Across Singapore, Hong Kong, Tokyo, Bangkok and increasingly Seoul, Asian regulators have converged — at different speeds and in different forms — on a bank-anchored model for stablecoin issuance. The architecture they’ve built since 2023 has implications well beyond compliance, and the United States, even after its early-May breakthrough, is still racing to catch up.

Stablecoin issuance in Asia has quietly become a banking activity, not a fintech one. Across 2023 to 2026, the region’s major financial centres have each built — at materially different speeds, and through materially different statutes — a regulatory architecture that places stablecoin issuance inside the regulated banking perimeter rather than in a sandbox or a tolerated grey zone. The pattern has been consistent enough that the central question is no longer whether Asia is converging on a model. It is what that model means for the application layer that runs on top.

The most recent and most explicit confirmation came on 10 April 2026, when the Hong Kong Monetary Authority issued the city’s first two stablecoin licenses [1]. One went to HSBC. The other went to Anchorpoint Financial, the joint venture led by Standard Chartered with HKT and Animoca Brands as partners [2]. The licensing decisions ended a multi-year debate about how Hong Kong would compete with Singapore on digital asset infrastructure, and the answer that emerged is more interesting than the binary the market was watching for.

Hong Kong did not chase Singapore. It built a different framework, anchored on bank balance sheets rather than fintech innovation pathways, and shipped it eight months after the Stablecoin Ordinance came into force on 1 August 2025 [3]. The first two licensees are not crypto-native. They are the largest non-Chinese commercial bank in Asia and a bank-anchored consortium with a telco distribution partner and a regional digital-assets platform. That choice — who gets licensed first — is the signal.

It was also a deliberately small choice. Eddie Yue, HKMA Chief Executive, confirmed on 5 May 2026 that the regulator received approximately 36 applications under the Stablecoin Ordinance, of which only the two were approved in the first round [4]. Future licenses, Yue said, will be conditional on market conditions, risk levels, and the operational track record of the first issuers. “The goal is not to flood the market with many issuers,” the HKMA’s accompanying statement made clear; the regulator wants a small, controlled cohort that can be closely watched. The cautious-rollout posture reinforces, rather than dilutes, the thesis: stablecoins in Hong Kong are infrastructure, not sandbox.

