This article is an adaptation of a presentation delivered by Insignia Ventures Partners principal Yongcheng Ong on The Southeast Asia Edge in the US$10 Trillion AI Revolution at the Tencent Cloud x Insignia Chinese New Year Luncheon 2026.

The artificial intelligence (AI) revolution, a market projected to be worth at least US$10 trillion, is not just a technological shift; it is a significant reshaping of work, supply chains, and the global balance of power [1][2][3]. While the Industrial Revolution took 144 years to move from the steam engine to the assembly line, the cognitive revolution is on a faster trajectory, poised to move from the GPU to a “cognitive assembly line” in just 17 years [4].

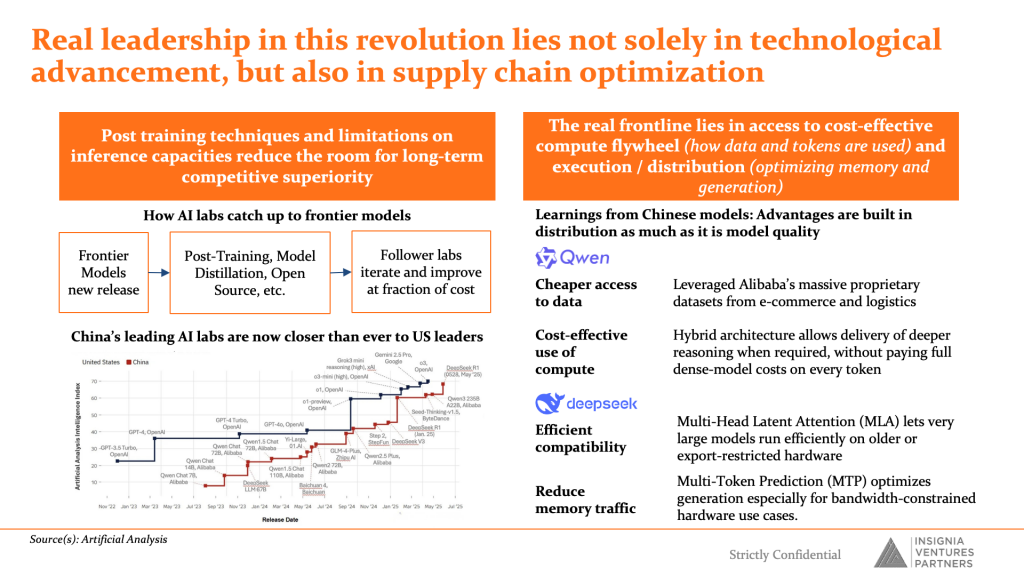

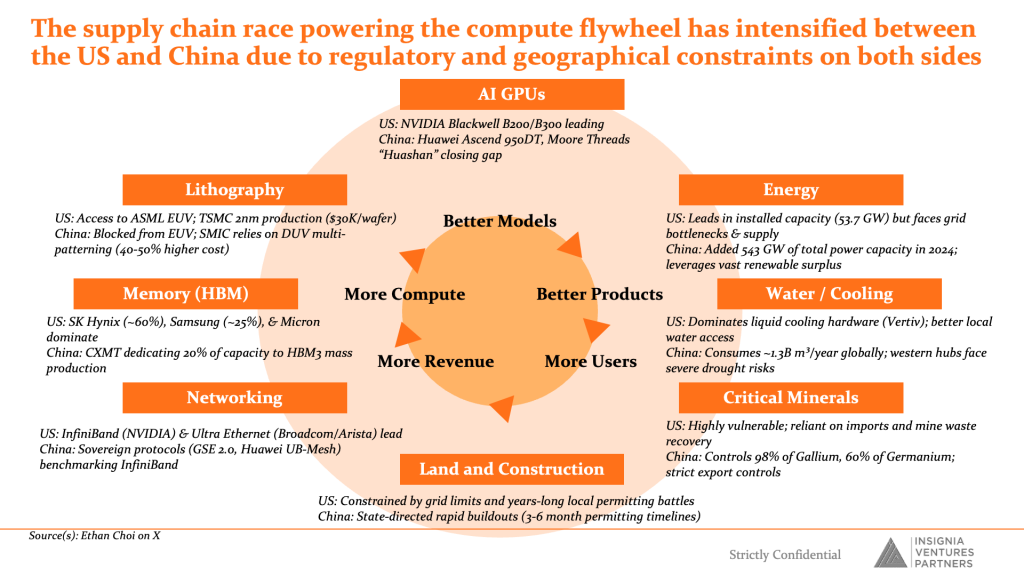

Real leadership in this new era will not be determined by technological superiority alone, but by the optimization of supply chains and the efficiency of distribution. As we have seen with the rapid advancements in Chinese AI models, which are now closer than ever to their US counterparts, competitive advantages are built as much in distribution as they are in model quality [5][6]. The race to build and control the AI supply chain—from GPUs and memory to critical minerals and data centers—has intensified, particularly between the US and China, with each facing its own set of regulatory and geographical constraints.

