The rise of fully digital banks (no physical branches and licensed) in Southeast Asia is an interesting case of how the forces of competition both birthed and today challenge the digital bank approach.

A rebundling of digital financial services created a race among fintechs (and some well-resourced non fintechs) to build up the digital banking stack through product development, partnerships, acquisitions, and licenses, revolving around a core product or acquisition driver (e.g., marketplace, lending, payments, credit cards, etc.).

Other fintechs took the “fully digital bank from day one” approach, building from the ground up through savings accounts (still an acquisition driver / go-to-market) with the aim of leveraging the cash supply to launch lending products.

At the same time, the open finance tech stack that enabled digital banks to operate within the existing banking industry and the emerging fintech ecosystem also created a new wave of non-fintechs integrating financial services into their customer journeys.

The emergence of fully digital banks in Southeast Asia also attracted other players in Asia to try their hand at expanding in the region by partnering with local banks (e.g., WeLab Indonesia).

The traditional banks also didn’t sit around as all this happened. As mentioned, they partnered with / got acquired by digital banks abroad looking to land in Southeast Asia or local fintech players for the latter to become digital banks, or kicked off digital transformation internally, launching their own digital apps and branchless customer journeys.

These three layers of competition rapidly emerged as the majority of the fully digital banks in Southeast Asia were licensed and launched from 2020 to 2022.

Throw in the challenges of a tight fundraising market, relatively high interest rates from central banks, and the pressure to prove profitability (a notably rare case for digital banks globally, around 5%), and you have the best parts of the region’s digital banking story yet to be told.

The good news is that the ecosystem of enablers around digital banks is becoming more sophisticated, along with the emergence of opportunities to tap into generative AI to deliver efficiencies on lending customer journeys.

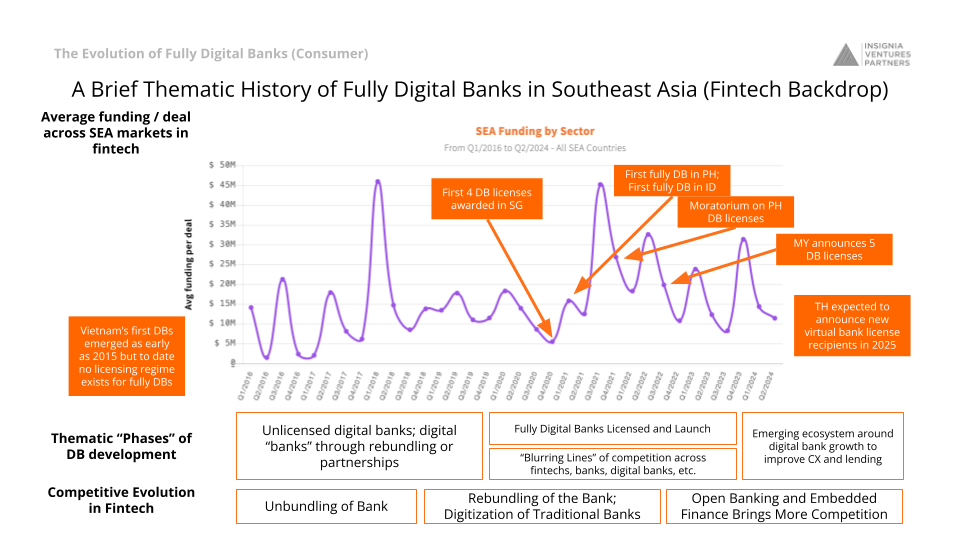

While regulatory regimes and licenses emerged and were updated for most Southeast Asia markets in the 2020 to 2022 period, these licenses and regimes are not equal and have nuances unique to the nature of each market.

For example, while Singapore and Philippines issued fully digital banking licenses (the Philippines later issued a moratorium), Indonesia did not issue dedicated licenses and only updated its regulation on conventional banks. In addition to digital bank licenses, Malaysia also released Syariah-compliant digital bank licenses.

Meanwhile, Vietnam digital banks emerged through partnerships due to the lack of a licensing regime, while Thailand only recently opened up applications for its new virtual bank license, with an aim to announce the awardees in 2025 and launch in 2026.

We’ve captured this industry’s development in the last five years through a variety of essays. We’ve divided up this development into phases and curated the best parts across the years.

