About the episode

In this episode, to help us better understand what it takes to build a neobank in Southeast Asia, we called Andrea Baronchelli, CEO and co-founder of Aspire (Y Combinator Winter Cohort 2018). We talked about how Aspire is becoming the banking platform of choice for SMEs in the region, from the pain points and risks of the neobanking trajectory to forging partnerships and a path to profitability. Andrea also shares lessons from his years as a Lazada co-founder and executive.

Takeaways on building an SME neobank for SEA

Key Takeaways on Neobanking in Southeast Asia from our call with Aspire CEO and co-founder Andrea Baronchelli

Key Takeaways on Neobanking in Southeast Asia from our call with Aspire CEO and co-founder Andrea Baronchelli (Part 2)

About our guest

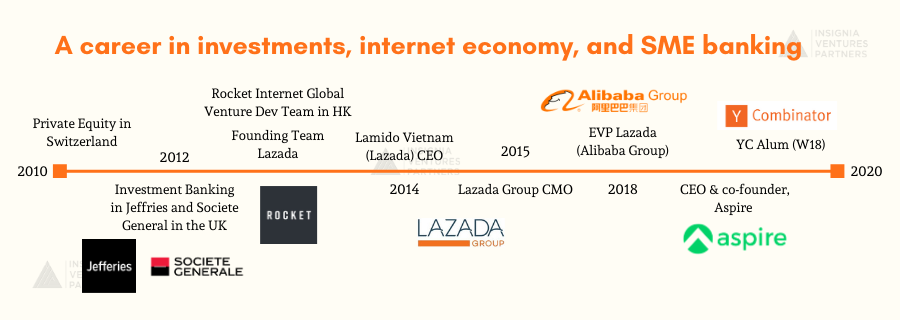

Prior to Aspire, Andrea Baronchelli was the CMO for Lazada in Singapore. He was part of the Lazada founding team and spent 6 years building the #1 e-commerce platform in Southeast Asia across Indonesia, Thailand and Vietnam. He also held several leadership positions within Lazada and Alibaba Group including regional EVP and CEO for the Vietnam business. Andrea is a Y-Combinator & Rocket Internet Alum. Before joining Lazada Group, Andrea was based in London in Investment Banking with Jefferies and Societe Generale.

Andrea Baronchelli’s ten years working in investments, internet economy, and SME banking

Timestamps

00:04 Introducing Andrea Baronchelli;

00:50 Check-in on how Aspire is operating remotely;

01:14 Origins of Aspire’s neobanking trajectory;

02:29 Unique aspects of building a neobank in Southeast Asia;

03:41 Infrastructure risk of building a neobank in Southeast Asia;

04:21 How Aspire has been addressing pain points of SMEs for financial services (with examples);

06:34 Aspire 2.0;

08:05 Proposition for banks;

10:27 Approach to partnerships (with the likes of Visa, Nium, TransferWise);

11:54 How Aspire operates in four markets;

12:58 What will set Aspire apart moving forward;

14:38 Lessons from Lazada and why Andrea chose to go into SME banking;

16:00 What to expect from Aspire moving forward;

16:50 Rapid-fire Recommendations from Andrea;

Transcript

Paulo: Welcome back to On Call with Insignia, where we go on call with Southeast Asia’s emerging technology startup leaders, and investors. Today we have on call with us from Singapore, Andrea Baronchelli, CEO and co-founder of Southeast Asia’s leading neobanking platform for SMEs, Aspire.

Aspire is building business banking for a new generation of entrepreneurs and business owners in Southeast Asia. In Southeast Asia, there are over 39 million underserved SMEs when it comes to financial services and Andrea and I will be talking about how Aspire is working to better serve their needs.

Welcome to our show, Andrea.

Andrea: Thank you Paulo and the Insignia team for having me, and I’m happy to share a bit more on how we plan to help these SMEs better and about our mission.

Paulo: And just to get the ball rolling, how are you doing right now and how are you managing and leading the company?

Andrea: So we are all quite remote. So we have people working in different countries. We are mostly working from home and overall a good vibe. I think we are much more efficient. We tend to call each other a lot on both Slack and Google Hangouts. And I think communication has been great so far.

Paulo: Yeah, that’s great to hear. And I’d like to dig deeper into Aspire’s trajectory, right? You initially started from offering lending services and now have gone on to offer much more than that and heading towards becoming a neobank. And that trajectory is something that we’re seeing across many fintechs across the globe. Was neobanking, part of the plan from day one? And if not, how did this story, neobanking story evolve for Aspire?