The Global AI Supply Chain Race

The competition across the AI supply chain is intense. In the realm of AI GPUs, the US leads with NVIDIA’s Blackwell series, while China is closing the gap with Huawei’s Ascend 950DT and other domestic chips [7][8]. The US has access to advanced lithography through ASML, while China is developing its own capabilities with DUV multi-patterning, albeit at a higher cost. This dynamic plays out across the entire supply chain, from energy and memory to cooling and networking, with both nations vying for dominance.

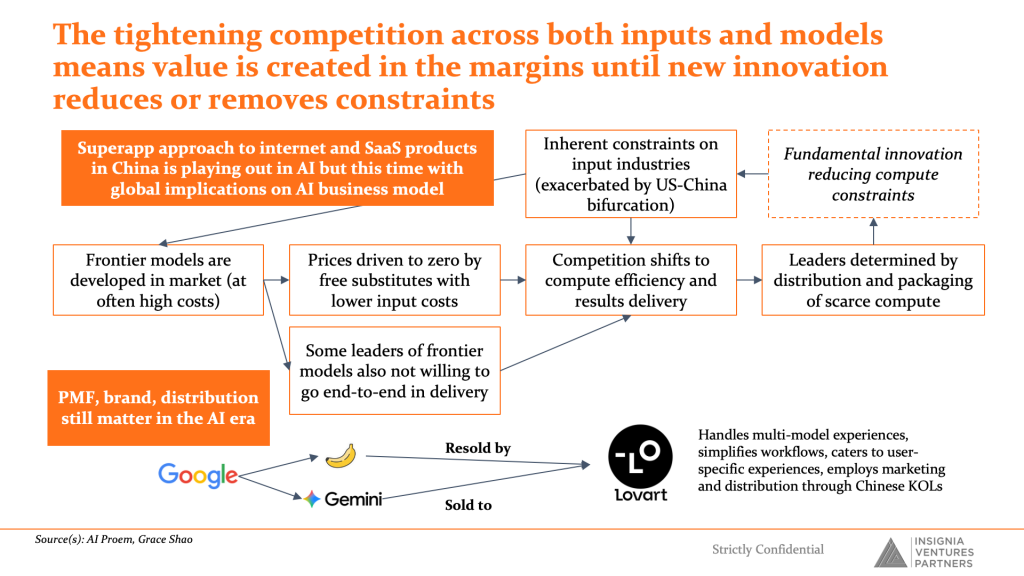

This intense competition means that value is created in the margins. As we saw during the Chinese New Year in 2026, the battle for AI supremacy is being fought not just in the lab, but in the market, with companies like Alibaba, ByteDance, Tencent, and Baidu leveraging the holiday to drive mass adoption of their AI applications [9].

The Southeast Asia Opportunity: From Follower to Frontier

So, where does this leave a region like Southeast Asia, situated outside the primary US and China bubbles? The opportunity is not necessarily in making the “factories” or the “cars” of the AI revolution, but in getting people to switch from their “horses” and, in the process, learning to build their own unique vehicles. The region is poised to cacarve out a unique and strong role, defined by five key opportunities.