A Brief Thematic History of Fully Digital Banks in Southeast Asia (Fintech Backdrop)

Years leading up to 2019: The unbanked / underbanked narrative drives the unbundling of the bank as fintechs figure out distribution

Essay 1: How Digital Disruptors Serve The Unbanked In Southeast Asia (January 2019), also published on Forbes

“Banking penetration remains low in the region, with only 47% of the population in Southeast Asia having a bank account despite these new initiatives. This gap is highlighted particularly in the Philippines, where a staggering 77% of the population is unbanked, according to a recent survey by the Bangko Sentral ng Pilipinas.

A similar magnitude of people are afflicted with the same problem in Vietnam and Indonesia at rates of 65% and 52% respectively. With this in mind, how can the unbanked be better served in the region?

“The supply of the banks can’t accommodate the burgeoning number of users. It’s the equivalent of being in Union Square in downtown San Francisco. The people in Mountain View and Oakland would find it difficult to get there,” said Hendra Kwik, CEO of Payfazz, an Indonesia-based mobile platform for financial services, in reference to the banking ecosystem in Indonesia.

As most Indonesians store their money as cash, a tech-only approach to banking the population does not suffice. A physical presence is required to digitize the cash for consumers, and Payfazz hopes to provide a solution with its army of offline agents…”

Read the full article

Essay 2: Scaling Fintechs In ASEAN (November 2019), from an interview for the 2019 Fintech in ASEAN report

“Scaling a fintech company across Southeast Asia means constant innovation. If the fintech is a payment gateway, how can they grow from that? If the platform initially aggregated insurance options, how else can users better get insurance? What kind of financial services will be available to users in the next five years?

Founders need to keep asking themselves how much better their product or platform can be for their users. When it comes to the direction of this innovation, access to data, available technologies, and market environments (regulation, partners) chart out the path to take, but founders should be unstoppable regardless.”

Read the full article

2019 – 2020: Pressure to increase monetization, drive retention, and take on competition drives rebundling of the bank as well as the rise of the fully digital bank (platform-first approach)

Essay 3: Platform-First: Fintech’s Next Destination (March 2020)

“As with the unbundling approach, the ongoing rebundling efforts of most consumer-focused fintech startups also has its limits. Taking the example of lending startups, which have been prone to jump on the rebundling bandwagon globally, they have had to rely on (expensive) external sources of funding originated from traditional banks, multi-finance companies, credit hedge funds, etc., constraining their margins, especially as compared to banking incumbents. Going to other ancillary services does not solve their fundamental unit economics problem even if it (theoretically) increases their customer LTV.

On the consumer side, while access to credit is a key painpoint for subprime clients in both developed and developing markets, fintech players despite their rebundling efforts have not yet been able to displace traditional banks to access the consumer fintech “holy grail”: checking accounts constraining their ability to finance themselves at lower costs and cross-sell.

In order to break away from these limits, some fintech players are choosing to become fully-fledged banks. In the US, Lending Club acquired Radius Bank, a FDIC-regulated, retail deposit-taking bank, last month. Varo, a digital bank that was relying on 3rd party licensed community banks to acquire depositors, also announced that it became the first fintech in the US to obtain a retail bank charter. In both cases, a cheaper and more stable access to capital as well as the ability to cross-sell and innovate without relying on partners were cited as key decision factors.

The past decade also saw fintechs going platform-first, redefining the bank as a store of value. Starting with checking accounts or better yet market-leading savings accounts, neobanks licensed to take retail deposits such as N26, Chime, NuBank, and Monzo catered to different segments of the population from mass-affluent travelers (Revolut/Niyo) to SMEs (Atom/Qonto).

This platform-first approach generates better unit economics than the single-product approach by drastically reducing cost of capital. It also created enough margin to release products covering liabilities aside from pure asset-focused products, catering to a wider range of customer needs…

…In Southeast Asia, Tonik Bank is the first to embrace this platform-first approach. Based in the Philippines as the first stand-alone, fully-licensed neobank in the country, the bank will cater to retail consumers across the entire credit spectrum from prime to unbanked segments of the population.

While there has been a lot of coverage recently on Singapore’s efforts to open up the local retail and wholesale banking market to new players, the Philippines was the first country to pull the trigger on the neobank model given how much pent-up demand exists locally.

There are indeed close to a million mass-affluent households in the country frustrated by their experience with brick-and-mortar local banks (e.g. slow and analog processing, high fees). More importantly, close to 20 million households are currently underbanked or unbanked. For the latter, the frustration over the years manifests in their unsustainable financial situation. Many of them turn to local loan sharks and pawn shops as their only sources of access to credit. TONIK will be offering both segments of the population a clearly differentiated proposition on both financing and deposit products.”