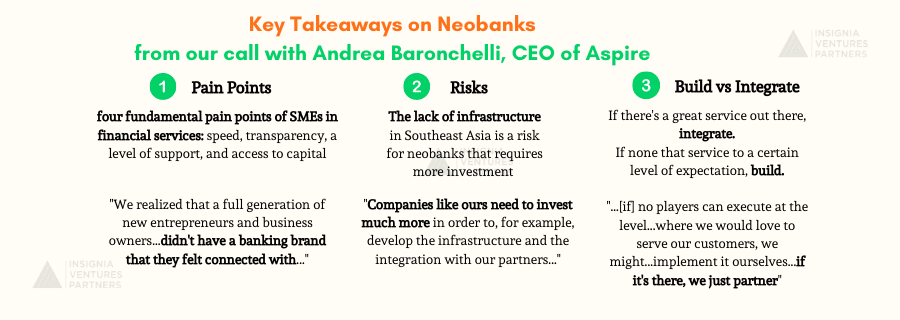

Andrea: Yeah. So we started our journey helping these SMEs that are unfairly underserved by the incumbent financial institutions with a credit line product in 2018. And then we opened up as you said to more and more products to complete our offering. And we realized that, as we were building Aspire, that a full generation of new entrepreneurs and business owners, they didn’t have a banking brand that they felt connected with and that was offering digital financial services with speed and transparency that they expected. And so we found a great opportunity to create a fully-fledged SME banking platform to become their banking partner. So that’s our journey so far.

Paulo: So this approach to offering financial services and driving financial inclusion for SMEs, this is something that I would say Aspire is one of the first in Southeast Asia, but this has been going on around the world for some time already. And as an SME fintech in Southeast Asia with a lending core, Aspire can be compared to Oak North, right, an SME challenger bank in Europe.

So how is this SME neobanking journey different in Southeast Asia? How would you compare what you’re doing here in the region to what other players are doing in other markets? Are there any key advantages or disadvantages in building this model in Southeast Asia?

Andrea: Yeah. Southeast Asia on one end as you mentioned, the model of an SME banking has been around for a while outside globally and there are various models. Southeast Asia is more complicated because by itself it’s made of different countries with different jurisdictions and different frameworks.

On the other hand, compared to other parts of the world, the industry is really nascent. So the opportunities are bigger due to the lack of a lot of players trying to solve these problems. And so at the same time, I mean, we see a great opportunity here for us.

Paulo: So the opportunities are bigger here in Southeast Asia given that the space is a bit more nascent. Are there any risks, in terms of growing this kind of business when it comes to Southeast Asia, apart from the regulations that are different from market to market? Are there any other risks when it comes to the business model, to the product itself, to the offerings?

Andrea: Some other risks could be related to the infrastructure that is a bit lacking in this market. And so companies like ours need to invest much more in order to for example, develop the infrastructure and the integration with our partners, which might first of all, delay a bit the go-to-market and also requires a bit more investments on this financial infrastructure.

Paulo: And you mentioned earlier when you were talking about the pain points of the SMEs here in Southeast Asia, they’re really looking for a banking brand, as you mentioned that’s offering, you know, financial services with that speed and transparency that they expect and Aspire has addressed that with its UI/UX and data approach. Could you explain a bit more what that means for Aspire and from the perspective of the SMEs?

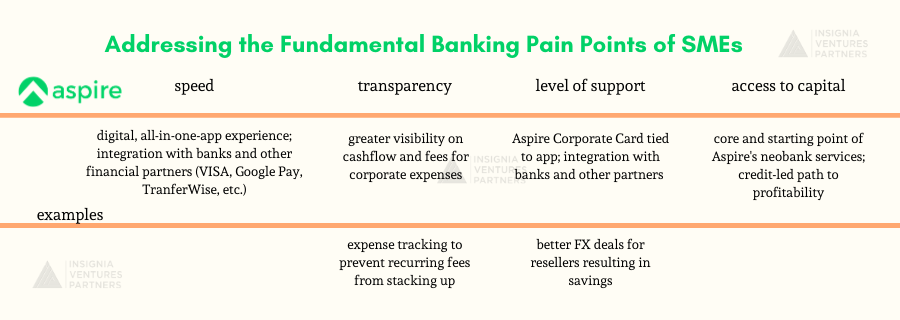

Andrea: Yeah, sure. From an SME perspective, when you think about financial services, it means speed, transparency, a level of support and access to capital. So these are the fundamental pain points that small business owners are facing and this is exactly what we’re trying to solve by focusing on their experience.

Paulo: Could you share an example or could you share a specific feature, that helps in terms of this, in terms of the speed, the transparency, support and access to capital?

Andrea: Yeah, we have a lot of examples of business owners and SMEs and startups that get really excited, right, when they start to use our business account app and they realize that everything that they’ve done before can be much simpler, much more seamless, so we managed to get them super excited.

And the fact that we really invest a lot to make the experience great. So for example, we have several customers that are good resellers. So they used to buy inventory from China on B2B commerce for example Taobao, Alibaba.com. And they were really getting really bad FX deals from their old corporate cards.