1. Leapfrogging from Mobile-First to AI-Native

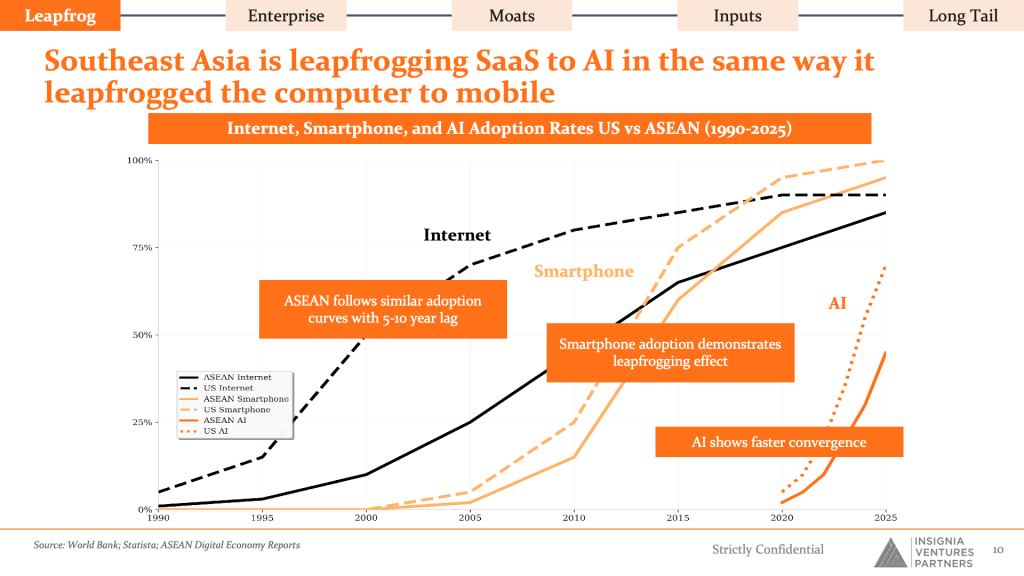

Just as Southeast Asia largely skipped the desktop era and went straight to mobile, it is now positioned to leapfrog the traditional, cumbersome Software-as-a-Service (SaaS) model and embrace AI-native solutions. This is highlighted by the fact that “Southeast Asia is leapfrogging SaaS to AI in the same way it leapfrogged the computer to mobile.”

This trend is rooted in two fundamental realities of the region:

- A Culture of Ownership: With an average homeownership rate of 80% compared to 65% in the US, the region has a cultural preference for ownership over access. This translates into a desire for more control and customization in digital solutions, which AI-native products can offer.

- Digital-First, but Cloud-Poor: While e-commerce penetration in markets like Indonesia is high (over 30%), the adoption of cloud services by businesses in the region (32%) lags significantly behind markets like the US and Australia (over 70%). This creates an opening for AI solutions that are not dependent on heavy, pre-existing cloud infrastructure.

This leapfrog effect means there are lower switching costs and less entrenched legacy systems, allowing for faster, more widespread adoption of AI-powered tools.

