There is a useful fiction in how the financial technology industry has historically organized its ambitions. Quantum computing belonged to research labs and defense contractors. Stablecoins and tokenization belonged to crypto. Artificial intelligence belonged to product teams optimizing call center deflection. Each category had its conference circuit, its investor thesis, its five-year roadmap.

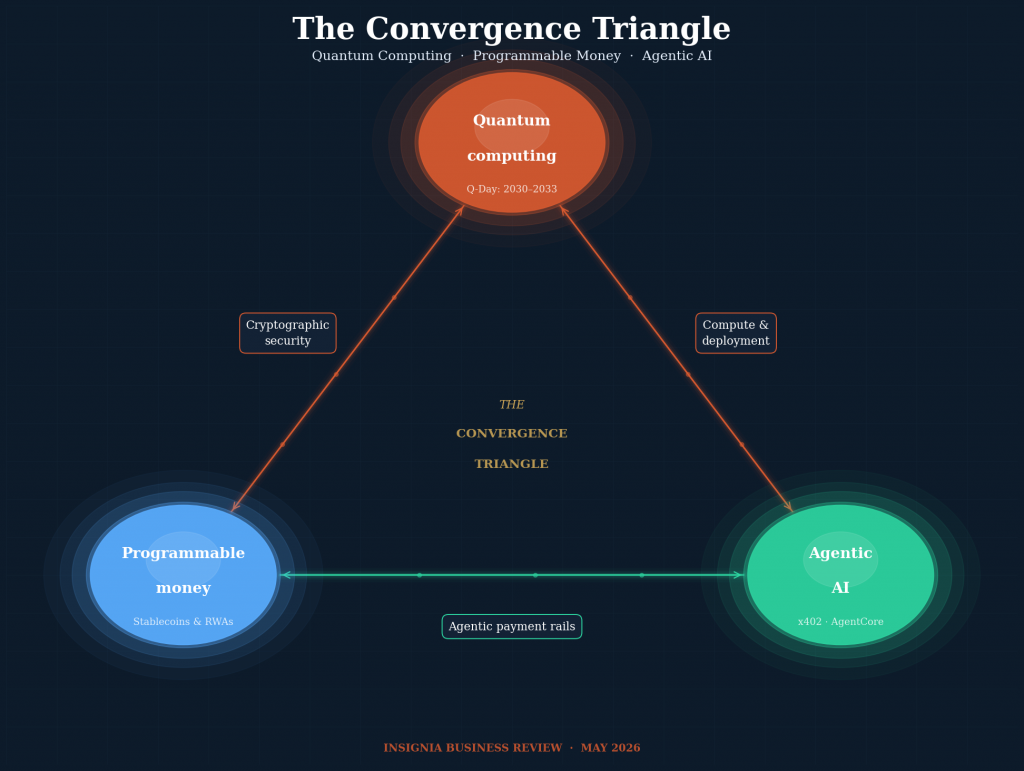

That compartmentalization is no longer descriptive. In the first five months of 2026, the three forces collided with unexpected speed, and the collision is not a coincidence. Quantum computing is compressing the timeline for when existing cryptographic infrastructure — the kind that secures every bank transfer, wallet signature, and token transaction on the planet — becomes vulnerable. Programmable money, arriving through stablecoins and on-chain real-world assets, is creating a settlement layer that AI can actually operate: instant, fee-less at the micro level, always-on, and addressable by software without human intermediaries. AI, in turn, is generating a new class of economic actors — autonomous agents — that are already transacting in stablecoins and for whom the legacy card and wire infrastructure was never built.

What the three technologies share is that each one individually produces incremental improvement to finance. Together, they produce structural replacement.

