When people ask me what Fluid does, I often get puzzled looks. “So you’re another SME lender?” they ask. Or, “You’re doing invoice financing, right?” While these aren’t entirely wrong, they’re missing the bigger picture. We’re not just improving cash flow—we’re rebuilding how B2B payments move across Asia. And to understand why this matters, we need to look at what Bill.com accomplished in the United States, and why Asia needs something fundamentally different.

Editor’s Note: This article was based on Fluid CEO and co-founder Trasy Lou Walsh’s LinkedIn post.

The Bill.com Blueprint: Digitizing American B2B Payments

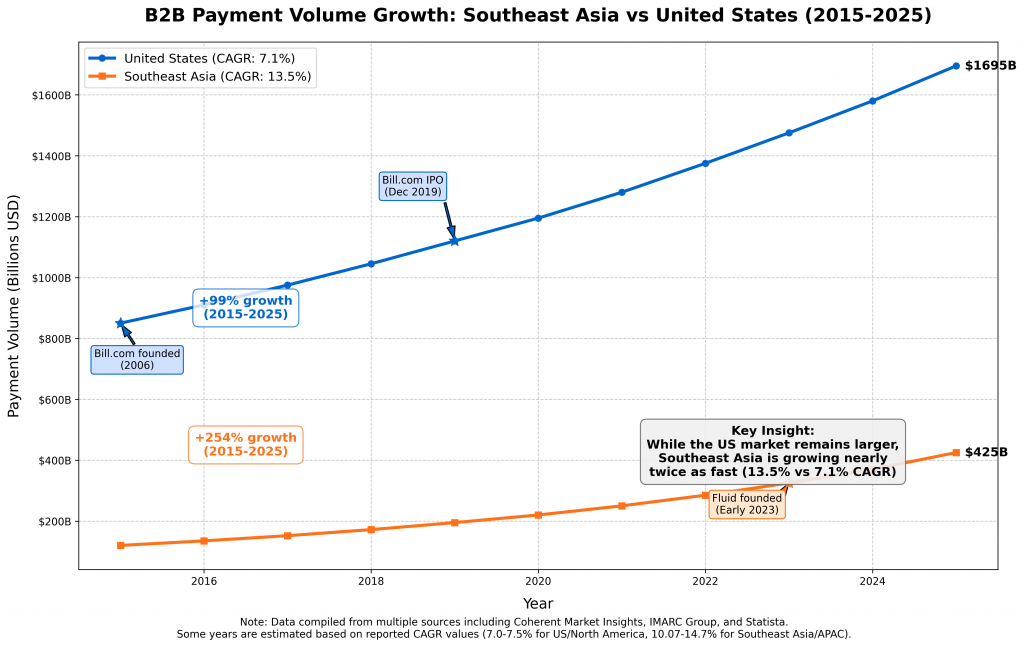

Bill.com’s story is one of the fintech success stories of the past decade. When René Lacerte founded the company in 2006, American small and medium businesses were drowning in paper-based processes. A 2016 survey revealed that 44% of B2B payments were still made by check—an astounding figure for a digitally native economy. Bill.com saw an opportunity to digitize these workflows, and they executed brilliantly.

The company built a comprehensive platform that integrated seamlessly with existing accounting software like QuickBooks and Xero. They automated accounts payable and receivable processes, enabled ACH transfers and wire payments, and gave businesses a single dashboard to manage their entire financial operations. The results speak for themselves: Bill.com went public in 2019 at a $1.6 billion valuation and today commands a market capitalization of over $4.2 billion, with annual revenues exceeding $1.3 billion.

But here’s what made Bill.com truly transformative—they didn’t just digitize existing processes. They reimagined how B2B payments could work when freed from the constraints of paper-based systems. Instead of businesses manually creating invoices, chasing approvals, and reconciling payments across multiple systems, Bill.com created a unified workflow where everything happened automatically within their platform.

The American market was ripe for this transformation. Businesses already had established ERP systems, standardized accounting practices, and a regulatory environment that supported digital payments. Bill.com could focus on building elegant software that connected these existing pieces together.

Asia’s Different Reality: Why Digitization Alone Isn’t Enough

Chart added by Insignia Business Review to illustrate Trasy’s sharing

When we start thinking about B2B payments in Asia, one could initially assume we can follow the Bill.com playbook. Build great software, integrate with existing systems, and watch businesses transform their operations. But the more time we spend with suppliers and buyers across Southeast Asia, the more we realize that Asia’s challenges are fundamentally different from what Bill.com solved in America.

Let me paint you a picture of how B2B payments actually work in most Asian markets today. A supplier takes orders via WhatsApp messages or phone calls from sales reps. Maybe a small percentage of their sales happen through online marketplaces or B2B websites, but the majority is still relationship-driven and offline. When goods are delivered, invoices are often issued manually—sometimes only when the products physically arrive at the buyer’s location. The buyer’s finance team then has to hunt through paper proof-of-delivery documents, signatures, and screenshots to verify what’s been delivered before they can process payment.

Then comes the waiting game. Suppliers typically wait 30 to 90 days to get paid, during which time they’re constantly chasing buyers for updates. When payments finally do arrive, reconciliation becomes a nightmare as money comes in through various channels—bank transfers, credit cards, QR codes, mobile wallets—each requiring manual matching against outstanding invoices.