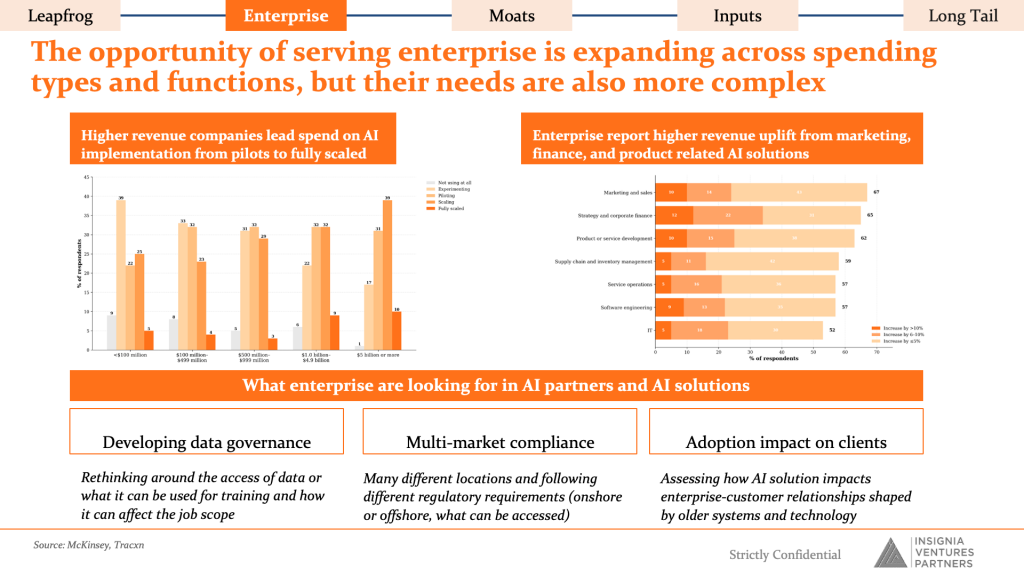

2. The Untapped Enterprise Goldmine

While individual AI adoption is soaring—with 75% of employees in Singapore using AI tools—a significant gap remains at the organizational level. Only 15% of SMEs in Singapore have integrated AI at an enterprise level. This disparity highlights a large, underserved market. The challenge, then, is “how do you translate individual adoption of AI to organizational outcomes?”

The opportunity lies in bridging the gap between simple, task-based automation and enterprise-level transformation. While 92% of AI startups in Southeast Asia are B2B-focused, a high 95% of generative AI projects globally fail to deliver a return on investment (ROI). The companies that succeed will be those that can address the complex needs of enterprises, including:

- Data Governance: Developing robust frameworks for how data is accessed, used for training, and how it impacts job roles.

- Multi-Market Compliance: Navigating the diverse regulatory requirements across the region, from data sovereignty laws to onshore/offshore rules.

- Client Adoption Impact: Assessing how new AI solutions will affect long-standing enterprise-customer relationships that were built on older technologies.

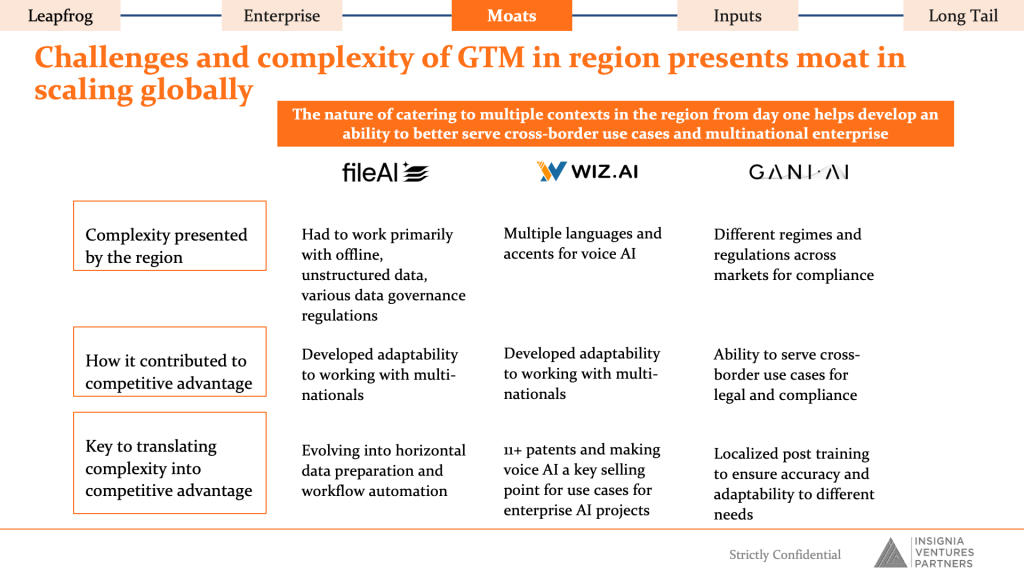

3. The Go-to-Market Moat: Forging a Fortress out of Fragmentation

The very complexity of Southeast Asia’s go-to-market landscape—often perceived as a challenging barrier—can be forged into a strong, long-term competitive moat. Companies that embrace the region’s fragmented tapestry of languages, regulations, and infrastructure from day one develop a unique “operational muscle” that is difficult for outsiders to replicate. This complexity forces a deep competency in localization, which evolves into a significant competitive advantage.

