This article was authored by Insignia Ventures Academy content developer Melissa Aurellia and edited by Paulo Joquino

For Southeast Asia’s venture capital landscape, 2021 has been a turnaround year in terms of momentum amidst the pandemic, marked by record-breaking milestones in funding and valuations, rapidly emerging venture-backed sectors and trends, and an overall growth in the internet economy that has exceeded predictions made previously and has only driven more investors into the region. In this article, we pick five graphs we’ve found interesting from regional ecosystem and industry reports and share our thoughts on what stories these graphs tell us about the past year’s venture capital landscape and the implications for its future.

- More investors are flocking to early-stage while late-stage funding has decreased since 2018.

- While the generation of VC firms founded from 2015 to 2019 have boosted investments, the increasing democratization of early-stage venture investing thickens the competitive landscape even further.

- Across industries, even as ecommerce and fintech continue to be the most heavily funded, emerging sectors like healthtech, edtech, and online platform enablers saw significant traction this year.

- Deal activity increased in the Philippines significantly vis-a-vis other Southeast Asia markets, boosted by government initiatives and incentives.

- Proceeds from IPO exceeded those from trade exits or secondary sales for the first time, the underlying tailwinds of which can potentially shift the value positioning and exit strategies of venture capital in the region.

Early bird catches the worm, but what happens when you have a flock of early birds?