This isn’t just a digitization problem. It’s a fundamental infrastructure problem. Unlike the United States, where businesses had established systems that needed to be connected, many Asian businesses are operating with fragmented, informal processes that need to be completely reimagined.

The AI-First Approach: Building Intelligence Into Every Transaction

This is where Fluid’s approach diverges from the Bill.com model. While Bill.com focused on connecting existing systems, we’re building intelligence directly into the payment infrastructure itself. Our proprietary technology makes instant credit decisions, allowing suppliers to get paid on Day 1 while buyers maintain their preferred 30-90 day payment terms. This isn’t just about improving cash flow—it’s about fundamentally changing the risk dynamics of B2B trade.

Our automated collection AI agent handles payment reminders and follow-ups, understanding cultural nuances and communication preferences across different markets. Instead of suppliers having to chase payments manually, AI collection agents proactively manage the entire collection process while maintaining business relationships.

Perhaps most importantly, our automated reconciliation process eliminates the need for manual matching of payments to invoices. The system streamlines workflows so businesses never miss a beat, handling the complexity that makes Asian B2B payments so challenging.

This technology-first approach allows us to handle the complexity that makes Asian B2B payments so challenging. We’re not just digitizing existing processes—we’re creating entirely new capabilities that weren’t possible before.

Chart added by Insignia Business Review to illustrate Trasy’s sharing

Embedded Finance: Credit as Infrastructure, Not Product

The other key difference in our approach is how we think about credit. Bill.com offers some financing options, but their core business is software-as-a-service. Credit is an add-on product. In Asia, we’ve learned that credit needs to be embedded directly into the payment infrastructure itself.

When a supplier uploads an invoice to our platform, our proprietary technology instantly evaluates the creditworthiness of both the supplier and buyer, the specific transaction details, and other risk factors. If approved, the supplier gets paid immediately while the buyer maintains their standard payment terms. This isn’t invoice factoring or traditional trade finance—it’s embedded lending that happens seamlessly within the normal flow of business.

This embedded approach is crucial in markets where access to working capital is often the biggest constraint on business growth. By making credit invisible and automatic, we’re removing friction from the entire B2B ecosystem.

Building for How Asia Actually Does Business

One of the biggest lessons I’ve learned is that successful fintech in Asia requires deep integration with how businesses actually operate, not how we think they should operate. While Bill.com could assume that American businesses would adapt their processes to use new software, Asian businesses need solutions that adapt to their existing workflows.

That’s why we’ve built direct integrations with ERP systems like Xero, QuickBooks, Microsoft, and NetSuite for businesses that sell offline, and plug-in checkout solutions for those selling through B2B order apps, marketplaces or websites. We support flexible payment terms that businesses actually need, from immediate payment to traditional net terms.

We’ve also learned that relationship management remains crucial in Asian business culture. Our platform doesn’t try to eliminate human relationships—it enhances them by removing administrative friction while preserving the personal connections that drive business.

From Fluid website gofluid.io

The Network Effect: Building Asia’s B2B Payment Infrastructure

What excites me most about what we’re building is the network effect potential. As more suppliers and buyers join the Fluid platform, the value for everyone increases exponentially. Suppliers get faster access to a broader base of creditworthy buyers. Buyers get streamlined procurement processes and better payment terms. Platforms and marketplaces can offer embedded financing to their merchants without building complex credit infrastructure themselves.

We’re not just building a product—we’re building the foundational infrastructure for how B2B payments will work across Asia. Every transaction that flows through our network makes the system smarter, more efficient, and more valuable for all participants.

Looking Forward: The Future of B2B Payments

Bill.com proved that there was enormous value in digitizing B2B payments. They built a $4+ billion company by solving this problem for American businesses. But Asia’s opportunity is even larger. The region’s B2B payment volumes are massive and growing rapidly, driven by the expansion of digital commerce and cross-border trade.

More importantly, by building AI and embedded finance directly into the payment infrastructure, we have the opportunity to create something that’s not just better than existing solutions—it’s fundamentally different. We’re not just making B2B payments faster or cheaper. We’re making them intelligent, predictive, and seamlessly integrated into the flow of business itself.

The businesses that adopt this new infrastructure will have significant competitive advantages. They’ll have better cash flow, lower administrative costs, and access to credit that scales with their growth. The platforms and marketplaces that integrate our solutions will be able to offer their merchants capabilities that standalone competitors simply can’t match.

This is why I’m so excited about what we’re building at Fluid. We’re not just creating another fintech product. We’re building the foundation for how business will be conducted across Asia in the coming decades. And unlike the incremental improvements that most B2B payment solutions offer, we’re creating something that’s genuinely transformative.

The future of B2B payments isn’t just digital—it’s intelligent. And that future is being built right here in Asia.

Fluid is more than a financing fintech. Fluid team at SuperAI 2025 conference.

Trasy Lou Walsh is CEO and Co-founder of Fluid. Prior to Fluid, she was Regional General Manager at BNPL startup Atome. Before that she was Head of Restaurant Operations at Uber Eats Asia Pacific. She received her MBA from HKUST Business School as well as an executive education at Harvard Business School.