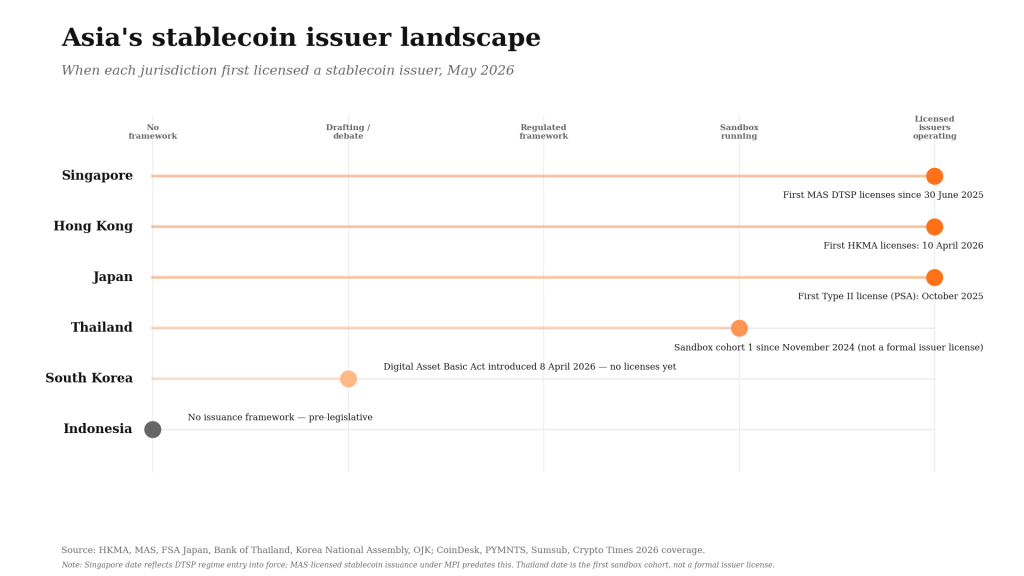

Exhibit 1. Asia’s stablecoin issuer landscape — a bank-anchored convergence. Status and named issuers across major Asian jurisdictions, May 2026. Source: HKMA, MAS, FSA Japan, Bank of Thailand, Korea National Assembly, OJK; CoinDesk, PYMNTS, Sumsub, Crypto Times 2026 coverage. Stage classifications reflect operational status as of May 2026; issuer lists are illustrative of named licensees and pilot participants.

How Hong Kong’s framework slots into Asia’s existing regulation

Asia’s stablecoin regulatory architecture has been building incrementally for the better part of three years. Hong Kong’s licenses are the most recent piece, not the first.

Singapore — MAS Digital Token Service Provider regime. Singapore began refining its Payment Services Act treatment of stablecoins in 2023 and finalised the Digital Token Service Provider framework through 2024–2025 [5]. The MAS regime treats stablecoins as a subset of regulated payment instruments, with full reserve requirements, licensed issuers, and guaranteed redemption rights. Singapore’s approach has been the global reference cited by every other regulator that subsequently introduced stablecoin rules — including the HKMA itself. MAS confirmed at the Singapore FinTech Festival in November 2025 that draft stablecoin legislation will be published in 2026.

Thailand — Bank of Thailand pilots. The BoT launched its Programmable Payment Sandbox (Stablecoin Sandbox) in 2024 and expanded it in December 2025 to safely test Thai Baht–backed stablecoins and programmable payment solutions, with three sandbox participants — SCB 10X, Kasikornbank and Ascend Bit — running pilots through 2025 and 2026 [6]. The April 2026 announcement of a stablecoin-based cross-border transfer exploration between DeeMoney and the Bank of Thailand [7] is one piece of a multi-year programme of state-blessed pilots.

Japan — already operational, increasingly bank-anchored. Japan’s Payment Services Act amendments, in force since June 2023 and refined further through to June 2026, restrict yen-pegged stablecoin issuance to three categories of licensed domestic entities: banks, fund transfer service providers, and trust companies [8]. JPYC became the world’s first fully regulated yen-pegged stablecoin under a Type II license in October 2025, and on 28 April 2026 the FSA formally classified JPYC under the regulated payment services framework [9]. The next wave of issuance is bank-led: SBI Holdings and Startale Group are launching the JPYSC stablecoin in Q2 2026, with Shinsei Trust & Banking handling issuance and redemption [10]. Japan’s three megabanks — MUFG, SMBC and Mizuho — are running joint proof-of-concept programs for trust-based yen stablecoins on the Progmat platform [8]. The pattern in Tokyo is the same as in Hong Kong: the regulator narrowed who can issue, and the result is a bank-and-trust issuer base rather than a fintech-led one.

South Korea — bill moving, central dispute unresolved. On 8 April 2026, South Korea’s ruling Democratic Party introduced the Digital Asset Basic Act, proposing 100 percent reserve requirements and bank-style operational standards for stablecoin issuers [11]. The bill is moving forward but the central dispute remains unresolved at the time of writing: the Bank of Korea insists on a 51 percent bank-ownership rule for any won-pegged issuer; the Financial Services Commission has pushed back, citing the EU’s MiCA framework — under which 14 of 15 licensed stablecoin issuers are electronic money institutions rather than banks — as evidence that fintech-led issuance can sit inside a bank-style perimeter. Earlier drafts of the government proposal indicate foreign-issued stablecoins (such as Circle’s USDC) would be permitted in Korea subject to a local branch or subsidiary requirement. Whichever way the 51 percent dispute resolves, Korean stablecoin issuance will be bank-anchored or bank-adjacent — the same regional pattern, with a slower timeline than Hong Kong, Singapore or Japan.