Read the full article

Essay 4: SFFxSWITCH 2020: Fintechs At The Forefront Of Investment Into ASEANnovation (December 2020)

Based on insights from an Investor Summit Panel “Spotlight on ASEAN: Investment Priorities”, with SBI Investment Executive Officer for Overseas Investment Tomoyuki Nii, Sixteenth Street Capital founder Rashmi Kwatra, Beenext Managing Partner Dirk Van Quaquabeke, Qualgro Partners founding managing partner Heang Chhor, and Insignia Ventures Partner founding managing partner Yinglan Tan. The panel was moderated by EY Global Emerging Markets Fintech Leader Varun Mittal and Expand Research Managing Director and Head of Asia Pauline Theobald Wray.

“In the next ten years, the digitization of financial services, in particular, will be at the forefront of ASEANnovation. We’ve already seen this year marked by the movement of tech unicorns and giants into the fintech space through payments (GrabPay, GoPay, ShopeePay) and banking licenses. Consumers are looking for more “complete” customer journeys on their fintech apps and the digitization of businesses along supply chains means more data to power B2B financial transactions.

For Yinglan, the immense opportunity for fintechs has also been met with risk. “The first wave of fintechs were unbundling the bank, but then they realized there are regulatory requirements and high acquisition costs, and difficulty in retaining customers.”

But then this risk for the first wave of fintechs is also now being overcome with new fintech models. “…now we’re seeing the second wave, which is the rebundling of the banks, we see it in tonik in the Philippines, and Flip and Fazz’s Fazz Agen in Indonesia.”

Read the full article

2021: Digital Banks Take Off with Deposits Amidst Digital Adoption Hype Driving Verticalization (More Competition)

Essay 5: 7 ASEAN Fintech Trends In 2021 (January 2021)

“The rebundling of banking services and creation of digital banks from scratch among fintechs is something we’ve written and talked about so many times over this past year, and for good reason. This rebundling trend aligns with the greater spotlight on digital banks, with regulators in at least three countries in the region (Singapore, Malaysia, Philippines) offering licenses.

While there are players who are non-endemic to the fintech space, Tonik, for example, has been building its proposition from the ground up — that is to say, it is a purely digital bank.

Moving into 2021, we will see how the winners of the license race will now work to build and launch their services to the masses. From the regulators point-of-view, it will also be interesting to see how they will engage with these existing contenders and entertain new entrants in the future.

While this evolution in fintech business models has been ongoing even before COVID19, the crisis has only accelerated adoption of fintech apps, and this consumer shift has opened doors for fintechs to expand their services even faster…

…We will see more downstream consolidation in consumer-facing fintech services, especially as local tech companies expand into fintech and traditional players try to participate more actively in the space. At the same time, this opens up room for players to evolve their business models, either to compete with or enable these consolidating forces. The digital banking races across the region is more of the former, where tech companies will compete in their propositions to consumers.

This shift into fintech is the next step for these consumer platforms that are making the super-app play and looking to capture the entire customer experience of their already massive user base. Investments into the region’s tech sector will slant heavily towards fintech lines of business in the next few years.”

Read the full article

2022: Pressure to Prove Platform-First Thesis Amidst Blurring Lines Across Fintechs, Non-Fintechs, Banks (More Competition)

Essay 6: 5 Learnings From A Front Row View Of The Philippines’ Digital Banking Future In The Making (March 2022)

“On our podcast back in mid-2020, Tonik CEO and founder Greg talked about his go-to-market strategy for digital banking in the Philippines, “For me, the most interesting business model is actually an asset-liability model. True monetization for a bank is through loans. And I think the emerging markets opportunity is very, very compelling.” He cites the example of Brazil’s Nubank, which recently went public in December 2021 in one of the largest IPOs of the year.

Although at different points in their growth trajectory, what Nubank and Tonik have in common is that their digital banking proposition revolves around consumer loans. This stands in contrast to the current account proposition which has been predominant among neobanks in Europe. For emerging markets like the Philippines where accessing equitable loans are a real pain point, there is massive middle-class consumer demand coupled with increasing GDP/capita.