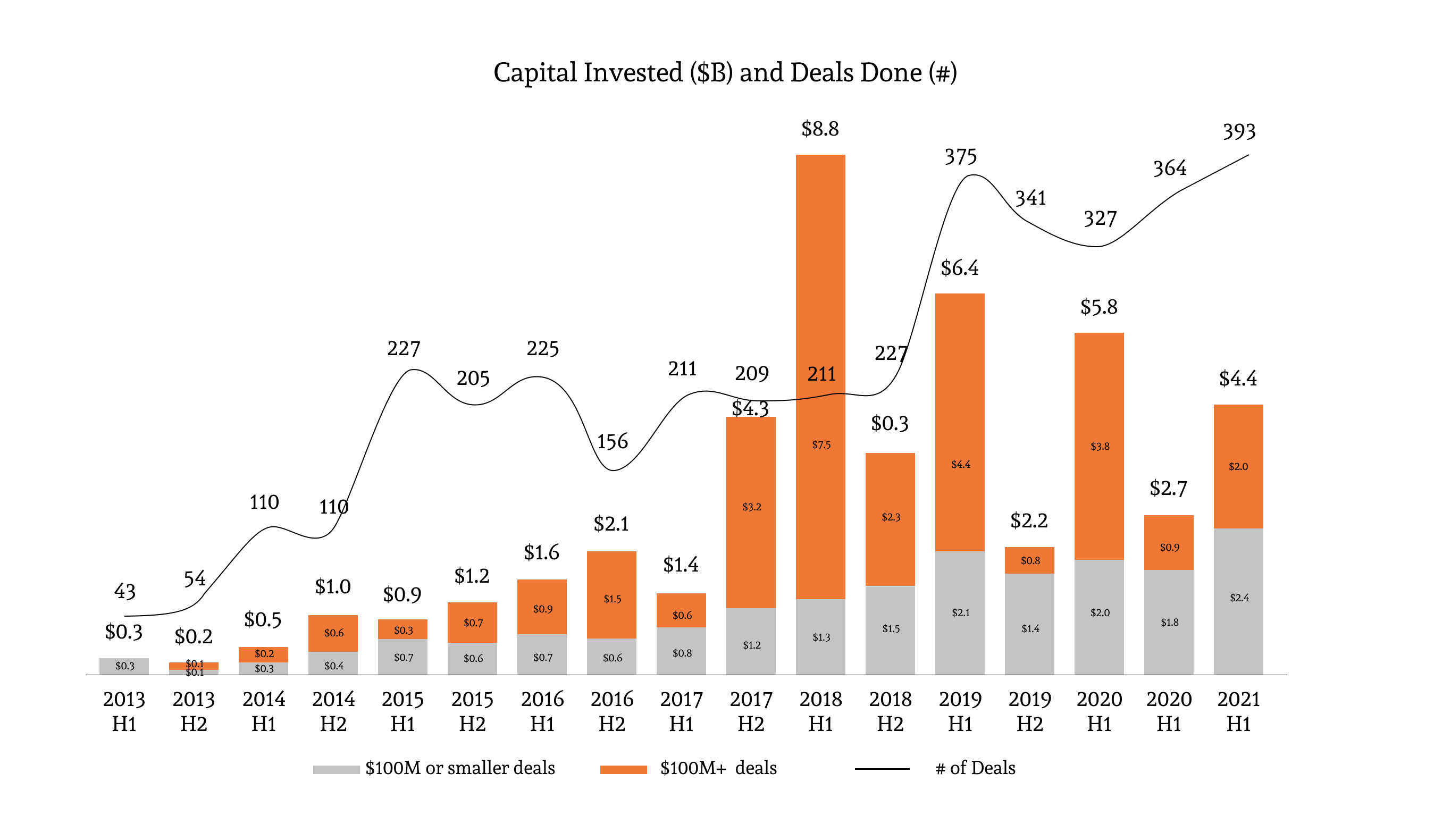

Exhibit 1: Record number of deals done in 2021. Taken from Cento Ventures.

The region saw a record number of deals activity in the first half of 2021, with almost 400 deals done in this time period. However, deals with a value of $100M and more have consistently decreased since reaching a peak the first half of 2018 (remember the time when the discussion was around how long tech companies could stay private and raise megarounds?). On the other hand, the amount of capital invested hit a record high for deals amounting $100M or under, reaching a combined amount of $2.4B altogether. As a result, the total amount invested slid to $4.4B in 2021. This pales in comparison with what investors forked out in the first half of 2018, 2019, and 2020.

Importantly, this signals that investors in the region are increasingly focused on earlier stage funding rounds, a trend we have been writing about over the past two years from different angles: family offices, global investment players, and even angels. It’s a widely accepted principle in venture capital that funding earlier maximizes the chances for investors to get that 100x return. While this is good for the ecosystem, as investments in the early stage companies signals a healthy market and sets the stage for greater growth, investors are now hard-pressed to really set themselves apart from the flock and leverage proprietary relationships. On the other hand, founders are also equally pressured to pick the right investors.

The (venture capital) grass is getting greener in Southeast Asia

Exhibit 2: Proceeds from IPO exceeded trade exit and secondary sales in H1 2021. Taken from Tech in Asia.

So who’s behind the record-high number of deals done in 2021? Sources of capital in the region are becoming more diverse as both global and local investors look to Southeast Asia. The global democratization of capital has allowed all kinds of investors from family offices to angel investors to participate in funding the future.

Starting from 2013, we see the number of new VC firms based in Southeast Asia constantly increasing. A majority of them were set up in Singapore, where the robust ecosystem is supported by government regulations (financing schemes, cash grants, tax incentives, etc.) as well as private sources of funding from high net worth individuals based in the city state.

A growing number of family offices in Southeast Asia is also pouring money into the ecosystem. In SIngapore alone, the number of family offices increased fivefold between 2017 to 2019, and more than 230 family offices have been set up since 2020. Similar trends can be seen across countries in the region. Recently on our podcast, we talked to Mark Sng, Vice President of Gentree Fund about setting up a VC fund for the Sy family office in the Philippines.

Besides your VC firms and family offices, the list also includes angel investors. Increasingly however, we see more founders, the very people who come to VCs for investments, investing in their peers’ startups. We see multiple funds especially in Indonesia which have been formed by founders of successful startups bringing in other startup founders to invest as well.

With all these characters pouring money into the ecosystem, investing is now much more competitive and happens at a rapid pace in order to not lose out on deals. But that’s not all. Given that funding is easily available, investors need to think about why startups should work with them. As Mark Sng shares on the On Call with Insignia podcast, “If everyone’s money is as green as everyone else’s, really what value do you bring to the startup founder?”

