For a while, the stablecoin story looked like a dollar story.

That made sense. If crypto’s earliest mainstream use cases were trading, treasury management, and moving value across borders faster than banks could, then a dollar-denominated instrument had obvious advantages. It was liquid, familiar, and legible to a market already organized around the greenback.

But that framing is starting to break down.

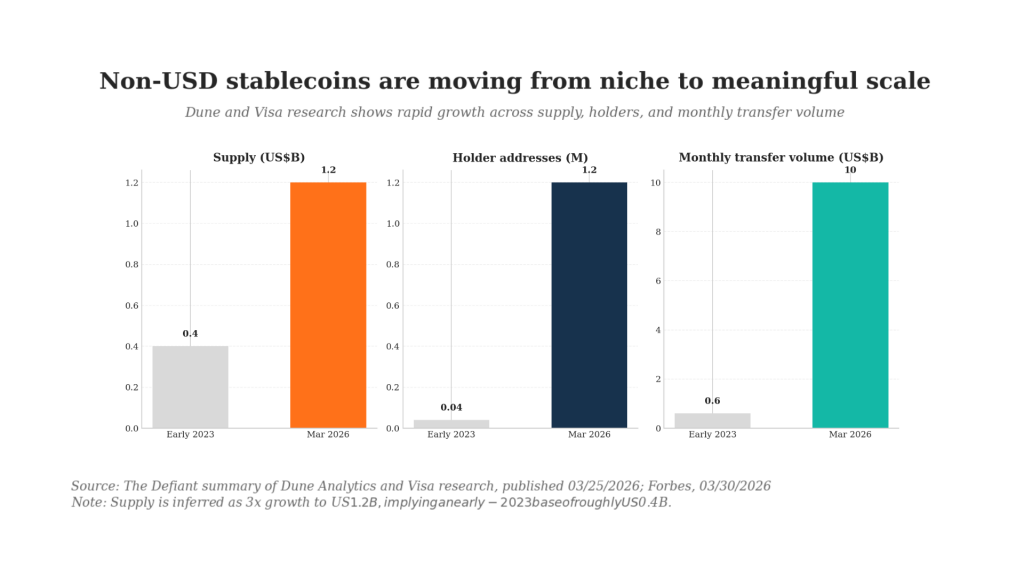

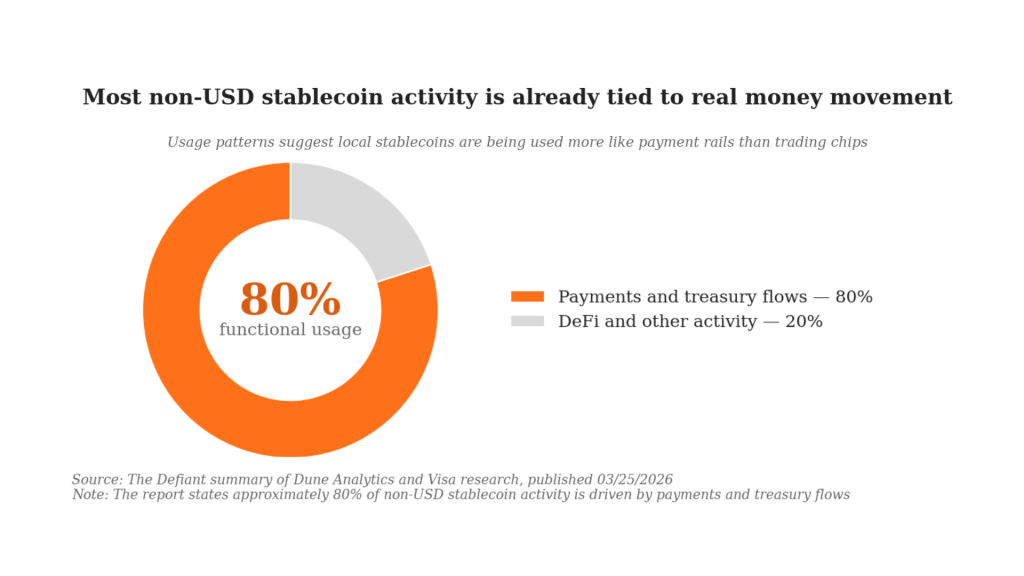

A March 2026 report synthesized by Dune Analytics and Visa, and later covered by Forbes and other outlets, found that non-USD stablecoins had reached roughly US$1.2 billion in supply, with holder addresses rising from about 40,000 to 1.2 million in three years and monthly transfer volume increasing from US$600 million to US$10 billion. Just as important, the activity appears increasingly functional rather than speculative: approximately 80% of non-USD stablecoin activity is tied to payments and treasury flows rather than DeFi. [5] [6]

That does not mean dollar stablecoins are losing relevance. It means the market is beginning to discover something more interesting: money works best when it matches the currency context of the transaction.