This creates both the supply and demand side of the banking proposition, with supply fuelled by savings and demand fuelled by needs for loans. As the transaction behavior of the Philippines becomes more increasingly fast-paced and ecommerce-driven, the demand for consumer loans only strengthens — already in Southeast Asia we’ve seen the emergence of buy-now-pay-later (BNPL) startups — and there is an opportunity here for more fair, accessible, and short-term solutions.

Tonik’s success with accumulating the supply side of the consumer loan proposition means that it is now a matter of meeting the already existing demand for consumer loans with the digital user experience and targeted offerings for their users.

A good beginning is half the journey, the adage goes, and Tonik has certainly had a good beginning, but there are a lot more needs to be met and opportunities to be tapped into beyond securing consumer deposits and driving adoption of fully digital savings accounts.

All this will be happening in the backdrop of significant developments in the Philippines’ financial services landscape: increasing crypto adoption beyond investing and trading, greater open finance adoption among banks and non-fintech platforms (i.e. every company is a fintech company the saying goes) driven by API platforms, and SME digital banking platforms making headway as SMEs begin to recognize the value of digitalization.”

Read the full article

Essay 7: Deposits, Licenses, And Investments: What Southeast Asia Fintechs Are Banking On For Growth (April 2022)

“Emerging markets in Southeast Asia (apart from Singapore) have long been characterized by having largely unbanked and underbanked populations with little to no access to credit or affordable financing.

This has made lending a popular service in the region for fintechs, and we’ve seen this evolve from pure P2P lending and microfinance to BNPL as the sources of data to build up underwriting capabilities and credit scoring has expanded over time. But the main challenge for P2P lenders or digital lending-only platforms in general is scalable liabilities.

As shared on Tech in Asia: “[Online lenders] are dependent on external funding to fuel their lending propositions…As P2P lenders start out, it may not be as much of an issue. But in order to continue sustainably expanding their offerings, greater weight is placed on ensuring that the funding does come in to fuel the loans.”

On the other hand, for fully digital banking propositions, they have the ability to leverage deposits as fuel. In the Philippines, Tonik is doing this to great effect having gathered a record amount of this “fuel” (US$50 million in 3 months after launch and more than US$130 million in February 2022) which they then have been able to use for their consumer loan offerings.

As Tonik CEO and founder Greg Krasnov illustrates the significance of this fuel the lending proposition on our podcast, “The digital lending guys, it’s so great that they’re doing it, and there are some guys that are bringing some really good know-how, but they don’t have scalable liabilities…

…They’re borrowing from banks, for example credit lines of US$1 million or US$2 million here and there. And that’s just not gonna feed the fire…if you don’t have access to a big amount of funding, you’re going to be marginalized. That for us is a very exciting opportunity.” It’s worth noting that prior to Tonik, Greg was trying to drive adoption for lending in the Philippines but found it challenging partly for this reason.

Economics 101 also tells us that with enough supply, prices can be adjusted down, and in the same way, with a more sustainable and scalable flow on the deposit side, digital banks could in theory offer more competitive interest rates than funding-dependent lenders.

As shared on Tech in Asia: “With a more sustainable and scalable flow on the deposit side, digibanks could theoretically offer more competitive interest rates than funding-dependent lenders.”…

…What’s been interesting to see emerge in the sector across Southeast Asia are digital banking players coming from different angles or core propositions, carrying with them unique moats, and building out their digital banking proposition through various methods. Again this is because of the differences in regulation, competitive landscapes, and fintech core services across markets.

Ajaib for example is building out its banking stack coming from their strength in the retail investment segment and through key investments and acquisitions to acquire key licenses (e.g. they made their foray into stock brokerages through an acquisition).

On the other hand, there’s Fazz, which has been building their banking stack coming from their strength in rural Indonesia and payments. Then at the beginning of the article we talked about Tonik’s approach already solving the single-serve lending proposition challenges from day one with a deposit-fuelled full digital banking proposition in the Philippines…

…Indonesia’s digital banking space in particular, as with many sectors in this massive market, is not a winner-takes-all competitive landscape, but more likely an environment where “winners-takes-what-they-are-good-at.”

As shared on Tech in Asia: “Indonesia’s digital banking space is not a “winner-takes-all” competition, but more likely an environment where “winners take what they are good at…“It is highly possible that as the market evolves, you’ll have these “kingdoms” of market leaders where individual Indonesians have accounts in more than one of these players.””