The Rails Beneath Everything

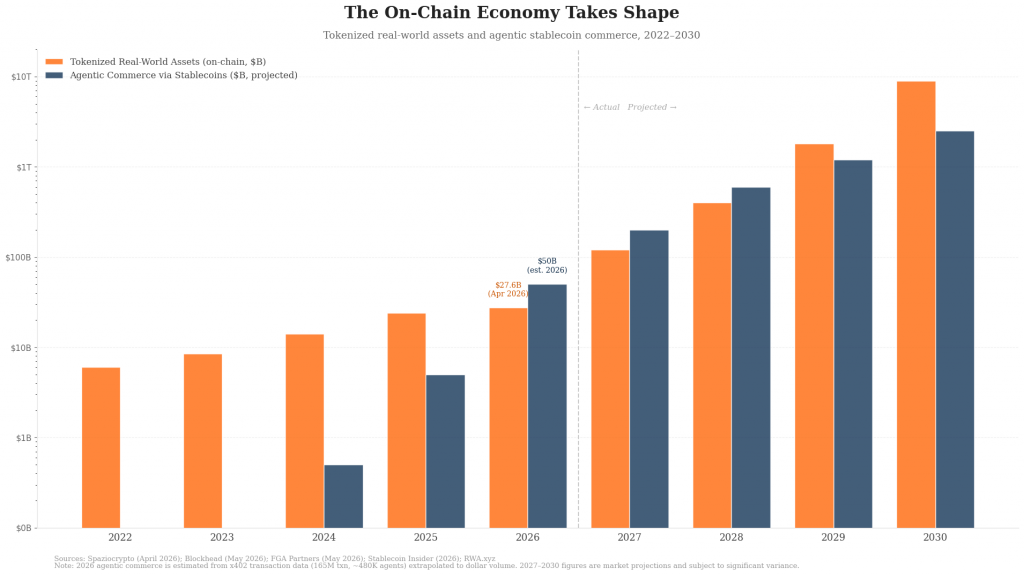

The stablecoin transition from speculative asset to institutional infrastructure has been underway for several years, but 2026 has clarified its shape. Tokenized real-world assets crossed $27.6 billion on-chain in April 2026, up from roughly $5.8 billion at the start of 2025 — a 266% increase in a single year [1]. The projections that circulated in 2021 as optimistic fiction, that tokenized assets would reach $9 trillion by 2030, are now treated by mainstream banks as baseline planning assumptions [2].

The regulatory anchor in the United States arrived this week. The CLARITY Act advanced through the Senate Banking Committee on May 14, 2026, after months of negotiation [3]. Its core mechanism — a 1:1 reserve requirement in high-quality liquid assets for every issued stablecoin token — effectively reconstitutes stablecoin issuers as narrow banks. Circle’s equity jumped nearly 20% on the compromise news [4].

The operational change this enables goes beyond balance sheet legitimacy. Programmable money — stablecoins with embedded logic, governed by smart contracts, settling in seconds — is qualitatively different from money that merely moves fast. A stablecoin can carry instructions with it: pay supplier B when shipment X is confirmed on-chain; release the escrow when the oracle reports the trade has cleared; distribute yield proportionally to token holders at midnight. These are not features that can be retrofitted onto correspondent banking. They are native to a different kind of financial infrastructure.

StraitsX, the Singapore-based stablecoin settlement layer and MAS-licensed Major Payment Institution, is building one expression of that infrastructure for Asia. In November 2025, StraitsX announced the expansion of its payment network to Thailand, Taiwan, and Japan, targeting Q2 2026 go-live [5]. The Thailand corridor, built in partnership with KBank and Orbix Technology, uses XSGD as the settlement asset between GrabPay and Thailand’s Q Wallet by KBank — allowing Thai travelers to pay at Singapore merchants using familiar QR interfaces while settlement happens instantly on-chain behind the scenes.

When the Agent Is the Customer

For the first decade of digital banking, the central design challenge was building better interfaces for human customers. The next design challenge is different: an increasing share of the transactions flowing through financial infrastructure will be initiated not by people, but by software acting on their behalf.