Indonesia — OJK and BI on parallel tracks. Indonesia’s Financial Services Authority (OJK) and central bank (Bank Indonesia) have not yet introduced a comparable issuance framework, but both regulators have engaged on digital asset governance through 2025 and 2026 in tandem with the country’s broader digital banking expansion. With 17 OJK-supervised digital banks now operating, the institutional substrate for a stablecoin issuance regime is materially more developed than it was eighteen months ago.

The pattern across the region is consistent. Asian regulators have moved at different speeds, but all of them are converging on a framework where stablecoin issuance is treated as an extension of the regulated banking system rather than as a fintech innovation category. Hong Kong’s choice to grant its first two licenses to bank-anchored entities is the clearest expression of this pattern to date.

Why the HKMA’s bank-anchored choice is the signal

The market’s binary read of the 10 April news — “Hong Kong is open for stablecoin business” — misses the more important detail. The deliberate first choice of HSBC and Anchorpoint Financial signals the HKMA’s view of who should be allowed to issue stablecoins in the Hong Kong jurisdiction at all.

Both licensees have already published concrete product roadmaps. HSBC plans to launch a Hong Kong Dollar–denominated stablecoin in the second half of 2026, fully backed by high-quality liquid assets in segregated accounts, supporting peer-to-peer payments via the HSBC HK Mobile Banking App and PayMe, peer-to-merchant payments for participating PayMe merchants, and tokenised investments via the HSBC HK App [2]. Anchorpoint targets to issue a Hong Kong Dollar–backed stablecoin branded HKDAP (HKD At Par) on a phased rollout from the second quarter of 2026 [12]. Both products are bank-balance-sheet instruments connected to existing consumer and merchant payment surfaces — not separate crypto rails.

This matters for the application layer in two ways.

First, the perceived counterparty risk on Hong Kong–licensed stablecoins drops to the issuing bank’s credit profile. For a Southeast Asian fintech building cross-border settlement on top of HKD-denominated stablecoins, the underwriting question becomes the same question one would ask of a wholesale bank deposit. That is a meaningfully different conversation from underwriting a USDT or USDC reserve composition.

Second, the bank-anchored model invites the rest of the regional banking system to participate. Singapore’s three local banks, Singapore-licensed foreign banks operating under MAS’s DTSP regime, Indonesian banks beginning their own digital asset conversations, Thailand’s commercial banks engaging via the BoT pilot, Japanese trust banks under the revised Payment Services Act, and the Korean banks contemplated under the Digital Asset Basic Act — all now have a reference precedent for how a developed-market regulator has chosen to organise the issuer base. Singapore’s MAS DTSP is interoperable with the HKMA framework in practice, and the application-layer providers shipping in 2026 are typically licensed in both.

Money20/20 Asia, held in Bangkok 21–23 April, served as a quick confirmation that the industry was reading the HKMA decision the same way. According to FXC Intelligence’s exhibitor analysis, 17 percent of all Money20/20 Asia exhibitors centred their primary product on stablecoin cross-border solutions — materially higher than any prior Money20/20 event globally [13]. That is a directional sentiment marker, not a policy event. The policy event is what happened in Hong Kong eleven days earlier — and what the HKMA has signalled, on 5 May, will be deliberately slow to follow.