And so last week, for example, we received two thank you emails saying that it was really awesome for them to switch to the Aspire corporate card for the transparency with the fees and the savings that we are giving them.

And of course there are other examples, right? So we hear a lot about expense tracking. So the ability to have a clear picture of all the expenses, transaction by transaction, flowing from the account to the accounting software, from the card to the accounting software and managing business insights and accounting. And everything basically is around this better usability and a lot of transparency on what’s going on in the background — how the fees stack up, which is something in the industry, tends not to be super, super clear, clearly communicated at least.

How Aspire is addressing the fundamental pain points of SMEs when it comes to financial services

Paulo: So I think it’s really interesting that Aspire’s focus by providing a platform that offers this transparency and usability really targets pain points that aren’t so apparent to the business, as you mentioned, fees that can stack up and insights that aren’t clear with, more traditional, ways of accounting or doing things, right.

So I think that’s really interesting. And now you’ve since launched your app more than a year ago, and now you’re upgrading that app to Aspire 2.0, and you’ve recently launched that newer version, right. Could you tell our listeners more about how the app has evolved in that regard? What does Aspire 2.0 mean? And how do these new UX improvements fit into Aspire’s neobanking story?

Andrea: Yeah. So as you mentioned, we just launched a completely redesigned experience, which was taking a lot of the feedback that we received into account. And the idea is fundamentally for a small business owner to control its full cash flow management cycle via the same app including the debit inflow and outflow, remittances, card spend, credit limits, but in a super simple and intuitive way.

So when you come into the application, you’ll find messages like, “What would you like to do today?”, simple access to the insights, which is typically something that our customers really like and overall, this sense of transparency about fees and about explaining how the features work.

Read more about how Aspire 2.0 came about from Aspire’s Head of Product >>>

Paulo: Yeah, I think, that’s just like you mentioned before, it’s really about all of these like obvious things that people tend to miss and then, you know, Aspire is really changing that by continuously improving usability on the app. And so speaking of that seamless user experience, it’s not just about the features, right?

You also have to form a lot of important partnerships in order to build out your pipeline of services for SMEs. And so one of the key tie-ups for Aspire has been with banks. What’s the main proposition for banks to partner with Aspire? What do you tell them to get them on the platform and connect with SMEs on your platform?

Andrea: Yeah. So the key for us is that we are targeting a specific demographic of SMEs that prefer a digital native brand and an open ecosystem platform. So we are talking about digitally savvy, early adopters, generally young people that still manage a business, right? And we build an in-house core banking system that allows us to connect with existing ecosystems and stay relevant.

‘Cause nowadays the type of tools that these businesses use, they change fast and they want this tool to be integrated with their cash flow management system. To our bank partners, we are that effective acquisition partner and retention partner from which they can get business, right, whether it’s deposits or credit opportunities and revenue share.

Paulo: And so you offer this business opportunity to the banks, and for the banking industry in general, what’s the trajectory going to be like for, the relationship between fintechs and banks in serving these SMEs? Do you think that there will be more platforms like yourself serving as a platform for these banks and SMEs? Will more banks also try to build out their own platform to directly serve their business clients?

Andrea: I think it’s going to be a mix of everything. Everyone will try whatever works better for them. What typically works is that it’s not easy for an organization, right, that is usually not so dynamic to basically create a lot of different propositions.

So the level of customization is not really high, I mean, for a typical incumbent player. So the value of a fintech is that it can really customize the product towards a specific demographic or a specific segment. And that’s the value it brings in the market.

And to that extent, I think there’s going to be a lot of interesting collaborations, between banking players and fintechs.

Read more about our take on banking-fintech partnerships in Asia >>>

Paulo: And speaking of interesting collaborations, over the past few months, at least in the headlines we’ve seen some interesting partnerships for Aspire, right? One of them is with Visa and Nium for the Aspire corporate card. And recently with TransferWise, could you talk about how these partnerships formed, and also how these partnerships concretely impact the business. How have they improved the number of business accounts that have been coming into Aspire?

(from left) Venkatesh Saha, TransferWise’s head of Asia-Pacific and Middle East, with Andrea Baronchelli

Andrea: So the idea for us is that we want to serve our customers right around the full spectrum of banking products, so what I mentioned a bit before and with the best possible offering obviously, and the approach for us is that if we find awesome services right in the market, that our customer might benefit from we’d just prefer to integrate them. For example, with the TransferWise FX rates and the idea is basically to not build everything from scratch, right?

For other services, for example, where we feel that there’s no players, maybe in the market that can execute at the level of service where we would love to serve our customers, we might decide to implement it ourselves. The example for us was some of our credit line products, and we can do it ourselves. And again, it basically built up this sort of full-fledged services that we want to bring this for our target demographics.