Let’s take a deeper look at the voice AI startup example. To be viable across the region, it can’t just support English and Mandarin. It needs to master Bahasa Indonesia with its various regional accents, Tagalog and its Cebuano variant, and the tonal complexities of Thai and Vietnamese. This is not a one-off task; it requires a massive, ongoing effort in sourcing and cleaning local, often offline and unstructured, data.

The startup must build relationships with local call centers to access conversational data, navigate the Personal Data Protection Act (PDPA) in Singapore, the PDP Law in Indonesia, and other data sovereignty regulations that differ from market to market. The engineering team has to build a system that can handle different legal requirements for data storage and processing. This demanding, front-loaded effort results in a portfolio of patents and a voice AI engine that understands the nuances of the region with high accuracy. This becomes a key selling point for any regional enterprise, and a barrier that a global competitor, used to more homogenous markets, would find costly and time-consuming to overcome.

This “GTM moat” is not limited to voice AI. Consider a fintech company building a compliance engine. To operate in Indonesia, it must integrate with Bank Indonesia’s regulatory sandbox. In the Philippines, it must comply with the Bangko Sentral ng Pilipinas’s rules on e-money issuers. In Vietnam, it must navigate the State Bank of Vietnam’s licensing requirements.

A company that builds a single, unified API that can handle this multi-jurisdictional complexity has created a valuable asset that can be licensed to other companies, effectively turning a regulatory headache into a revenue stream. Similarly, a logistics startup that builds a network of micro-warehouses in rural Thailand, managed by local entrepreneurs using a simple mobile app, creates a last-mile delivery network that is difficult for a large, centralized competitor to replicate. In each case, the initial struggle with fragmentation becomes the foundation of a long-term, defensible business.

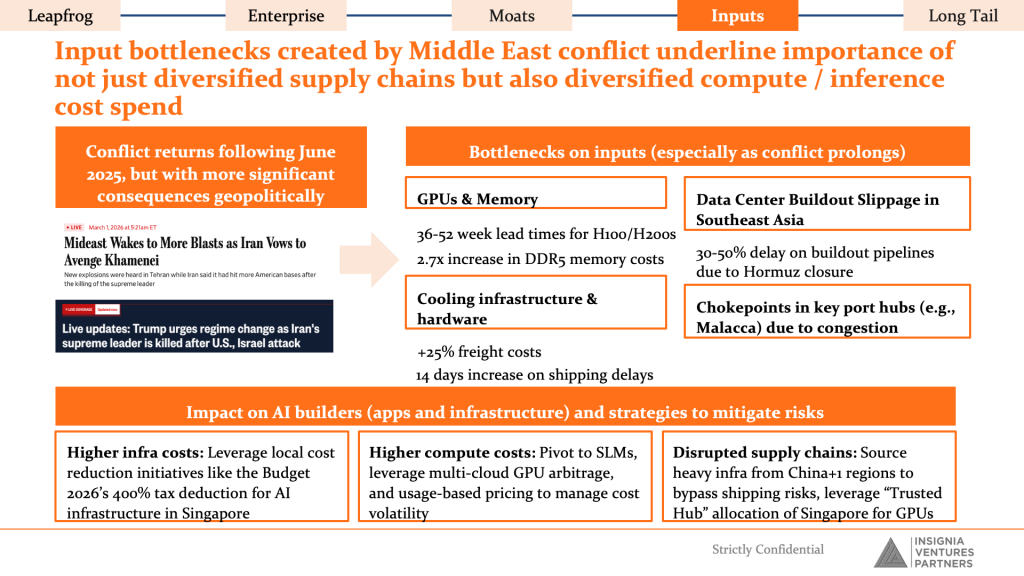

4. A Critical Role in the Diversified AI Supply Chain

As geopolitical tensions between the US and China push for a decoupling of supply chains, the strategic importance of Southeast Asian markets is growing. The region is no longer just a consumer of technology but a critical node in the global AI supply chain.

“As the US and China seek to reduce bilateral interdependencies, competitive advantages of Asian markets become more attractive.”

