Across 10 podcast episodes, we’ve had the opportunity to talk to leaders of Fazz at various stages of growth.

There are parallels between their journey and how fintechs in the region have evolved and matured.

They faced challenges shared by many other fintechs at that point in time but also approached these challenges with their own unique approach.

We compiled this recap of the past 10 episodes and learnings from how they tackled the various learning curves for Southeast Asia fintechs:

The Learning Curve to Unlock Distribution for Fintech (2016 to 2019 in Indonesia)

From 2016 to 2019, PayFazz grew its business on top of (to this day) one of the country’s largest agent networks for financial services, primarily enabling consumers in rural Indonesia to make bill payments and bank transfers.

PayFazz’s competitive advantage was not in its application per se, but in the pairing of this application to agents (typically warung / kirana store owners) at scale. It was an online-to-offline platform for financial services to reach populations banks had typically overlooked.

A platform Hendra likened to Google Play in 2020.

“When we started the company, we knew that one of the reasons why there are so many unbanked in this place is because there is no effective distribution channel. So the first step that we do is to find the most effective method to distribute things in rural areas.

According to history, we’ve seen that kirana stores are the most effective tools for consumer goods or telco to distribute their products to this huge rural population, hundreds of millions of people.

And as we see that the kirana store or warung is the most effective one, we try to onboard all of them to our platform and then, as soon as we get the warung on our platform we use them to distribute products, right?

In this case, for example, we provide things like bill payments that is already familiar to the customer. And when the customer interacts a lot with the PayFazz agent to access bill payments, this kind of interaction can be used as a baseline to create a platform…

…Like the people in the city always think that whenever I have to find apps, I will have to go to Google Play. We would like to see PayFazz as the Google Play of financial services for the rural people. So that’s how we evolve from the bill payment agent network to finally become like the go-to agents for every financial service.

To achieve that mission, we have several methods. First, we partner with many financial services providers in the country. We also have [to secure a] license with which we can create customized financial service products that are tailored to this unbanked rural market.”

Listen to the full podcast

The Learning Curve to Build Regulator Confidence in Fintech (2016 to 2019 in Singapore)

While PayFazz was building its agent network and working to secure licenses that would enable them to launch more products on this “Google Play” platform for financial services in rural Indonesia, another company was also grappling with scale and in particular, winning over regulators.

In Singapore, building API solutions for more efficient and cheaper bank transfers in a time before FAST meant having to open up regulators to this new form of distributing financial services. Since launching in 2015/2016, Xfers made it a point to build a strong relationship with regulators and ensure their services were compliant. From an operations standpoint, that meant prioritizing features like verification to handle fraud.

Tianwei shared in March 2022: “So a lot of these things have come a long way in the last five or six years. Hopefully, we were part of the reason that contributed to it. We were pioneering bank transfer-as-a-service; we build APIs around virtual accounts, and we automate people’s ability to send money. And on top of that we have to build of course the compliance layer around the whole solution.

I think we spent a long time…being able to be compliant to local regulators, and handling the fraud that is happening on the ground so that the regulators start to open up. Because they used to have a mentality that these are things that can only be done by the bank. Because the bank can be restricted and controlled and protect the consumer.

But I think Xfers has successfully demonstrated to the regulators for the last five to six years, [that] we can do it just as safely. It’s not better, but at the same time at a faster, lower cost and promoting innovation. So on top of that, you’re seeing a booming of fintechs. Now you have FinTech investment space, the blockchain space, the payments space, whatever they want.

But the basic building blocks of being able to receive payment, send payment and make this whole seamless and low cost, it’s really a great leap forward. I was selling them that pitch that it takes 18 months for any FinTech then, in 2015, to start a company because it takes that long for you to figure out how to build an API and build the basic services.”

Listen to the full podcast

The Learning Curve of Consolidation (2020-2021)

This challenge of securing licenses and developing compliant financial services was the backdrop for these two companies to eventually join forces in 2020/2021 to form Fazz.

Beyond the licenses PayFazz had in Indonesia (e.g., emoney) and Xfers in Singapore (e.g., emoney as well), PayFazz was already using Xfers technology as part of their tech stack to power the transactions being facilitated through their agent network.

Tianwei shared in December 2022: “I think everyone can say that regulators around the region need to be more innovative and Singapore is probably already at a frontier of that. But having spent the last five to six years working with them, I will fundamentally distill down the fact that we have to face the fact that the number one job of regulators is not innovation, it’s financial stability.

So they need to make sure that things are gonna be okay. And that is their primary, most important job. And with that, there needs to be trust. So I think the pandemic made that even more difficult these days. But the fact is you need to have a proven track record of being able to be on the ground, serving the community, and actually doing a good thing before they will even be willing to give you licenses.”

