insignia Ventures Partners’ portfolio companies demonstrates that this convergence is creating platforms with global potential. Surfin’s AI-powered financial inclusion platform, already serving 60 million users across nine markets, exemplifies the global scalability of alternative credit scoring models embedded into diverse customer journeys. AwanTunai’s supply chain finance solution addresses universal challenges in FMCG distribution that exist across Latin America, Africa, and South Asia. Meanwhile, enterprise-focused companies like Fluid and Finmo are building B2B financial infrastructure that transcends geographic boundaries, and consumer-focused platforms like Carro and Pinhome demonstrate how embedded financing can transform major purchase experiences globally.

The portfolio companies mentioned across the three global expansion segments—Carro and Pinhome in consumer finance, AwanTunai in SMB supply chain finance, and Fluid and Finmo in enterprise solutions—represent different pathways to capturing shares of the $320 billion global embedded finance opportunity. Each has proven their model in Southeast Asia’s challenging and diverse markets, positioning them to expand into the much larger global opportunity with AI-powered operational advantages and deep emerging market expertise.

The $180 billion Southeast Asian opportunity is not just about market size—it’s about the fundamental transformation of financial services from institution-centric to customer-centric, from product-focused to platform-based, and from human-powered to AI-enhanced. Southeast Asia’s unique combination of demographic dividend, mobile-first infrastructure, and regulatory innovation creates the perfect environment for this transformation to accelerate and scale globally through embedded finance models.

The future of fintech is being written in Southeast Asia, and it’s embedded, AI-powered, and globally scalable. The question is not whether this convergence will reshape global financial services, but how quickly and how broadly Southeast Asian embedded finance champions will capture their share of the global $320 billion market. With proven models, battle-tested technology, and deep emerging market expertise, they are uniquely positioned to lead this global transformation.

This article is based on market research and analysis of Southeast Asia’s fintech ecosystem, including insights from Insignia Ventures Partners’ portfolio companies and industry data from various sources including KPMG, Royal Park Partners, Grab Holdings, McKinsey, and BCG & QED Investors.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.