Read the full article

Essay 8: Making Sense Of The Blurring Lines In Digital Banking: Finovate Edge Asia Panel (June 2022)

Insights from the Finovate Edge: Asia event on 13 July 2022, when our founding managing partner Yinglan Tan joined Asian banking leaders WeLab Group COO Ernest Leung and Kota Mahindra Bank Chief Digital Officer Deepak Sharma on a panel on “The Rise and Fall of Asia’s Digital Banks”, moderated by FinTech Futures reporter Shruti Khairnar.

Regardless of the trajectory, Yinglan adds that there are three important criteria for digital banks: (1) underbanked or underserved population, (2) a good profit pool (proven by incumbent banks), and (3) weak / legacy incumbents (referring to technology). He shares that in the Philippines, these criteria existed and provided the fertile ground for Tonik to rapidly grow its user base and deposits in its pioneering fully digital bank…

…Fully digital banks have the ability to move faster and deliver more catered services, with digital-first understanding (i.e. data) of the customers. This means digital banks are ideally able to reach that holy grail of personalizing offerings to a “segment of one,” in a significantly shorter period of time than traditional banks.

For WeLab, spotting the market opportunity for a digital-only banking proposition in Hong Kong put them ahead of the game today, but the lines are blurring, as Ernest adds, “The big boys have their own digital initiatives or are spinning off. As one of the first movers, we have an advantage of being ahead, however, the lines between a digital-only bank and [a bank becoming digital] are blurring.”…

…Because digital banking services are now operating on the same platform as many other apps (which may also have banking services embedded), then framing customers as “account holders” may no longer be good enough to compete.

For Yinglan, “the competition [of incumbents] is not the banks down the road but the fintechs.” When it comes to digital evolution and transformation, banks need to think like tech companies. Emphasizing the previous point, it’s all about “providing services that customers are comfortable paying for.”

This means framing customers as “daily active users,” and think about how the digital banking proposition is continually able to be a part of the customer’s regular transactions.

“If you’re just trying to move the bank teller to an app, I don’t think there’s much value there,” Yinglan adds, “whereas if you’re combining services…” and he cites the examples of Indonesian fintech unicorn Ajaib, which he describes as a globally unique case of having a bank, a stock brokerage license, and a crypto license.

Essentially it’s an evolution of existing billion-dollar tech companies (i.e. Robinhood, Chime, Coinbase), where users in Ajaib can deposit in their accounts, buy shares of their preferred stock, then diversify with crypto holdings as well.”

Read the full article

Essay 9: Fintech Is Everywhere Part 2: 5 More Trends On The Adoption And Democratization Of Digital Finance (December 2022)

“(1) Platforms with consumer lending products are seeking more secure shores to weather the inflationary environment. Now there are several considerations here: (1) the sensitivity of target customers to inflation, (2) the sustainability of the platform’s liabilities, and (3) the existing credit system to cover these customers vis-a-vis the unsecured loan market (that most fintechs have been looking to tap in these emerging markets). In general, however, asset managers are looking to shift safer disbursement/deployment/underwriting strategies.

For example, Philippine digital banking platform Tonik, while initially looking to lend unsecured consumer loans to what CEO Greg calls the “blue ocean rising middle class”, has since developed offerings into safer segments and assets.

This decision was made in the context of the factors we discussed above: (1) the blue ocean rising middle class working in sectors like retail and F&B that would be the first to be impacted in an inflationary environment, (2) Tonik had accumulated a significant amount of deposits on the asset side, and (3) the underwriting capabilities needed to compensate for the lack of a credit system in the Philippines for their target customers needs time to iterate and fully develop.

And so Tonik has adapted. As he explains on our latest podcast episode, “So we launched actually the first digital mortgage product in the Philippines. And that’s a larger ticket, and a safer product because it’s secured. We are repositioning our cash loan, we’re spinning out a cash loan into the prime segment, a more kind of banked personal loan segment because I fully expect banks to pull back on personal loans.”

(4) One direction fintechs have been taking to expand their product offerings has been building up the banking stack. This has been something we have been writing about since 2019. Building out the banking stack is becoming a predominant path to scale for many fintechs but there are many ways to go about it depending on the availability of licenses, the competitive landscape, and the fintech’s core service / product-market fit.

What we have seen since 2019 is the variety of methods fintechs have been building these stacks: fintech M&A (Fazz forming from M&A of Payfazz and Xfers), investments into and acquisitions of banks and FIs by fintechs (Ajaib acquiring Primasia Sekuritas in 2020 and investing into Bank Bumi Arta), and day-one digital banks (Tonik).