On May 7, 2026, Amazon Web Services launched Amazon Bedrock AgentCore Payments, built with Coinbase and Stripe [6]. The product enables AI agents running on AWS to pay for APIs, data services, and other agents autonomously, using USDC stablecoin, settling on Base in approximately 200 milliseconds at less than a fraction of a cent per transaction. The day prior, the Solana Foundation and Google Cloud launched Pay.sh, an open-source payment gateway for AI agents to access and pay for APIs on a per-request basis [6]. Coinbase’s x402 protocol processed approximately 165 million transactions across more than 480,000 transacting agents in its first year, and has since moved under the Linux Foundation with backing from Google, Stripe, AWS, Visa, and Mastercard [6].

Circle’s response arrived on May 12, 2026: the Agent Stack, a product suite that includes agent wallets, a service marketplace, and sub-cent “nanopayments” — USDC transfers as small as one-millionth of a dollar — positioned explicitly as the financial infrastructure of machine-to-machine commerce [7].

The consumer dimension is cumulatively larger. AI agents operating with financial authority on behalf of individuals — negotiating mortgage rates, executing recurring investments, switching utility providers, filing insurance claims — collapse the gap between financial advice and financial action. JPMorgan’s EVEE Intelligent Q&A assistant cut servicing calls per account by nearly 30% and processing costs by 15% [8]. Finastra’s 2026 survey projects that 44% of finance teams will deploy agentic AI this year, representing more than a 600% year-over-year increase [9].

The Sword in the Infrastructure

The third force operates on a longer timeline but a shorter fuse than most financial institutions have acknowledged.

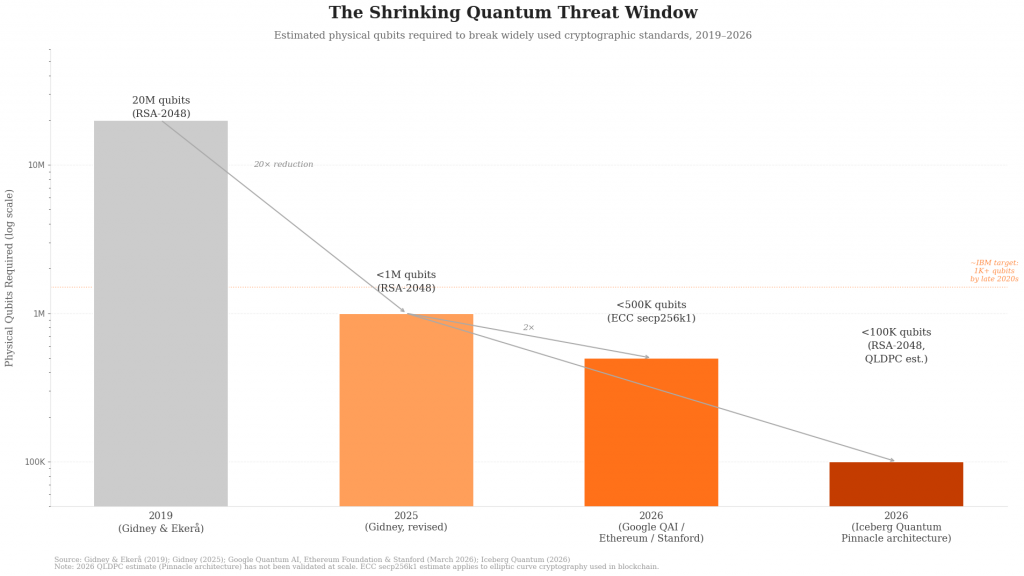

The cryptographic systems protecting every transaction on the planet — RSA, elliptic curve cryptography, the signature schemes underlying Bitcoin, Ethereum, and every bank’s TLS layer — were designed for a world without fault-tolerant quantum computers. In 2019, the best estimate for breaking RSA-2048 required approximately 20 million physical qubits. Research published in May 2025 revised the estimate to under one million qubits — a 20-fold reduction driven entirely by algorithmic improvements [10]. A March 2026 paper from researchers at Google Quantum AI, the Ethereum Foundation, and Stanford further revised the estimate for breaking elliptic curve cryptography: fewer than 500,000 physical qubits, representing another 20-fold reduction [10].

