The best companies in early cancer diagnosis will own workflow, not just the model.

Every company building AI for cancer detection wants to lead with model performance: sensitivity, specificity, Area Under the Curve (AUC). Those metrics matter, but they are not the real bottleneck. In cancer care, value does not accrue to the algorithm that performs best in a benchmark. It accrues to the company that gets adopted inside a messy, capacity-constrained clinical workflow.

That distinction matters even more in Southeast Asia. The region does not just need better models. It needs faster reads, earlier referrals, fewer missed cases, and more consistent access to specialist expertise. In markets where radiologists and pathologists remain in short supply, AI is not a substitute for clinicians. It is leverage.

Accuracy vs Adoption

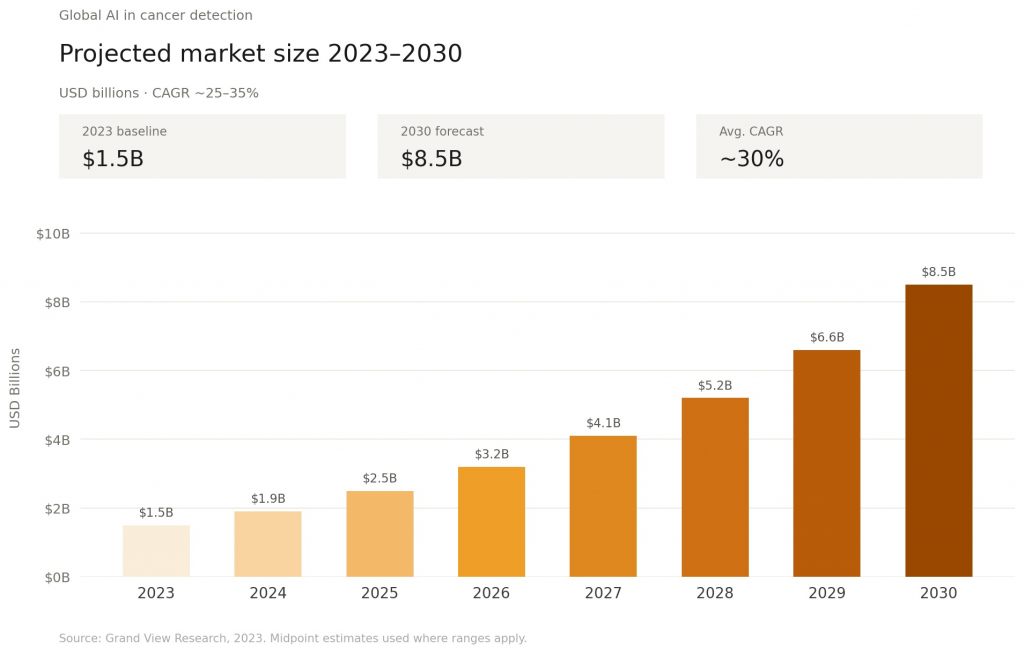

AI in cancer detection is one of the clearest applied AI opportunities in healthcare. Imaging, pathology, endoscopy, and genomics all produce data-rich workflows where machine learning can help surface weak signals earlier and more consistently. Market estimates already point to a category that could exceed US$5 billion to US$10 billion by 2030, supported by better algorithms, expanding datasets, and the broader push toward precision medicine 1.

But technical performance alone does not create durable companies. Hospitals do not buy “AI” in the abstract. They buy faster turnaround times, lower false negatives, fewer unnecessary follow-ups, and better use of specialist capacity. Accuracy gets attention. Workflow fit gets adoption.

That is why the strongest products in this category tend to look less like standalone software and more like embedded infrastructure. They help clinicians prioritise cases, standardise first reads, and reduce delays without forcing hospitals to redesign how care is delivered.

Exhibit 1: AI Cancer Detection Market Growth and Workflow Bottlenecks

Where Value Accrues First

Not every detection and diagnosis workflow is equally ready for AI. Near-term value sits where three conditions hold: the data is already digitised, the diagnostic burden is high, and clinical action can follow quickly.

