Fintech in Southeast Asia is entering a new chapter with digital banking. This new chapter brings with it the reduction of costs and dependencies. It also attempts to answer the limitations in services that often cause friction in the growth and adoption of fintech platforms. At Insignia, we’ve invested in several fintechs across the region and have seen how consumers are looking for ease and convenience from their banks, while at the same time demanding an ever-widening range of offerings from fintechs.

Recently, through TONIK Bank, the region’s first fully-fledged digital bank in the region, we’re investing in a fintech play that aims to do both. To better understand the undercurrents that brought this model into fruition, this piece runs through the evolution of the fintech model over the past decade and how it has led to TONIK’s approach.

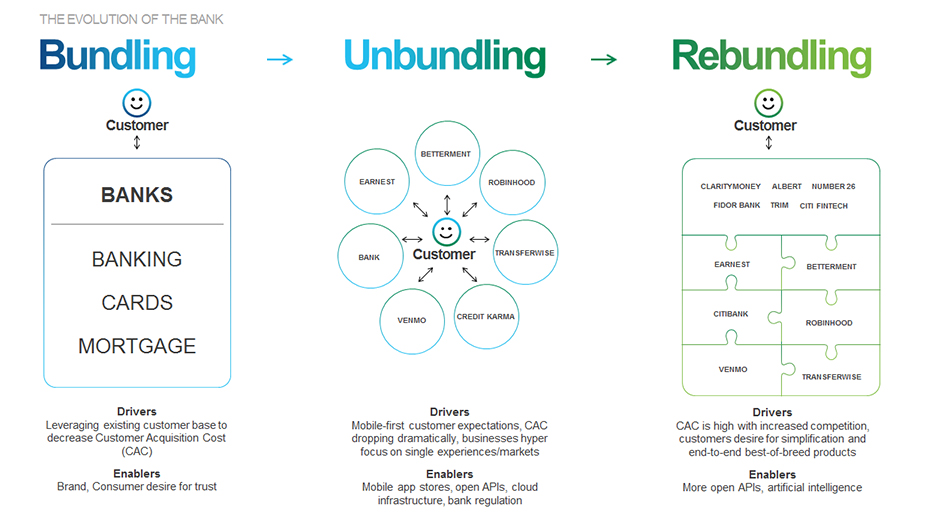

Unbundling: Delivering a better customer experience

In 2015, CBInsights published its now famous ‘Unbundling the Bank” picture showing how newly-minted startups were going after brick-and-mortar banking incumbents in the US and around the world.

Unbundling of a Bank. CBInsights. (2015)

The thesis could be summarized simply: a large number of consumers were growing increasingly dissatisfied with the relationships they had with their banks. Taking a page out of the the digital native playbook that ecommerce giants were offering to change how consumers shopped, the likes of Venmo, Acorns, Wealthfront, Betterment, LendingClub, Funding Circle, Transferwise and Lemonade introduced digital products over the last decade in the US and Europe that enabled consumers to engage in cost-efficient, customer-friendly financial services.

In China, the fintech revolution began earlier, in 2004, when AliPay spun out of Taobao to create a payment system catering first to its own needs and over time to millions of external merchants. AliPay rapidly became the payment network of choice, rivalling Visa, Mastercard, and Union Pay domestically.

These fintechs tackled specific banking services better than traditional banks did. While these “single product” approaches disrupted banking activities across the board, they were limited by the small share of the consumer wallet they could win. The increasing competition within each segment also pushed CAC to unsustainable levels. This threatened the economics of startups relying on an already narrow set of revenue streams. It also placed additional burden on users who had to manage multiple apps and optimize among them.

While “unbundling the bank” helped save consumers time and money, consumers didn’t completely do away with traditional banks. Hungry for growth, fintech players broadened their offerings with one goal in mind: be the figurative and literal consumers’ wallet of choice.

Rebundling: Leveraging on data to become the “wallet of choice”

Acorns’ move to open checking accounts for its clients, Wealthfront’s breakout into lending, and Sofi’s launch of investment and debit accounts are all examples of the more recent rebundling era where fintech startups want their users to consider them as their primary financial services partners.