Project Eleven’s 2026 blockchain security report places Q-Day — the moment when a quantum computer could feasibly break elliptic curve cryptography — between 2030 and 2033 [11]. More than $3 trillion in digital assets are currently secured by cryptographic schemes that become vulnerable at that threshold [11]. The “harvest now, decrypt later” risk — where adversaries collect encrypted financial data today for decryption once quantum capability matures — is already operative for any data that must remain confidential beyond 2030.

The constructive application of quantum computing in finance runs parallel to the threat. Hybrid quantum-AI systems are demonstrating materially improved fraud detection: early adopters report accuracy improvements of 25–40% with false positive rate reductions of up to 60% [14]. The McKinsey Quantum Technology Monitor 2026 frames this year as a “commercial tipping point” for hybrid quantum-AI deployment across financial services [15].

How the Triangle Moves Together

The three forces are not simply additive. They compound.

Post-quantum cryptographic migration is a prerequisite for the long-term integrity of stablecoin and tokenization infrastructure. The $27.6 billion in on-chain RWAs and the agent payment networks are secured today by elliptic curve cryptography — the same scheme researchers estimate can be broken with fewer than 500,000 qubits [10][11]. Only 0.35% of blockchain implementations had adopted post-quantum algorithms as of 2025 [11]. Stablecoin issuers and tokenized asset platforms that address this migration proactively will hold a structural security advantage.

AI agents require stablecoin rails to operate at scale. The x402 protocol settles in 200 milliseconds at sub-cent fees [6]. As on-chain networks migrate to post-quantum signature schemes, the same infrastructure that enables machine micropayments gains a cryptographic durability that makes it viable for institutional-grade AI agent commerce — autonomous treasury management, cross-border procurement, real-time insurance adjustment.

The consumer experience produced by this convergence is one that no individual technology achieves alone. A consumer sees an account that understands their financial behavior in real time, acts on their behalf across multiple institutions and currencies, settles instantly across borders, and does so over infrastructure that remains cryptographically secure as quantum computing matures.

The Business Model Rupture

The combination of programmable settlement, autonomous agents, and quantum-hardened infrastructure does not merely improve existing financial products — it obsoletes several of the mechanisms through which banks and financial platforms currently generate revenue.

Float income compresses toward zero on stablecoin rails, where settlement is continuous and reserve assets are held 1:1. Payment interchange is structurally incompatible with the sub-cent fees that agent commerce requires. Credit underwriting based on backward-looking bureau scores is displaced by models that reprice in real time on behavioral data. The models that emerge in their place:

- Utility fee models — revenue scales with transaction volume rather than balance sheet size

- Programmability-as-a-service — conditional payments, auto-rebalancing, and event-triggered escrow command margin

- Agent account economics — the institution that holds the agent wallet becomes the primary financial relationship for an expanding share of economic activity

- Post-quantum security premium — institutions completing cryptographic migration early can price security posture as a differentiated product feature

The World Economic Forum’s January 2026 analysis frames the risk of delayed quantum migration not as a cost problem but as a market structure problem: institutions that complete the transition gain the ability to offer quantum-safe products as a differentiated category, while those that delay face a potential “two-tier” financial system [16].

Building on a Live Experiment

Southeast Asia is not waiting for the convergence to resolve in the West. The region’s combination of mobile-first consumer populations, underbanked credit markets, and regulatory environments that have moved faster than legacy banking incumbents make it a faster feedback loop for all three technologies simultaneously.

StraitsX’s Q2 2026 payment network launch across Singapore, Thailand, Taiwan, and Japan is a live test of stablecoin infrastructure as everyday consumer and institutional settlement. AWS AgentCore Payments and Circle’s Agent Stack are being adopted by fintechs in the region as the foundation for agent-powered financial products. And Singapore’s Monetary Authority has been among the more active global regulators in publishing quantum security guidance for financial institutions.