A merchant in Singapore still prices in Singapore dollars. A traveler from the region still thinks in local currency. A business settling with suppliers across Asia still has to manage local payouts, FX exposure, compliance, and domestic banking rails. As more commerce moves on-chain, the logic becomes clearer. The real opportunity is not simply putting fiat on-chain. It is putting the right fiat on-chain.

That is where local stablecoins begin to matter.

And that is also where StraitsX (our portfolio company) has been positioning itself for years.

Beyond Dollarization

The easiest way to misunderstand local stablecoins is to treat them as a smaller copy of the USD stablecoin market. They are not.

Dollar stablecoins succeeded first because they solved a global crypto coordination problem. They gave exchanges, traders, market makers, and protocols a shared unit of account. Local stablecoins solve a different problem. They reduce the frictions that appear when digital value has to touch the real economy: payroll, merchant settlement, remittances, treasury operations, domestic payouts, and cross-border commerce where users want local currency outcomes.

That distinction matters more in Southeast Asia than in many other regions. The region is digitally native, highly mobile, and deeply cross-border, but its payment infrastructure is still fragmented across markets, regulatory regimes, and banking systems. In its recent article on tokenization, Insignia Business Review argued that distributed ledger infrastructure is compelling not because it is novel, but because the benefits are no longer theoretical: near-instant settlement, reduced counterparty risk, and improved capital efficiency are becoming practical infrastructure advantages rather than conference-stage promises. [4]

This is the context in which local stablecoins become useful. They are not just crypto assets with different flags attached. They are attempts to build a more programmable version of domestic money for a region where domestic money still matters.

That logic also aligns with an earlier observation from the same Insignia Business Review piece: stablecoins can act like a kind of “Google Translate” for currencies, lowering the dependence on the U.S. dollar as the required intermediary in regional trade and settlement. If that becomes true at scale, the strategic value will sit with the companies that can connect on-chain money to trusted local rails. [4]

The Real Product Is Not the Stablecoin

One of the strongest insights from On Call with Insignia Ventures’ conversation with Luke Boland of Standard Chartered is that users do not wake up wanting to use a stablecoin. They wake up wanting a better payment outcome.

That sounds obvious, but it changes the entire way the category should be evaluated.

When Boland discusses StraitsX, he does not describe it as a token project chasing speculative demand. He describes a company that helped foster Singapore’s local fintech ecosystem, worked closely with regulators, and built the operational and banking trust needed for stablecoin infrastructure to function in the real world. The bank’s role in that relationship is telling: reserve balances, mint-and-burn support, off-ramping, and the resilience required to make fiat rails move “as fast as a stablecoin.” [3]

That is a much better way to think about local stablecoins. The asset is visible. The product is mostly invisible.

The winning company is unlikely to be the one that convinces consumers to care deeply about the token itself. It is more likely to be the company that makes settlement, reconciliation, merchant acceptance, treasury movement, and cross-border value transfer feel dramatically better without forcing the end user to think about what happened under the hood.

In that sense, local stablecoins look less like consumer fintech brands and more like regulated middleware for money movement.

Why StraitsX Is Well Positioned

StraitsX’s recent milestones matter because they show how local stablecoins move from thesis to infrastructure.