The U.S. asymmetry, briefly — and updated

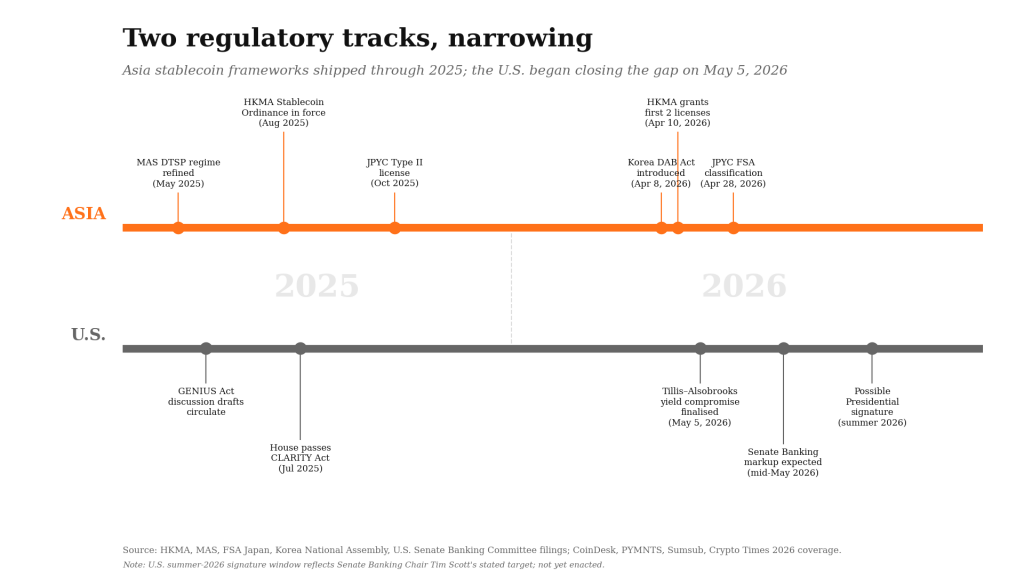

The original framing of this article assumed the U.S. would remain materially behind Asia for an extended period. As of 5 May 2026, that assumption needs to be tempered.

On 5 May, Senators Thom Tillis and Angela Alsobrooks announced that their Section 404 stablecoin yield compromise — the central blocker on the CLARITY Act’s progress through Senate Banking — was complete and final [14][15]. The compromise bars crypto firms from paying interest equivalent to a bank deposit but explicitly allows activity-based “bona fide” rewards, threading the needle that had stalled the bill since late 2025. Senate Banking Committee markup is now expected by mid-May. Senate Banking Committee Chair Tim Scott has stated publicly that he is targeting a presidential signature by summer 2026 [16]. The American Bankers Association and adjacent industry groups have signalled that the compromise language remains insufficient on bank-deposit risk, but the bill is moving regardless.

In other words: the gap is closing on the legislative side. What is not closing is the operational gap. The HKMA, MAS and BoT regimes now have months — and in Singapore’s case, years — of live operating data, integrated counterparties, and cross-border settlement throughput that the U.S. framework will not match by year-end even in the most optimistic legislative scenario. The asymmetry has shifted from “Asia ships, U.S. debates” to “Asia operates, U.S. is about to legislate” — a meaningfully different competitive posture, but still one in which Asian providers retain a head start.

Hassan Ahmed, Coinbase Singapore Country Director, on On Call with Insignia Ventures (13 April 2026):

“Stablecoins have especially strong product-market fit in payments, cross-border payments, payouts, and anything involving international movement of money. Venture-scale builders should take stablecoins very seriously.” [25]

What this means for the application layer in Southeast Asia

If stablecoin issuance is now solidly inside the regulated banking perimeter across Hong Kong and Singapore, with Thailand, Japan, Korea and Indonesia on observable adjacent tracks, the competitive question for SEA fintech becomes: which application-layer plays convert this infrastructure into durable cross-border revenue? One of our portfolio companies is already shipping at scale; two others sit in adjacent layers where the bank-anchored regulatory architecture creates concrete forward implications.

The live case — B2B neobank with stablecoin infrastructure already operating. StraitsX, the Singapore-headquartered digital finance infrastructure arm, secured Major Payment Institution licenses from MAS, launched the XUSD stablecoin alongside its existing XSGD, and disclosed cumulative on-chain volume above $28 billion across its rails — up from approximately $18 billion at the end of 2025 [18][19]. StraitsX has begun extending its payment network across Asia, beginning with enhanced connectivity between Singapore, Thailand, Taiwan and Japan, and a partnership with KASIKORNBANK for stablecoin-native cross-border settlement [19]. The Fazz / StraitsX combination is the cleanest demonstration in the SEA portfolio of what application-layer scale on top of bank-anchored regulation actually looks like at production scale today.