Breast imaging fits that pattern. So does digital pathology in high-volume centres. Endoscopy is another strong wedge, especially when real-time detection support can improve outcomes during the procedure itself. These are not necessarily the broadest stories in oncology. They are the most commercially legible ones.

By contrast, liquid biopsy and multi-modal platforms may define the longer-term frontier, but they usually require more regulatory complexity, deeper clinical partnerships, and longer adoption cycles. The first category leaders are more likely to be companies solving a specific bottleneck well than companies trying to reinvent oncology end to end.

Who’s Winning

The competitive landscape already shows how the market is segmenting. In radiology, companies such as Lunit have shown how AI can be integrated into screening workflows rather than positioned as a research tool alone 2. In pathology, companies such as Paige and PathAI have pushed digital slide analysis toward clinically relevant decision support. In endoscopy, the value proposition is even more immediate: better detection inside the procedure, with measurable workflow benefits.

What separates the strongest companies is not just model quality. It is access to proprietary clinical data, regulatory progress, physician trust, and the ability to fit into hospital systems without adding friction. In healthcare, the best product is often the one clinicians barely notice because it fits naturally into how they already work.

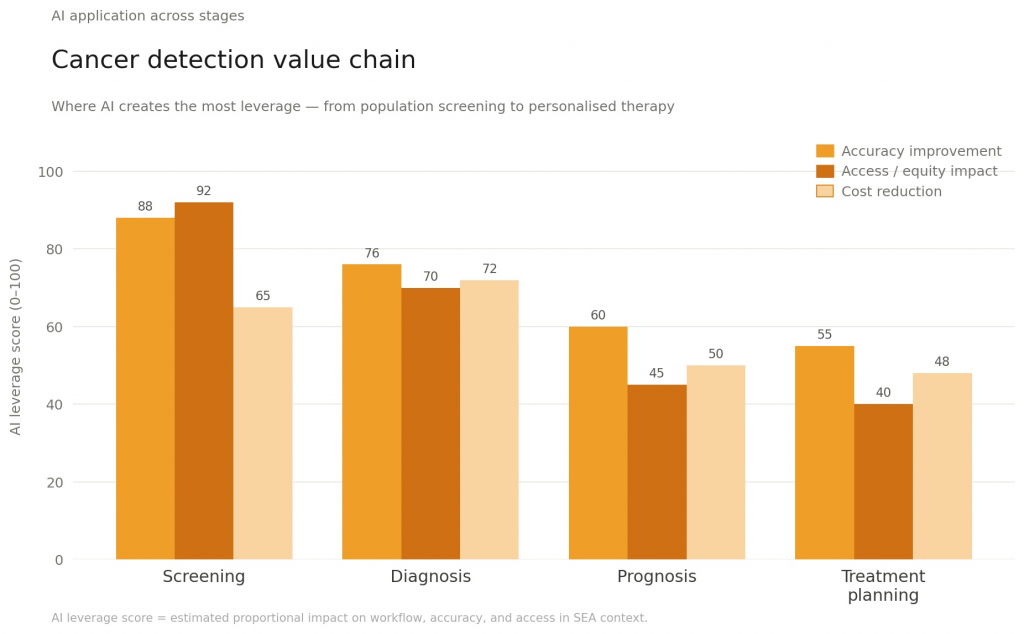

Exhibit 2: Cancer detection value chain

The Southeast Asia Position

Southeast Asia is unlikely to produce the global winner in every layer of AI cancer detection. The regional opportunity is more specific, and in many ways more compelling.