Xfers on the other hand recognized the value of PayFazz’s immense distribution, and how much of a presence the company had built in the fabric of the communities where it was present.

“So across our work for the past five years, we have onboarded almost 200,000 small mom-and-pop stores in Indonesia, which we call warungs. By giving them a mobile application to provide over-the-counter financial products and services such as bank transfers, paying water bills, electric bills, and telco bills to their neighbors.

So a lot of these customers are actually their neighbors who walk up to them to buy a cigarette, FMCG product, or mineral water, and then they will also ask for financial services.

And through them, they become an agent of change. A lot of our customers get access to e-commerce for the first time through these agents, because they have no way to make payments for Tokopedia or Bukalapak.

You also realize if you just spend some time near the agent, the Gojek drivers who we say are a huge part of the change that we received the last five years, you just observe where they are actually getting their Gojek credit top-up, and where they are having their coffee is again around these small mom-and-pop stores. They’re the heart of the economy over there.

These are their neighbors. These are where they have a very comfortable time during their downtime sitting under a large tree enjoying a sate tai chan and just chatting with their friend. And that’s where they get most of the services that they get today.”

Crucially, both founders envisioned building regional companies, and consolidation provided an avenue to do that when their work was already quite entwined.

“So that was the backdrop that we were even discussing in 2019. Hendra and I were saying that we are both trying to expand the business. I’m looking to go into Indonesia; they are expanding out. But a problem is gonna happen where if you’re not local enough, we don’t have enough presence, acquiring licenses is extremely difficult to navigate.

So we saw a lot of synergies already with the fact that our businesses have so much overlap and we need each other to expand a lot. So that became one of the key drivers for why we decided to come together as a company. Because together we can achieve a lot more and licenses will allow us to basically have a [wider] reach and give more services to our existing clients.”

Listen to the full podcast

The Learning Curve of Building Competitive Moats Amidst Fintech Rebundling (2020-2021)

One of the benefits of the formation of Fazz was that it allowed the now regional fintech group to test out and develop expansion both horizontally and vertically.

This became more important as competition began to heat up for fintech around “rebundling the bank”, expanding vertically to develop their own banking stack, reduce revenue dependencies on go-to-market products like payments and e-wallets, and increase the “customer basket/wallet.” This came at a time when digital banks were entering the market in full force, presenting yet another class of competition for fintechs.

The race to “rebundle the bank” created more permutations for winners in the market, especially if verticalization revolved around a target market where the company has unique, defensible distribution.

As Hendra shared in April 2021: “So that’s what I foresee in the future, that the guys who have a laser focus on one field and have a very localized approach, especially in the rural areas, [will win]. You may be in the same country, Indonesia, but rural Indonesia will have its own localization. So that rural localization and that laser focus on fintech, especially for the unbanked, I think is our key to be able to defend in our David versus Goliath scenario that we always face.

And what I foresee in the next five years is that the evolution of the Indonesian fintech landscape will shift away from purely payment and e-money playbook into a full banking stack where people will start to offer you, instead of just payment with QR, a full banking stack where people are going to start to use this more than just for payment.

They’re going to start using it for other use cases, such as investing, lending, or also buying houses with installment, et cetera. And I think this evolution is unavoidable. And a lot of fintech in the region will need to adapt to stay relevant.”

Listen to the full podcast

The Learning Curve of Building in Crisis and Opportunity (2020-2021)

Apart from the challenges of increasing competition and pursuing regionalization, the years 2020 to 2021 also saw fintechs grappling with fluctuating market conditions around private funding, from the crunch into 2020 to a sudden boom in 2021.

For Fazz, the formation of the fintech group diversified risk for all the businesses part of the group. But at the same time, the increasing size and complexity of the organization presented new challenges in orchestrating agility and moving goalposts.

As Hendra shared in 2023: “That move to expand has proven that not only can we build a profitable business with a good product and good unit economics, but we also can expand to other countries under the crisis. And that’s been proven to be successful. So now our vision has scaled up from just changing the way an underbanked small business in Indonesia runs their financial operation to also including countries like Singapore where more sophisticated businesses like crypto businesses exist.

…Our [mission] at the end of the day back then was not to build another bank for them, but it’s really to revolutionize the way these businesses are doing their business. We started with a very simple product and then it’s grown [from there]. And then as we saw that as Covid [came in] 2020, we were forced to think about how to become profitable. We quickly turned the company to be profitable in 2020 and then after that in 2021, we saw that the market was going back very crazily. Every company is raising rounds. And then we discussed with Insignia that we need to be more aggressive again and we quickly converted again from profitable mode to aggressive mode.”