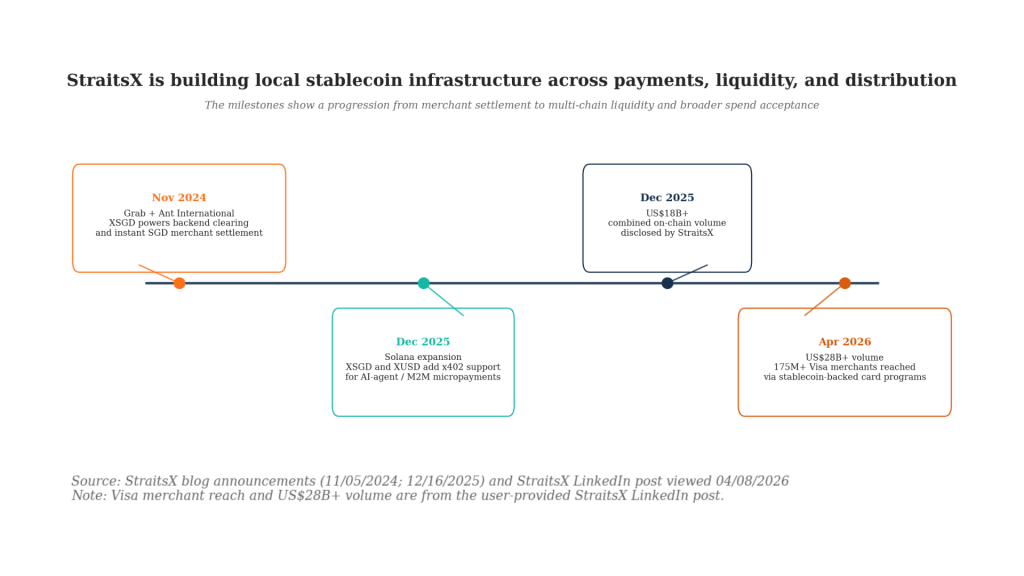

The company has said its stablecoin rails have now processed more than US$28 billion in combined on-chain volume, up from more than US$18 billion previously disclosed in late 2025. That number matters less as a vanity metric than as a signal that the system is being used repeatedly across real flows. [2] [7]

The more important signal is where that usage is showing up.

In November 2024, StraitsX announced a partnership with Grab and Ant International to support cross-border payments for inbound travelers paying GrabPay merchants in Singapore via Alipay+ partner apps. Under the hood, the system uses the Avalanche network, XSGD, and purpose-bound money to handle backend clearing and settlement, while merchants receive instant settlement in Singapore dollars. That is exactly the kind of use case local stablecoins need: not crypto for its own sake, but better local-currency settlement for a transaction that is inherently cross-border. [1]

The structure of that flow is revealing. Consumers pay with familiar wallets. Merchants receive local currency. The stablecoin does the hard work in the middle.

That is what mature infrastructure looks like.

StraitsX has also been pushing distribution outward. Through stablecoin-backed card programs, the company says it is helping extend access to more than 175 million Visa merchants, connecting on-chain balances to everyday spend rather than isolating them inside crypto-native contexts. At the same time, XSGD’s availability on platforms such as Coinbase matters because local stablecoins need liquidity, access, and credible distribution before they can become truly useful at scale. [7]

A local stablecoin without liquidity is just a concept. A local stablecoin with banking rails, exchange access, merchant settlement, and institutional partnerships begins to look like infrastructure.

Singapore’s Advantage Is Not Just Regulation

It is tempting to explain Singapore’s role in this market simply by pointing to regulation. That is part of the story, but not the whole story.

Singapore matters because it combines several things that are rarely found together: legal clarity, a strong payments ecosystem, globally connected financial institutions, and a high concentration of companies building for regional rather than purely domestic use cases. In the Luke Boland conversation, StraitsX is explicitly recognized for the work it has done with MAS and the broader ecosystem to help mature the local stablecoin environment. [3]

That ecosystem effect is easy to underestimate. Local stablecoins do not scale through issuance alone. They scale when regulators, banks, exchanges, merchants, wallet providers, settlement partners, and developers can all work against a common set of expectations around trust, redemption, reserves, compliance, and operating standards.

This is also why Singapore’s role in programmable money initiatives matters. The tokenization article published by Insignia Business Review frames Singapore as a regional precedent for turning experimentation into repeatable infrastructure, especially through efforts such as Project Guardian. Local stablecoins benefit from the same institutional habit: innovation that is forced to become operationally credible. [4]

That environment helps explain why a company like StraitsX can play a much broader role than issuance. It can become the connective layer between local banking systems, digital asset platforms, cross-border merchants, and eventually machine-native payment flows.

Local Stablecoins and the Agentic Economy

The next chapter may be even more interesting than merchant settlement.

A large part of fintech over the last decade improved the user experience layer of finance. Stablecoins are now starting to improve the settlement layer. The next leap may come when software agents, APIs, and machine-driven commerce need money that can move as natively as data.

This is where local stablecoins stop being a niche regional payments story and start looking like part of a much larger internet infrastructure story.

In December 2025, StraitsX announced the launch of both XSGD and XUSD on Solana, explicitly positioning the chain as a high-speed liquidity hub where businesses can swap between the two assets instantly and where the assets can support the x402 interoperability standard for AI agents and machine-to-machine micropayments. The announcement framed XSGD and XUSD as among the first stablecoins designed to support automated agent-to-agent payments natively. [2]

That might sound futuristic, but the logic is straightforward. If internet-native agents are going to pay for compute, APIs, services, or one another’s outputs, then they will need money that is internet-native too. And if those transactions eventually touch real commerce, local currencies will matter there as well.