Paulo: So it’s basically look for the best platforms or services that cater to what you want to offer to the SMEs and if it’s not there, you guys are gonna build it yourselves, right?

Andrea: Yeah, correct. And if it’s there, we just partner.

Paulo: Right. And this whole trajectory that we’ve just been talking about has now resulted in Aspire, growing in four markets across Southeast Asia. So Singapore, Vietnam, Thailand, and Indonesia. One thing I found really interesting with Aspire in terms of the organization and the leadership is that you have like co-founders in each market and leaders who are focusing on a specific market. How has that affected how Aspire grows as a company that’s cross-border?

Andrea: So that’s really an interesting thing because we find it really helpful to have a distributed team because we need to make sure that we are always trying to be close to our customers and for us it has been working quite well. We started since the beginning as quite a distributed team.

I mean, obviously, we have people now working remotely anyway but even in the past, we had a lot of interaction across various jurisdictions. We have a lot of our regional strategies and teams that are taken not from people sitting in Singapore, even if Singapore is our headquarters. And this allows for the company to be not really centered, but it’s basically moving as the market is basically evolving.

Paulo: So really growing with the market and with your customers. and I guess because of the specific leaders that you have in each market, you’re able to better pay attention to what’s happening on the ground. Earlier, you mentioned about the market, not having that many competitors yet. I guess this is a matter of time, right?

It’s only a matter of time before we see more fintech players, catering to these similar services. And what I wanted to know is what would make a player like Aspire stand apart from the rest in Southeast Asia?

Andrea: So I think for us it’s really important, the synergy, between the credit product and the transaction banking product, right? Because we are one of the few players that managed to basically master both, which is a bit the Oaknorth example you mentioned before, right? The successful SME neobanking player that, you know, is that credit-led.

So it’s basically managed to create a lot of paths to profitability, monetization coming from credit. And so it can, you know, offer services which are cheaper than what other players could provide, if they will focus only on payments, right.

Paulo: Now that you’ve explained it, it seems obvious that credit is the way to go in terms of profitability, for a fintech in general. Why do you think that not many fintechs have really explored this space? And why have they been focused more on the asset side of things?

Andrea: I mean, typically, there’s a lot of payments-led fintechs, right? But if you talk to them, right, they will pretty much always tell you that trying to monetize via lending. Either they have it in the plans or they’re testing it out, or they are doing a bit on the side just to add some revenues on the topline, but it’s pretty clear in the industry, that’s one fundamental way, right, where eventually the path to profitability needs to come from.

Paulo: Right, so it’s really a matter of speed in terms of how the players move. So we’ve been talking about Aspire but before you co-founded Aspire and started to venture into neobanking for SMEs, you held several leadership positions in Alibaba and Lazada here in the region. So what were some of the key lessons from your six years there that have helped in building Aspire?

Andrea: I mean too many, I would say, but if I have to narrow it a bit I think the idea [to] not to be worried about iterating and learning and together with this many more, obviously.

Paulo: And how did your experience in ecommerce sort of influence your decision to go into fintech and lending?

Andrea: For me, one thing was trying to get into something impactful, where I had the opportunity of having an impact on someone’s business, someone’s family, something that is meaningful in an external way.

And the second was the idea of B2B. So something functionally helpful a bit and obviously the problem of the digital economy in Southeast Asia is really fresh, right?

We are talking about now eight years, right, since we had the first purchases online and the first businesses that started to focus on supplying basically, and filling that demand and the whole ecosystem is evolving and they all need the different way of addressing financial services. It’s something that I was really excited about.

Paulo: Right, and this desire to create impact, what does that mean moving forward for Aspire as you go on this neobanking trajectory. You’ve covered already a lot of different offerings for SMEs. What are still some of the missing elements and synergies that you’re looking forward to covering in the next few years?

Andrea: Yeah, so we’re basically building our company to help SMEs and be there as they grow. So we will always be looking around for products and services they need from their financial service banking partner and try to find the best way to serve them. So we like to think about it as a way to honor entrepreneurs, right, and to really try and to make sure that they identify us as someone that has built a business centered in them, which is not something that they see frequently.

Paulo: Yeah, so a business that really puts other SMEs, other businesses at the center. That wraps up our conversation today and to close things off we always ask our guests to share some of their favorite things in our rapid fire question round.

What is your favorite book on entrepreneurship?

Zero to One by Peter Thiel

What app do you use the most nowadays that you think not many people use?

Navigator, managing agenda for meetings, can integrate with Gmail

What is your favorite, go-to destination in Southeast Asia?

Vietnam (Danang), I lived there and still go back often for vacation.

What is your favorite activity to de-stress?

Cycling (recently) and sailing (best spots in Vietnam!)