The Rebundling of the Bank. Citi Ventures. (2017)

AliPay followed a similar strategy. With a high frequency, high volume use case in hand and a wealth of consumer data in its commerce payment product, the company launched its Ant Fortune wealth management platform in 2015 with its now famous Yuebao (余额宝) money market fund. At its peak, Yuebao held more than US $250B in AuM and displaced Fidelity’s and JP Morgan’s money market funds as the largest in the world. Underpinning its product strategy is Sesame Credit, a behavioral credit scoring system based on the consumers’ purchasing history on Alibaba and Alibaba partners’ websites.

The ability to extract credit scoring data from users behaviour on high frequency uses cases (eg payment, ride-hailing) to offer broader product suites is the leverage that a number of other consumer-focused startups used to build up their own financial stack including Southeast Asia’s Grab and Go-Jek. The recent US $1.7B acquisition of Credit Karma by Intuit confirms the treasure trove that represents customer credit data at scale.

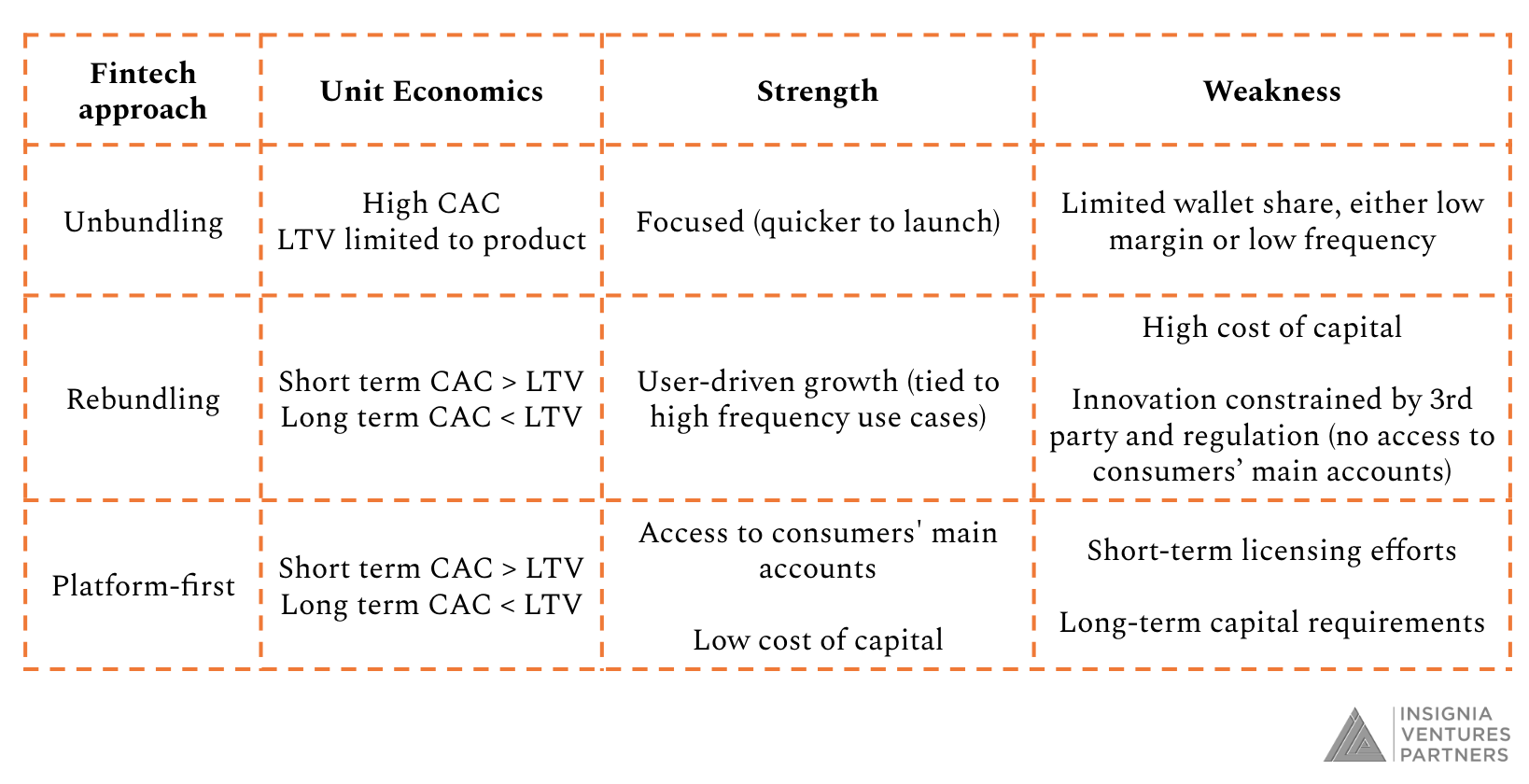

Platform-first: Surpassing the limits on capital and innovation

As with the unbundling approach, the ongoing rebundling efforts of most consumer-focused fintech startups also has its limits. Taking the example of lending startups, which have been prone to jump on the rebundling bandwagon globally, they have had to rely on (expensive) external sources of funding originated from traditional banks, multi-finance companies, credit hedge funds, etc., constraining their margins, especially as compared to banking incumbents. Going to other ancillary services does not solve their fundamental unit economics problem even if it (theoretically) increases their customer LTV.

On the consumer side, while access to credit is a key painpoint for subprime clients in both developed and developing markets, fintech players despite their rebundling efforts have not yet been able to displace traditional banks to access the consumer fintech “holy grail”: checking accounts constraining their ability to finance themselves at lower costs and cross-sell.

In order to break away from these limits, some fintech players are choosing to become fully-fledged banks. In the US, Lending Club acquired Radius Bank, a FDIC-regulated, retail deposit-taking bank, last month. Varo, a digital bank that was relying on 3rd party licensed community banks to acquire depositors, also announced that it became the first fintech in the US to obtain a retail bank charter. In both cases, a cheaper and more stable access to capital as well as the ability to cross-sell and innovate without relying on partners were cited as key decision factors.