The convergence triangle is not a future scenario. It is the infrastructure being built today, and the window to position on the right layers of it — compliant stablecoin rails, agent-native financial products, and quantum-hardened cryptography — is narrower than it appears.

References

[1] “Tokenized RWAs Hit $27.6 Billion: The 2026 Institutional Boom Explained,” Spaziocrypto, April 2026. https://en.spaziocrypto.com/rwa/tokenized-rwa-27-billion-institutional-boom-2026/

[2] “RWA Tokenization in 2026: How Real-World Assets Are Moving Onchain,” Blocklr, 2026. https://blocklr.com/news/rwa-tokenization-2026-guide/

[3] “LIVEBLOG: Senate Banking Committee advances Clarity Act to full Senate floor,” CoinDesk, 14 May 2026. https://www.coindesk.com/policy/2026/05/14/live-senate-banking-committee-holds-key-hearing-to-advance-clarity-act

[4] “Circle jumps nearly 20% on Clarity Act compromise that preserves stablecoin rewards,” CNBC, 4 May 2026. https://www.cnbc.com/2026/05/04/circle-jumps-16percent-on-clarity-act-compromise-that-preserves-stablecoin-rewards.html

[5] “StraitsX to Extend Payment Network Across Asia, Advancing Stablecoin-Native Cross Border Settlement,” StraitsX Blog, 4 November 2025. https://www.straitsx.com/blog-post/straitsx-to-extend-payment-network-across-asia-advancing-stablecoin-native-cross-border-settlement

[6] “AI Agents Are Paying Bills in Stablecoins — The Infrastructure Race Is On,” Blockhead, 8 May 2026. https://www.blockhead.co/2026/05/08/ai-agents-are-paying-bills-in-stablecoins-the-infrastructure-race-is-on/

[7] “Circle Launches Agent Stack to Put USDC at the Centre of Machine-to-Machine Payments,” Blockhead, 12 May 2026. https://www.blockhead.co/2026/05/12/circle-launches-agent-stack-to-put-usdc-at-the-centre-of-machine-to-machine-payments/

[8] “The Autonomous Banker: How AI Agents Will Rewire Wall Street’s Profit Engines by 2026,” Unbox Future, May 2026. https://www.unboxfuture.com/2026/05/the-autonomous-banker-how-ai-agents.html

[9] “AI in banking and financial services: Trends for 2026,” Finastra, 2026. https://www.finastra.com/viewpoints/articles/future-of-ai-in-financial-services-2026

[10] “Why 2026 Matters for Quantum Security,” The Quantum Insider, 28 April 2026. https://thequantuminsider.com/2026/04/28/why-2026-matters-quantum-security/

[11] “The Quantum Threat to Blockchains — 2026 Report,” Project Eleven, 2026. https://www.projecteleven.com/blog/the-quantum-threat-to-blockchains—2026-report

[12] “Migration to post-quantum cryptography,” Mastercard, 2025. https://www.mastercard.com/us/en/news-and-trends/Insights/2025/post-quantum-cryptography-white-paper.html

[13] Ibid.

[14] “Shaping The Future Of AI And Quantum In Financial Services,” Oliver Wyman, April 2025. https://www.oliverwyman.com/our-expertise/insights/2025/apr/ai-quantum-technology-transform-financial-services.html

[15] “McKinsey Quantum Technology Monitor 2026: A Commercial Tipping Point,” McKinsey & Company, 2026. https://www.mckinsey.com/capabilities/mckinsey-technology/our-insights/mckinsey-quantum-technology-monitor-2026-a-commercial-tipping-point

[16] “How quantum computing can prevent a two-tier global financial system,” World Economic Forum, January 2026. https://www.weforum.org/stories/2026/01/quantum-divide-two-tier-global-financial-system/

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.