A machine paying for something in Singapore may still need SGD-denominated settlement.

That is why the local stablecoin story is bigger than regional payments. It is about whether domestic currencies can become programmable building blocks in a financial system where transactions are increasingly executed by software, settled across chains, and embedded inside products rather than routed manually by humans.

What the Market Is Starting to Reward

The recent growth in non-USD stablecoins is still small relative to the broader stablecoin market. But small markets can still be strategically important if they reveal where value will accrue next.

What the Dune and Visa data suggests is that local stablecoins are not expanding mainly because people want more speculative tokens. They are expanding because more users and businesses want currency-aligned digital money for practical workflows: payroll-like cycles, treasury movement, merchant settlement, and cross-border transfers that end in local payout. [5] [6]

That has important implications for how the category should be judged.

The leading local stablecoin companies may not look like the leading crypto companies of the previous cycle. They will probably look more operational, more regulated, and more distribution-heavy. They will need bank partnerships, compliance depth, redemption reliability, exchange access, and enough real-world integrations that the token becomes part of a payment graph rather than an isolated asset.

In other words, the market may reward the companies that can make stablecoins boring in exactly the right way.

That is what makes StraitsX’s position notable. It sits at the intersection of local-currency issuance, regulated payment infrastructure, merchant settlement, institutional partnerships, and emerging machine-native use cases. In a market that is moving from stablecoins as instruments to stablecoins as rails, that is a strong place to be.

The Future of Stablecoins Will Not Be Only Dollar-Shaped

The future of stablecoins is unlikely to be a simple story of non-USD assets overtaking dollar ones. The dollar will remain central for a long time, both on-chain and off.

But the future does look increasingly multi-currency.

As more economic activity moves onto blockchain-based rails, the market will keep rediscovering a basic truth that traditional finance never escaped: value may move globally, but it is still lived locally. Salaries, invoices, merchant settlements, consumer prices, and treasury obligations do not disappear just because the ledger changes.

They still settle somewhere. They still settle in someone’s currency.

That is why local stablecoins matter. Not because they challenge the dollar everywhere, but because they make digital finance usable where the dollar was never the right final answer in the first place.

And if that is the next phase of the market, then the winners will not simply be the issuers with the biggest tokens.

They will be the companies that build the local rails, trust layers, and real payment pathways that let those currencies move on-chain as naturally as money should.

StraitsX is one of the clearest examples of that future already being built with both XSGD and XUSD.

References

[1] StraitsX. “StraitsX, Grab, and Ant International Further Partnership to Simplify Cross-Border Payments.” StraitsX Blog. 11/05/2024. https://www.straitsx.com/blog-post/straitsx-grab-and-ant-international-further-partnership-to-simplify-cross-border-payments

[2] StraitsX. “StraitsX to Launch Both XSGD and XUSD on Solana’s Public Blockchain.” StraitsX Blog. 12/16/2025. https://www.straitsx.com/blog-post/straitsx-to-launch-both-xsgd-and-xusd-on-solanas-public-blockchain

[3] On Call with Insignia Ventures. “The right way to bridge fintechs and banks with Standard Chartered Head of Fintech, Asia Luke Boland.” Insignia Business Review. 03/12/2026. https://review.insignia.vc/2026/03/12/luke-boland-standard-chartered/

[4] Paulo Joquino. “The Tokenization Precedent: How Wall Street’s Infrastructure Evolution Impacts Southeast Asia.” Insignia Business Review. 03/13/2026. https://review.insignia.vc/2026/03/13/tokenization/

[5] DefAInt. “Non-USD stablecoin supply surges 3x in latest research: Dune and Visa.” The Defiant. 03/25/2026. https://thedefiant.io/news/markets/non-usd-stablecoin-growth-dune-visa-research-b6efj2

[6] Boaz Sobrado. “Non-Dollar Stablecoins Hit $1.2 Billion As Currencies Go On-Chain.” Forbes. 03/30/2026. https://www.forbes.com/sites/boazsobrado/2026/03/30/non-dollar-stablecoins-hit-12-billion-as-local-currencies-go-on-chain/

[7] StraitsX. “Non-Dollar Stablecoins Hit $1.2 Billion As Currencies Go On-Chain.” LinkedIn. 04/2026. https://www.linkedin.com/posts/straitsx_non-dollar-stablecoins-hit-12-billion-as-activity-7447146165130903553-zoJi

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.