Zooming into the fintech M&As approach, Fazz had been acquiring key licenses to launch in-house services ranging from payments to loans and money transfer as well as investing in startups with adjacent services like Xfers with their banking infrastructure (which ultimately led to the formation of Fazz Financial from Payfazz), Modal Rakyat with their P2P lending platform, and CrediBook with their digital bookkeeping app.

Tianwei shares on our latest podcast episode, “Hendra and I were saying that we are both trying to expand the business. I’m looking to go into Indonesia; they were expanding out. But a problem is gonna happen where if you’re not local enough, we don’t have enough presence, and acquiring licenses is extremely difficult to navigate…

…So we saw a lot of synergies already with the fact that our businesses have so much overlap and we need each other to expand a lot. So that became one of the key drivers for why we decided to come together as a company. Because together we can achieve a lot more and licenses will allow us to basically have a [wider] reach and give more services to our existing clients.”

These methods have emerged given (1) the challenges of securing licenses across markets (it’s already difficult to secure one license in one’s home market, what more in others), (2) the challenges of competing with established banking players and financial institutions which have increasingly been venturing into digital, and (3) the challenges of building competitive moats with differing infrastructure and social behaviors around financial services in different Southeast Asia markets.

Different seeds and growth trajectories but there is such as thing as “fertile ground” in digital banking: (1) underbanked or underserved population, (2) a good profit pool (proven by incumbent banks), and (3) weak / legacy incumbents (referring to technology).

As lines blur between traditional and digital banks, and even beyond banks with open finance and more channels to develop and deliver financial services, the competitive landscape boils down to which players are able to serve their customers’ needs the best and retain them in the long-term. This customer focus means reframing customers from account holders (how to get customers to open and keep accounts) to DAUs (how to provide value-adding services), and this approach is producing mutant, segment-specific banking models.”

Read the full article

2023: Digital Bank Infrastructure and Customer Experiences Evolve with Open Finance and AI Amidst Pressures on Business Model and Profitability

Essay 10: Insignia AI Notes #12: Where Fintech 2.0 Meets AI 2.0 (September 2023)

“The era of smartphone banking is giving way to agent-driven banking, focusing on a full customer experience rather than mere support. Tonik CEO Greg Krasnov talks on our podcast how he envisions a future where natural language dialogues replace cumbersome in-app forms. “It’s going to be by pushing the microphone button and saying, ‘Hey, dude, I need a loan. 5,000 bucks. What do I do?’ And then the app talks back and walks you through the filling out of the application fields,” he said.”

Read the full article

Essay 11: Startups Impacted By The Rise Of Embedded Finance (October 2023)

“In Southeast Asia alone, fintechs facilitate over US$320B in transaction value (digital payments, digital capital raising, neobanking) and generate over US$6B in revenue. This aligns with Indonesia seeing fintech growth going from 51 in 2011 to 334 in 2022. Even amidst the funding winter in 2022, VC investments in Singapore fintech startups reached a peak of US$2.31 billion, up 13% from a year ago.

Over the past decade in Southeast Asia, fintechs were developed in response to specific needs, especially around payments (from the customer POV) and monetization (from the fintech’s POV). This eventually expanded to what is called the “unbundling of the bank”.

While this grew the fintech industry in the region, fintechs have remained largely fragmented across markets, applications, and customer journeys. These products have also largely been standalone or plugged into other platforms separately.

But in recent years, there have been two key developments shifting the way fintechs are being built and approaching growth.

First is the emergence of open finance and API/infrastructure adoption across all types of businesses, from SMEs to banks and FIs.

There are companies like open finance pioneer Brankas that have been democratizing aggregated API solutions and financial infrastructure access. This enables financial services to be embedded in customer journeys like transportation and healthcare. It also enables more secure and transparent data access and sharing for banks and FIs as they offer new products or partner with other companies to do so.”

Read the full article

Essay 12: Fintech, Monetization, Diversification: Takeaways From The Google, Temasek, Bain E-conomy SEA 2023 Report (November 2023)

“Digital financial services have taken on a significant share of revenue over the past year, and show continued momentum in markets like Indonesia, Vietnam, and the Philippines, where the growth potentials are highest.

In particular, embedded finance and wider integration of digital financial services across platforms as adjacent revenue sources will create an “arms race” towards bridging capital access (i.e., proprietary underwriting algorithms / credit bureaus for unbanked segments or previously uncovered products and services).