Listen to the full podcast

The Learning Curve of Reprioritization / Returning to the Core Business (2022)

As Fazz experimented with new products and business lines, the company continued to see growth around its payments business, as an infrastructure that exists for multiple use cases, from consumer payments to merchant payments to crypto payments.

Defining this core business became important in 2022 as the fundraising bubble popped and companies were forced to prioritize.

As Zack Yap, Head of Payments at StraitsX, shared in 2022: “I have to echo what Hendoko just mentioned that also points to something about our growth in the future to the rest of Southeast Asia, that the core business needs of these businesses when they’re doing their financial operations revolves a lot around receiving payments, making payments, and this is exactly what we are focused on and this is also our strength, making sure that we focus entirely giving them a 10x experience in terms of how they receive money, how they’re gonna be making payments, how can they grow their business, by providing them credit at the right basis.”

Listen to the full podcast

The Learning Curve of Staying the Course (2023)

Eventually by 2023, Fazz was evolving into having two key pillars driving its growth: its agents business in Indonesia (Fazz Agen) and its blockchain business in Singapore (StraitsX).

The latter saw a milestone later that year, where StraitsX’s issued XSGD and XUSD became part of a new license regime being developed by the MAS as of this writing, a significant step forward in driving mainstream, compliant adoption of stablecoins as digital assets.

It was not an easy road for StraitsX, even before the business became part of the Fazz. The hype cycles around crypto and widespread fraud in the industry also did not help. But the company remained steadfast in its mission, continuing to work with regulators and industry partners (see Project Orchid and Project Lighthouse) to develop meaningful use cases for these digital assets, which using stablecoins can actually help merchants settle transactions faster and at a lower cost.

As Tianwei shared earlier this year: “It’s almost four or five years since we launched XSGD, and close to 8 billion XSGD has been transacted on-chain…These are real transactions that people have started using…it gives us the confidence that this is going to be a regulated industry. This is going to be something that’s the right step in the direction as a payment infrastructure for this part of the world…and beyond the Singapore dollars, the licenses also mean to say…we are now able to issue G10 currency stablecoins out of Singapore with this new license regime and XUSD, which is what we’re gonna be focusing our effort on in the coming years…

…There’s so many things you can do, but in [a certain] order…it must be first, be able to increase the acceptance and make sure that it’s as seamless as possible without drop off rate. Then you go into costs. Can I make sure my cost is as low as possible, especially for cross border…Then the innovation, which is free game for a lot of guys to come in.”

Watch the full podcast

The Learning Curve on Translating Regulatory Innovation into Meaningful Growth (2023)

While Fazz was able to secure key licenses through its journey to roll out various financial services, simply having the license does not equal growth or market leadership.

There needs to be alignment with the organization as well as the product quality itself to justify the stamp of approval being given by the regulators.

As Tianwei shared earlier this year: “…“move fast and break things” does not apply here. In payments and fintech, you can’t break things. If things go wrong…someone’s going to get really hurt…you do really need to be patient. There are certain things that we know what the goal is, but you need to know that you can’t do this overnight. You actually have to set the culture to do things right the first time and consider the impact on the customers and on people…”

Regulation opens doors to previously inaccessible market segments (e.g., FIs and banks) but the product makes the first step.

…“It’s not something that can be done overnight, but getting these licenses and compliance helps to give you a stamp of approval. It is not enough, but it’s definitely more helpful to at least help education move along. It also means that institutions are able then to adopt this blockchain technology…Having a regulation compliance on a FinTech side, from a competitive advantage side of this, means that you can then serve a wider customer that traditionally would either be fearful or unable to reach”…

Time and place matter when it comes to regulation. There are also blue oceans / market gaps as well when it comes to regulation and this factors into the growth potential of the business.

…“Singapore is in a perfect position to do it, because of the regulation regime where you probably would think about China and other jurisdictions being geopolitically sensitive as well…there’s a huge opportunity in being able to be a regulated stablecoin issuer in Singapore. But potentially, this means for the whole entire region there will be a lot more adoption given that now Singapore has set the bar down. We have seen this happen before.”

Watch the full podcast

The Learning Curve of Horizontal Expansion (2024)

As Fazz has continued to grow and mature going into 2024, the key question remains of how the company will expand with the capabilities and scale it has achieved.

To even be in a good position to ask this question, it was necessary to professionalize Fazz as an organization.

Mark Hew shared how his first few years in the company were spent transitioning “from a startup into a professional organization, focusing on systems, processes, and cadence.”

Today, Fazz is well into what Mark calls the “consolidation phase.” Fazz has started to “consciously align different parts of the organization, identifying core strengths and creating a competitive advantage moving forward.”