The past decade also saw fintechs going platform-first, redefining the bank as a store of value holder. Starting with checking accounts or better yet market-leading savings accounts, neobanks licensed to take retail deposits such as N26, Chime, NuBank, and Monzo catered to different segments of the population from mass-affluent travelers (Revolut/Niyo) to SMEs (Atom/Qonto).

This platform-first approach generates better unit economics than the single-product approach by drastically reducing cost of capital. It also created enough margin to release products covering liabilities aside from pure asset-focused products, catering to a wider range of customer needs.

Comparing fintech approaches. Insignia Ventures Partners. (2020)

Embracing the platform-first approach in Southeast Asia

In Southeast Asia, TONIK Bank is the first to embrace this platform-first approach. Based in the Philippines as the first stand-alone, fully-licensed neobank in the country, the bank will cater to retail consumers across the entire credit spectrum from prime to unbanked segments of the population.

While there has been a lot of coverage recently on Singapore’s efforts to open up the local retail and wholesale banking market to new players, the Philippines was the first country to pull the trigger on the neobank model given how much pent-up demand exists locally.

There are indeed close to 1M mass-affluent households in the country frustrated by their experience with brick-and-mortar local banks (eg slow and analog processing, high fees). More importantly, close to 20M households are currently underbanked or unbanked. For the latter, the frustration over the years manifests in their unsustainable financial situation. Many of them turn to local loan sharks and pawn shops as their only sources of access to credit. TONIK will be offering both segments of the population a clearly differentiated proposition on both financing and deposit products.

In TONIK, we are not only backing the future of fintech in the region, we are also backing a fantastic team of industry veterans who have previously launched and scaled emerging market-based banks. We are excited to invest in their vision and energy as they not only deliver on the ease and convenience of banking but also redefine how fintechs leverage on capital and innovation.

Samir Chaibi is a seasoned investment professional whose experience ranges from investment banking to venture capital. He has served as board director on numerous startups across the globe and has also been a founder himself. He now focuses on finding the next big thing in fintech and SaaS in Southeast Asia.

Hit him up for a chat at samir@insignia.vc if you are a founder building a fintech, proptech, or SaaS startup in Southeast Asia!