This aligns with lending being the largest driver of revenue for DFS and loan demand continuing to grow in spite of rising interest rates. Ultimately, digital financial services arms race is ultimately a data arms race, as companies with more robust data infrastructures and flywheels will be better positioned to offer more comprehensive and complex financial products and services.”

Read the full article

Essay 13: How The Next Five Years Of ASEAN Fintech Will Be Different: 8 Fintech Trends To Watch (November 2023)

“To truly unlock the value of global payments in Southeast Asia, it will be key to build greater interoperability between banking platforms and payment systems.

Tonik Strategic Development Lead Jui Takle: “What it lacks is interoperability between digital banking platforms and payment systems, which is a major obstacle in the growth of digital banking in Southeast Asia. Interoperability allows seamless transactions between digital platforms and systems, just like how it is in India with UPI. In any ecosystem, the first thing that develops is payments, and then the rest follows. So I would say that there is still some time for Southeast Asia to mature.”

It will be exciting to see in the next five years how AI, and especially generative AI, will contribute to building increasingly personalized experiences for consumer fintech applications.

Tonik Strategic Development Lead Jui Takle: “The other thing is enhancing customer experience and innovating products that are unique to customer needs in that region. People don’t want to stand in long lines. Today, they just want everything done quickly on their phones, and they want personalized experiences. The traditional banks in the Philippines have realized the value of this seamless experience that we and other digital banks are giving, so they are also trying to get into it.””

Read the full article

2024: Ecosystem of Enablers for Digital Banking Emerges as Fully Digital Banks Refocus to Achieve Profitable Scale

Essay 14: 4 Things We Learned About The Future Of Banks And Banking Transformation For 2024 (February 2024)

“(1) Digital user experience is not enough for digital banks to be sustainable. As Tonik CEO and Founder Greg Krasnov shares in a LinkedIn post on a The Business Times article featuring his insights on the industry, “[Sorting] out unit economics first…allows [digital banks] to scale confidently, with not only monetization, but actual positive customer-level profitability.

Tonik has developed this through their loans, from shop installment loans to their recently launched SME loans, all seamlessly accessible through their app and integrations with retail and payment partners.

(2) But user experience is still a point of competition as more agile, digital players enter the market. Open finance company Brankas’ Bank Stability Report 2023 highlights room for improvement in terms of uptime for banks in their dataset (Indonesia, Philippines) compared to the minimum requirements for Singapore banks. This comes with digital banks and fintechs already capturing 47% of all new checking accounts opened in 2023.

As the report concludes, “In light of more sophisticated cybe attacks, the need for more frequent cross-border access, and banking support for a multitude of platforms and devices, banking needs to be secure, accessible, and trustworthy.”

(3) Generative AI can be at the intersection of driving unit profitability and improving customer experience. Gen AI has the potential to decrease technical debt as well as improve productivity of large customer-facing and white-collar workforces.

McKinsey & Company reported that Gen AI could increase the overall industry revenue by US$340B and operating profits by 15%.

For example, WIZ.AI’s generative AI solutions have helped increase customer reach by 70% and save 72% on costs for banking customer growth. More in their “Increasing Bank Competitiveness with Generative AI” whitepaper.

(4) Leveraging generative AI is best done with effective data capture and processing at scale, especially for regional banking operations, to then train proprietary LLMs.

This means taking a look at the hood and automating data processes at scale — something that bluesheets has made its bread and butter with AI-based products around accounting and insurance processing especially.”

Read the full article

Essay 15: 5 Insights Into Indonesia’s Fintech Industry In 2024 (May 2024)

“As more Indonesians adopt ewallets and (digital) banking accounts, competition is not just about driving adoption, but retaining usage of the “stored value” of customers in these ewallets and banking accounts.

“If you see in Indonesia as well, most larger fintechs or super apps have a banking part to it as well. Banking is getting embedded into the whole experience. So I think that’s how I see 2024 and beyond where I think neobanks alone find it very hard to scale. So that’s why everyone is getting associated with let’s say a larger ecosystem.

So that is a kind of theme which I see playing as well because with FinTech and banking merging that way, users will get a better experience in terms of the money they are storing and store value as well.

That redefines how people look at FinTech. So once a baseline is set, others start to do the same thing. So your differentiation or competitive advantage, I don’t think lasts very long in the tech world.” – Flip VP of Product Sourabh Gupta”

Read the full article

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.