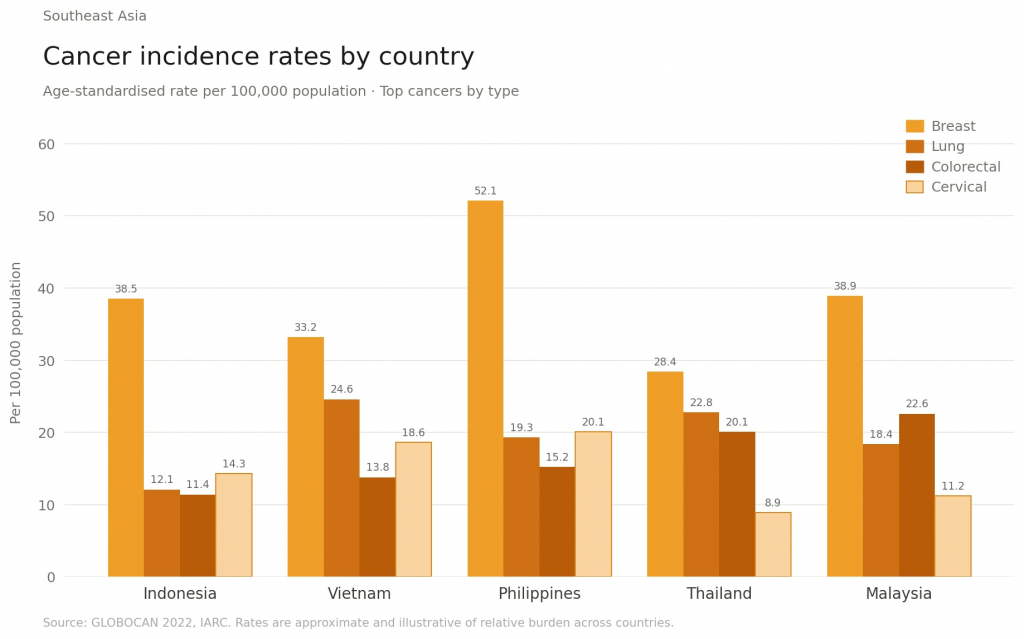

Cancer incidence is rising across the region, while access to specialist interpretation remains uneven. Large urban centres may have stronger capabilities, but secondary cities and rural areas often face diagnostic backlogs, fragmented infrastructure, and inconsistent access to trained specialists. That makes Southeast Asia an especially strong market for diagnostic augmentation.

The best regional companies will not win by building a generic AI platform and hoping hospitals adapt around it. They will win by solving for local constraints: variable digital maturity, cross-border regulatory complexity, limited specialist density, and the need to prove ROI quickly to healthcare providers.

The playbook is straightforward. Own the workflow where delay is expensive. Become the layer that helps hospitals flag suspicious cases earlier, triage scans more consistently, and move patients to specialist review faster. In Southeast Asia, the wedge is not just better AI. It is better clinical throughput.

This is also where regional defensibility can emerge. Global leaders may continue to dominate the underlying models, but local companies can still own implementation, distribution, and trust across fragmented healthcare systems. In a market like Southeast Asia, that is not a secondary role. It may be the most investable one.

Exhibit 3: Southeast Asia Cancer Incidence Rates by Country

What We’re Looking For

When evaluating AI cancer detection companies, the signal is not a polished demo or a benchmark result in isolation. It is evidence that the product changes clinical behaviour.

We would look for strong clinical validation, a clear regulatory path, access to differentiated datasets, and integration that does not require a hospital to rebuild its workflow from scratch. We would also look for narrow, high-frequency use cases where ROI is measurable: fewer missed cases, faster turnaround times, better specialist productivity, or expanded screening capacity.

Most of all, we would look for companies that understand a hard truth about healthcare adoption: it compounds more slowly than software, but once embedded, it becomes far harder to displace.

The biggest companies in AI cancer detection will not be the ones with the most impressive model demo.

They will be the ones that make early diagnosis easier to deliver at scale.

And in Southeast Asia, that may matter more than anywhere else.

References

[1] Grand View Research — AI in Cancer Diagnostics Market Size, Share & Trends Analysis Report