This is particularly evident in the semiconductor industry, where countries like Singapore, Malaysia, and Vietnam play key roles in manufacturing, assembly, and R&D. Furthermore, the recent conflicts in the Middle East have highlighted the fragility of global supply chains and the need for diversified compute and inference cost spend. The impact of these disruptions is clear:

- Higher Infrastructure Costs: Delays in data center buildouts and increased freight costs are forcing companies to look for local solutions and tax incentives, such as Singapore’s 400% tax deduction for AI infrastructure.

- Higher Compute Costs: Volatility in GPU and memory prices is pushing a pivot to smaller, more efficient models (SLMs) and multi-cloud GPU arbitrage.

- Disrupted Supply Chains: Sourcing infrastructure from China+1 regions and leveraging “Trusted Hub” allocations for GPUs are becoming critical strategies.

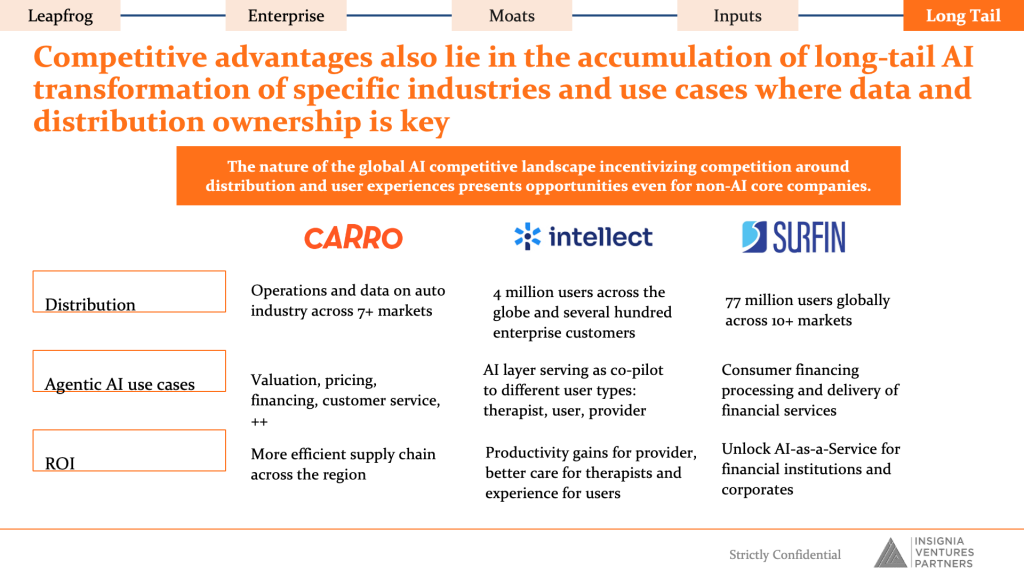

5. The Long-Tail Transformation

Finally, competitive advantages in the AI era will be accumulated in the “long-tail” transformation of specific industries where data and distribution ownership are paramount. Companies with deep, proprietary datasets and a large, engaged user base are uniquely positioned to build a powerful AI layer on top of their existing operations.

There are several examples of this in action:

- An automotive platform with operations across 7+ markets can use its data to build AI-powered tools for valuation, pricing, and customer service, creating a more efficient regional supply chain.

- A mental health platform with millions of users can develop an AI co-pilot to assist therapists, users, and providers, leading to better care and higher productivity.

- A financial services company can leverage its user base to create AI-as-a-Service offerings for other institutions, unlocking new revenue streams.

Navigating the Path Forward: From Opportunities to Impact

The AI revolution is here, and it is moving at a rapid pace. For Southeast Asia, the path forward is not to compete head-on with the US and China in a race to the bottom on cost, but to carve out a unique position in the global AI ecosystem. The five key opportunities outlined above translate directly into a set of strategic imperatives for AI-native companies in the region. Here’s a deeper look at what these opportunities mean in practice:

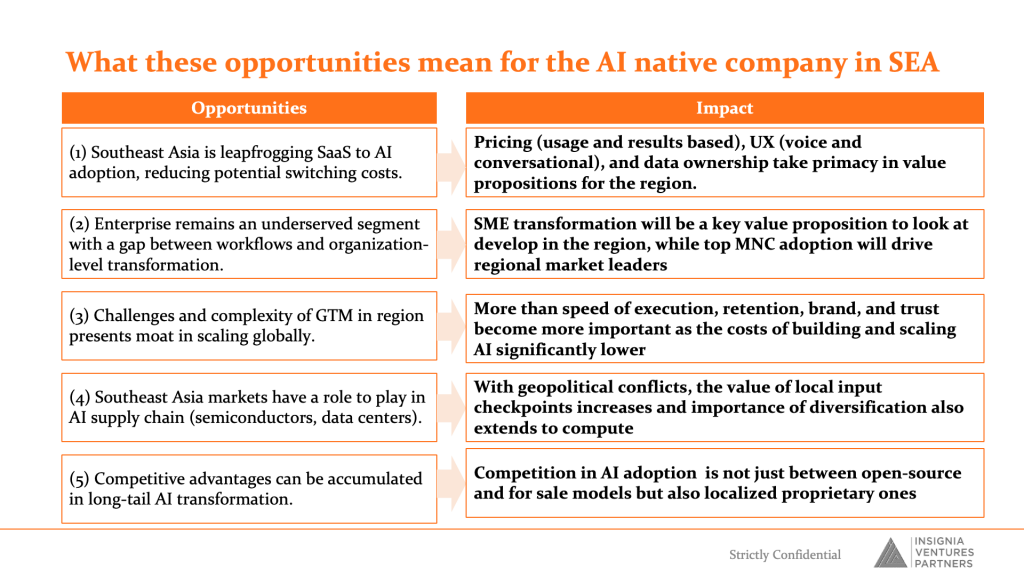

- Leapfrogging SaaS to AI Adoption: A New Value Proposition

- The Impact: Pricing (usage and results based), UX (voice and conversational), and data ownership take primacy in value propositions for the region.

Because Southeast Asia is not encumbered by legacy SaaS systems, there is a unique opportunity to redefine the value proposition of enterprise software. Instead of the traditional, rigid subscription models, AI-native companies can pioneer usage-based or results-based pricing, aligning their revenue directly with the value they create for their customers. The user experience can be built from the ground up around intuitive, conversational interfaces, making powerful AI tools accessible to a much broader audience. And in a region that culturally values ownership, building business models around data ownership and portability will be a strong competitive advantage.

- The Underserved Enterprise Segment: A Two-Pronged Approach

- The Impact: SME transformation will be a key value proposition to look at develop in the region, while top MNC adoption will drive regional market leaders.

This creates a two-pronged strategy for ambitious founders. On one hand, there is a large, untapped market in providing simple, affordable, and high-impact AI solutions to the millions of SMEs that form the backbone of the region’s economies. This is a volume play that requires a deep understanding of local business needs. On the other hand, landing flagship contracts with the large multinational corporations that operate in the region will be crucial for building brand credibility, attracting top talent, and establishing market leadership. The companies that can successfully execute this dual strategy will be the ones that dominate the enterprise AI landscape.

- The GTM Moat: Trust as the Ultimate Currency

- The Impact: More than speed of execution, retention, brand, and trust become more important as the costs of building and scaling AI significantly lower.

As the cost of building and scaling AI products continues to fall, the competitive advantage will shift from pure technology to the strength of a company’s brand and the trust it has earned from its customers. The deep, operational moat built by navigating the complexities of the region’s go-to-market landscape must be reinforced by a relentless focus on customer retention and brand building. In a world of AI abundance, trust is the scarcest and most valuable resource.

- The AI Supply Chain: From Consumer to Critical Hub

- The Impact: With geopolitical conflicts, the value of local input checkpoints increases and importance of diversification also extends to compute.

Geopolitical tensions are creating a once-in-a-generation opportunity for Southeast Asia to move from being a consumer of technology to a critical hub in the global AI supply chain. For founders, this means thinking beyond their own product and looking for opportunities to become a key “input checkpoint,” whether by providing specialized data, developing a unique hardware component, or offering a critical service. It also means that diversifying their own compute resources, leveraging a multi-cloud strategy, and tapping into local data centers will be essential for mitigating risk and ensuring business continuity.

- Long-Tail AI Transformation: The Power of Proprietary Data

- The Impact: Competition in AI adoption is not just between open-source and for sale models but also localized proprietary ones.