The competitive advantage moving forward has been increasingly defined around payment infrastructure. “Our infrastructure actually serves some of the big names in Indonesia, like Blibli, Brick, Bukalapak, and Flip.”

Fazz’s core has always been in payments. Looking ahead into what Mark calls the company’s “expansion phase”, Fazz is looking to expand their services into “as many customer segments as possible.”

“For instance, a company from China or the U.S. wanting to enter Southeast Asia could partner with us, and we would provide them access to the entire region. This horizontal expansion also includes the Web3 world. You get access not only to fiat transactions but also to the Web3 world, which transcends national boundaries.”

Watch the full podcast

The Learning Curve of Keeping the Startup Spirit Alive at Scale (2024)

Even as Fazz continues to evolve across these phases of growth, there are key pillars of the company’s identity that have to remain the same — that it is envisioned to be a regional company; that it has a founding history rooted in rural Indonesia; that it was built by leaders with an underdog mindset.

As Mark quotes Hendra: “We are building a regional company, not just an Indonesian one.” As much as Payfazz has its roots in rural Indonesia, and Indonesian culture will always be part of its DNA, the scope it has achieved has to match with how the company operates, down to even how meetings are run. “Our vision is to compete with international companies, so we need to operate like one.”

“Bring them back to where it started.” It’s important to balance out the future with the past in onboarding employees into the company. Employees in Fazz’s agent business have warung visits as part of their onboarding journey.

“During onboarding, we remind new employees why digital transactions for the unbanked and underbanked population are so important. Constant reminders of the company’s founding origins help inculcate this behavior in everything we do.”

Learn more about the SOS culture at Fazz

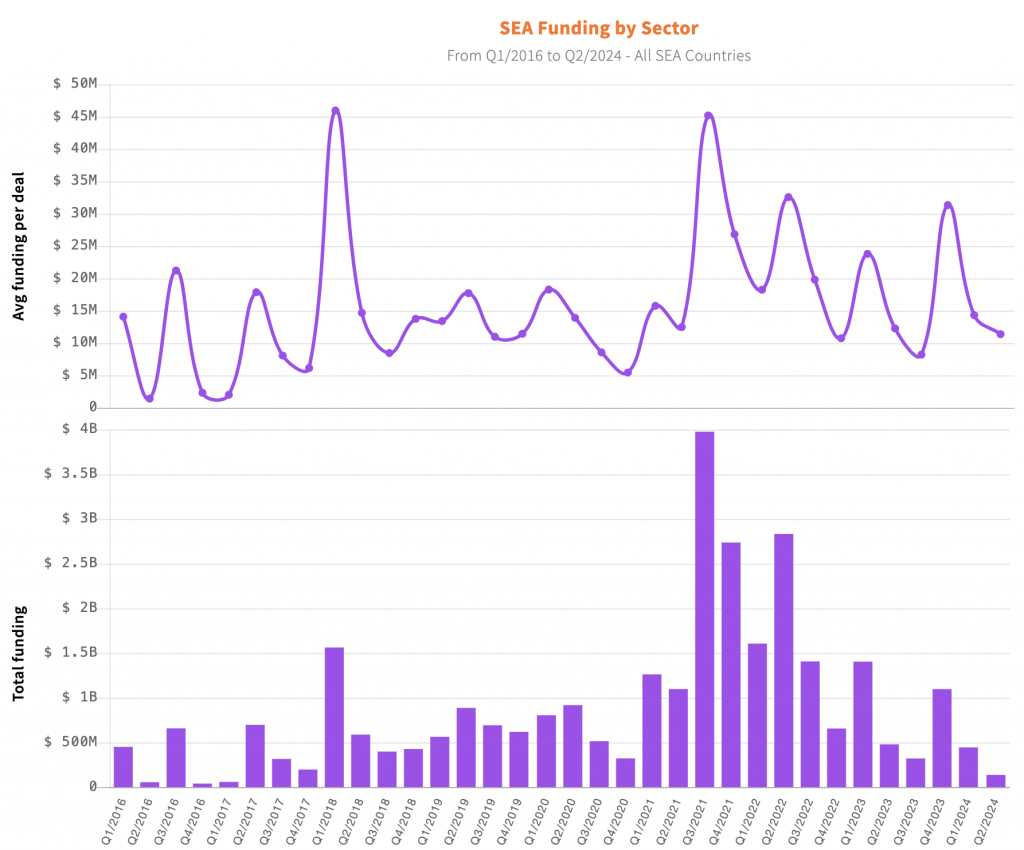

Fintech funding in Southeast Asia, all stages, all markets, from 2016 to Q2 2024

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.