Tianwei Liu, StraitsX co-founder and Fazz Group Deputy CEO, on On Call with Insignia Ventures (Episode 186, 23 July 2025):

“We’re powerful because we’re regulated and positioned at the front seat of this expansion into real-world use cases. We’ve been operating in the real world for the past 10 years — doing payments for non-tech-savvy, underserved users. Imagine putting this kind of stablecoin infrastructure in their hands.”

Exhibit 2. Two regulatory tracks, narrowing. Asia’s stablecoin frameworks shipped through 2025 and into early 2026; the U.S. CLARITY Act timeline began closing the gap with the 5 May 2026 Tillis–Alsobrooks yield compromise. Source: HKMA, MAS, FSA Japan, Korea National Assembly, U.S. Senate Banking Committee filings; CoinDesk, PYMNTS, Sumsub, Crypto Times 2026 coverage. U.S. summer-2026 signature window reflects Senate Banking Chair Tim Scott’s stated target; not yet enacted.

Implication — Indonesia consumer rails as a future volume engine. Flip operates one of Indonesia’s largest non-bank consumer payment networks, supporting 13 million individual users and over 1,000 businesses [20]. Flip does not currently offer stablecoin-denominated capabilities; its existing cross-border product, Flip Globe, runs on fiat rails through a February 2025 partnership with Wise Platform that integrates Wise’s global payments infrastructure across 15 international payment routes [21]. The implication of bank-anchored HKD and SGD stablecoin issuance is forward-looking rather than current: the same kind of distribution surface area that made Flip’s Wise Platform integration viable becomes available for stablecoin-denominated settlement once SEA-licensed issuers are operating at scale. Whether and when Flip integrates that layer is a product decision; the regulatory substrate for it now exists.

Implication — treasury as a future margin engine. Finmo positions itself as a “next-generation Treasury Operating System” that unifies payments, cash and liquidity management, FX risk management and reporting for cross-border businesses [22]. At the Singapore FinTech Festival in November 2025, Finmo and Standard Chartered announced a strategic partnership integrating Standard Chartered’s global currency accounts and API-driven treasury connectivity into the Finmo platform, with Singapore as the launch market and the UAE, Hong Kong and the United Kingdom in the expansion roadmap [23]. The April 2026 launch of Finmo’s CFO and Treasurer Advisory Board, drawing senior practitioners from across Asia [24], signals where the operational conversation is heading.

David Hanna, Finmo CEO (Money20/20 Asia Digital Transformation podcast, 2025):

“Everyone has a treasury problem. Managing global currencies, trying to reconcile payments, doing FX and currency exchange. And there wasn’t necessarily a single solution that was solving that end-to-end problem for treasurers and CFOs.” [28]

Akhil Nigam, Finmo CPO and co-founder, on On Call with Insignia Ventures (Call 199, 2 December 2025):

“Stablecoins can be a part of real treasury. We’ve been talking about stablecoins for quite some time, and a lot of the companies we’ve been talking to are already thinking in that direction.” [29]

Finmo does not currently issue or settle in stablecoins. The implication of bank-anchored issuance, however, is concrete: regulated stablecoin infrastructure on the issuer side is what makes it possible — for treasury platforms in general, and Finmo in particular — to compress the 1–3 percent of FX friction that today sits at every cross-border conversion node into single-digit basis points on the underlying transfer.

The narrowing legislative gap, the widening operational lead

The U.S. is closing fast on the legislative side; the second half of 2026 is now plausibly the U.S. window. The operational gap is a different matter. Asian providers will have executed against live regimes for at least eighteen months in Singapore, twelve months in Hong Kong, longer in Japan, and progressively in Thailand and Korea by the time U.S. providers begin building under a domestic CLARITY framework. StraitsX alone has crossed $28 billion in cumulative on-chain volume [18]. The application layer that captures the next decade of cross-border B2B value is being built right now in Singapore, Hong Kong, Jakarta, Bangkok and Manila.

References

- HKMA. “Granting of stablecoin issuer licences” (press release). 10 April 2026.