While open-source models provide a powerful foundation, the strongest competitive advantages will be built by companies that can create localized, proprietary models trained on unique, hard-to-replicate datasets. This is the “long-tail” of AI transformation, where deep industry knowledge and proprietary data are combined to create solutions that are significantly better than anything a generic, off-the-shelf model can provide. This is where the strongest moats will be built, and where the true category-defining companies of the AI era in Southeast Asia will emerge.

References

[1] Cathie Wood sees AI driving US$10 trillion global robotaxi revolution. (2025, March 27). South China Morning Post. Retrieved from https://www.scmp.com/business/banking-finance/article/3304100/cathie-wood-sees-ai-driving-us10-trillion-global-robotaxi-revolution

[2] Could Nvidia Become the World’s First $10 Trillion Company? (2026, February 23). Streetwise Reports. Retrieved from https://www.streetwisereports.com/article/2026/02/23/could-nvidia-become-the-worlds-first-10-trillion-company.html

[3] Sequoia’s AI cheat sheet: 5 trends today, 5 themes tomorrow. (2025, September 2). Tech in Asia. Retrieved from https://www.techinasia.com/sequoia-ai-believes-purpose-replacement-expansion

[4] Does the Rise of AI Compare to the Industrial Revolution? ‘Almost … (2024, April 16). Columbia Business School. Retrieved from https://business.columbia.edu/research-brief/research-brief/ai-industrial-revolution

[5] Is China quietly winning the AI race? (2026, January 23). BBC News. Retrieved from https://www.bbc.com/news/articles/c86v52gv726o

[6] The best Chinese open-weight models. (2025, December 15). Understanding AI. Retrieved from https://www.understandingai.org/p/the-best-chinese-open-weight-models

[7] Huawei debuts top AI supercomputer overseas in … (2026, March 1). Nikkei Asia. Retrieved from https://asia.nikkei.com/business/china-tech/huawei-debuts-top-ai-supercomputer-overseas-in-challenge-to-nvidia

[8] Huawei’s Ascend and Kunpeng progress shows how … (2025, December 31). Tom’s Hardware. Retrieved from https://www.tomshardware.com/tech-industry/semiconductors/huaweis-ascend-and-kunpeng-progress-shows-how-china-is-rebuilding-an-ai-compute-stack-under-sanctions

[9] China’s AI titans are giving away money and cars to try and … (2026, February 13). CNBC. Retrieved from https://www.cnbc.com/2026/02/13/china-ai-lunar-new-year-bytedance-baidu-tencent-alibaba.html

[10] Taking enterprise AI transformation in Southeast Asia from the fringe to the core. (2026, February 27). Insignia Business Review. Retrieved from https://review.insignia.vc/2026/02/27/enterprise-ai/

[11] Konstantine Buhler. “Video: The $10 Trillion AI Revolution.” Sequoia Capital. (08/28/2025). Retrieved from https://sequoiacap.com/article/10t-ai-revolution/

[12] Ethan Choi. “The Global AI Battle Part 1 of 2: U.S. vs. China.” X. (02/27/2026). Retrieved from https://x.com/EthanChoi7/status/2025143362010136807

[13] Grace Shao. “Part I: The Gala, the Suburbs, and the ‘Months Behind’ Myth in LLM Labs.” AI Proem. (02/20/2026). Retrieved from https://aiproem.substack.com/p/part-i-the-gala-the-suburbs-and-the

[14] Grace Shao. “Part II: How to Understand China’s.” AI Proem. (02/2026). Retrieved from https://aiproem.substack.com/p/part-ii-how-to-understand-chinas

[15] Grace Shao. “Part III: China’s Super Bowl, the Spring.” AI Proem. (02/2026). Retrieved from https://aiproem.substack.com/p/part-iii-chinas-super-bowl-the-spring

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.

Yongcheng Ong is Principal at Insignia Ventures Partners. Previously he spent three years at China-based Qiming Ventures as an associate for their investment team in Southeast Asia and before that was part of Sea Group’s Corporate Development and Strategy team as well as Deutsche Bank’s Structured Commodity Finance team. He graduated from Nanyang Technological University with a Bachelor’s Degree in Accountancy.