- Bloomberg. “HSBC, StanChart Get First Hong Kong Stablecoin Issuer Licenses.” 10 April 2026. ; HSBC press release, “HSBC welcomes HKMA’s grant of a Hong Kong stablecoin issuer licence,” 10 April 2026

- Sumsub. “Hong Kong Stablecoin Regulation: HKMA Licensing Framework in 2026.” Updated 2026.

- Crypto Times. “Hong Kong Isn’t Rushing Stablecoins — Here’s Why.” 5 May 2026. HKMA insight piece, Eddie Yue, “Robust development of the regulated stablecoin ecosystem in Hong Kong,” 10 April 2026,

- MAS. “Guidelines on Licensing for Digital Token Service Providers” (regime in effect 30 June 2025; refined through 2025–2026).

- Tilleke & Gibbins / Lexology. “Sandbox Projects in Thailand: Innovation for Digital Assets and Finance” (Programmable Payment Sandbox launched 2024; expanded December 2025; participants SCB 10X, Kasikornbank, Ascend Bit). 2026.

- FXC Intelligence. “Highlights and key takeaways from Money20/20 Asia 2026” (DeeMoney / Bank of Thailand stablecoin pilot announcement). 24 April 2026.

- Bitcoin News. “Japan Stablecoin Regulation Explained: PSA Rules, JPY Coins and Bank Issuers” (PSA framework, three licensed issuer categories, MUFG/SMBC/Mizuho Progmat POC). 2026.

- Crypto Times. “Japan FSA Classifies JPYC Under Regulated Payment Services Framework.” 28 April 2026.

- The Coin Republic. “Metaplanet CEO Backs Yen Stablecoins As Ripple Partner SBI Nears 2026 Launch” (SBI Holdings + Startale Group JPYSC, Q2 2026 launch, Shinsei Trust & Banking as issuer). 4 May 2026.

- CoinDesk. “South Korea proposes comprehensive digital asset law including stablecoin rules” (Digital Asset Basic Act introduced; Bank of Korea vs. FSC dispute on 51% bank-ownership rule; foreign issuer local-branch requirement). 8 April 2026.

- Standard Chartered. “Standard Chartered-backed Anchorpoint granted Stablecoin Issuer Licence by the Hong Kong Monetary Authority.” 10 April 2026. FXC Intelligence. “Asia’s stablecoin lead: Insights from Money20/20’s showfloor.” 24 April 2026.

- CoinDesk. “Clarity Act text lets crypto firms offer stablecoin rewards while shielding bank yield.” 1 May 2026.

- Payment Expert. “US lawmakers advance CLARITY Act after stablecoin yield compromise.” 5 May 2026.

- Yahoo Finance. “Coinbase Backed Clarity Act Advances: Tim Scott Eyeing Summer.” May 2026.

- Fazz. “All-in-one finance for every Southeast Asia business” (homepage); $6B+ annualised GTV and $25M annualised revenue per company-published material accessed May 2026.

- PYMNTS. “Singapore’s StraitsX Sees Surge in Stablecoin Payment Volume” (cumulative on-chain volume figures). 2026.

- StraitsX. “StraitsX secures Major Payment Institution Licences and launches XUSD stablecoin” / “StraitsX to Extend Payment Network Across Asia, Advancing Stablecoin-Native Cross Border Settlement.” April 2026.

- Flip. Company profile, user base (13M individuals, 1,000+ businesses) and “#FlipBuatSemua” positioning. coverage via Crunchbase, Peak XV. Accessed May 2026.

- Wise Newsroom. “Flip partners with Wise Platform to Power Faster, Cheaper International Payments for Millions of Indonesians.” February 2025.

- Finmo. “Treasury Operating System” homepage and About. Accessed May 2026.

- Standard Chartered / Finmo. “Finmo and Standard Chartered Partner to Integrate Global Currency Accounts and API-Driven Treasury Connectivity.” Singapore FinTech Festival 2025, November 2025.

- Finmo. “Finmo Launches Inaugural CFO & Treasurer Advisory Board.” 30 April 2026.

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.