Thank you ecommerce and fintech, what’s next

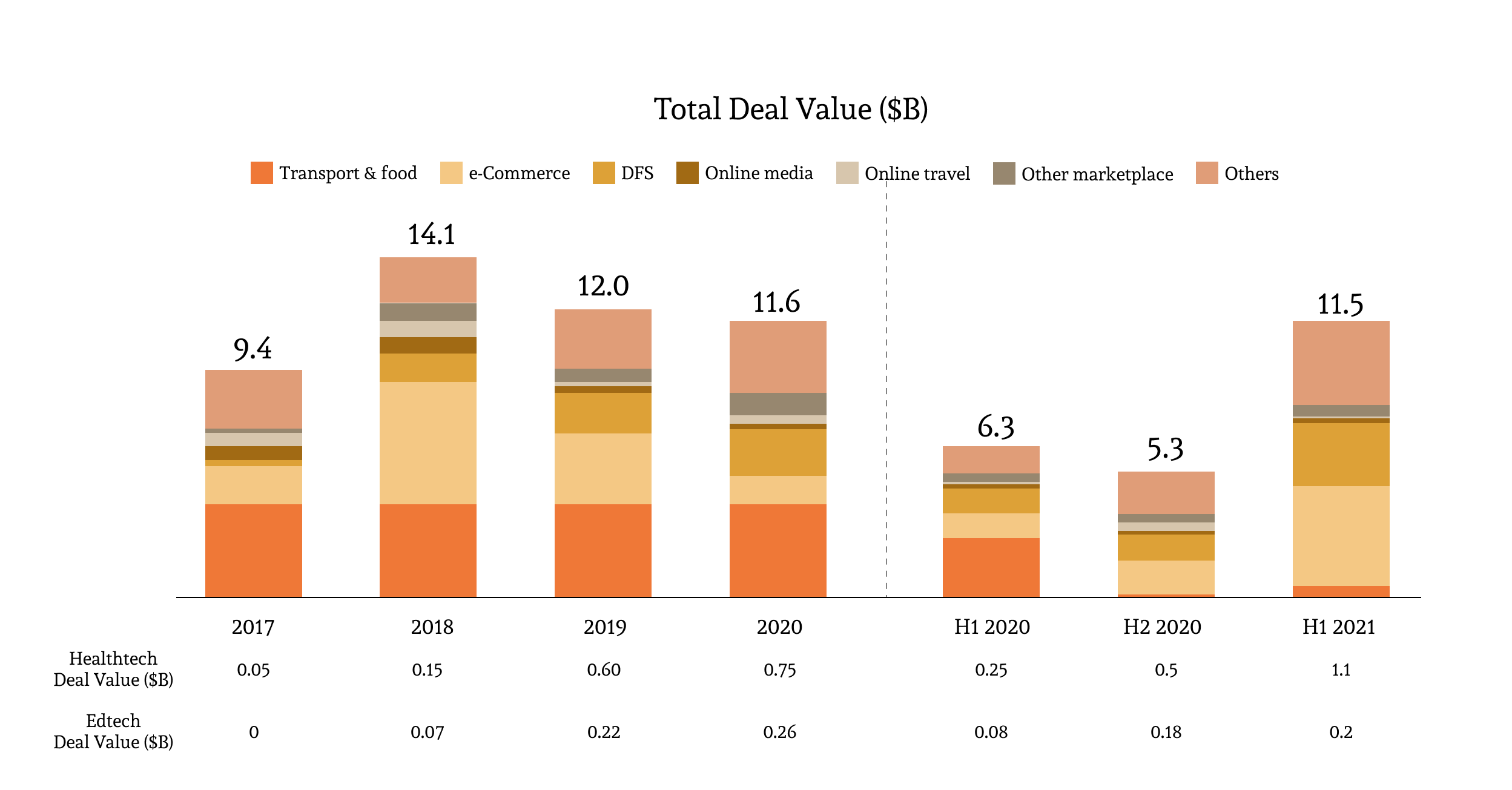

Exhibit 3: The ecommerce and fintech sector still receive the most funding, but healthcare and edtech also show a significant increase in funding from previous years. Taken from eConomy SEA 2021.

Which sectors are these investors putting their money in? This year, ecommerce and fintech continue to be the top 2 startup verticals receiving the most funding. At the end of 2020, we saw three specific verticals dominate the startup ecosystem; transport and food, ecommerce, and financial technology startups. A year on, post-pandemic investment opportunities have changed slightly. Although ecommerce and fintech continue to receive the majority of investors’ capital, verticals like health tech and edtech are receiving more attention against the backdrop of the pandemic.

In the ecommerce sector, a majority of investments are given to logistic players, followed by marketplaces. As marketplaces in the region mature, naturally companies that support the growth of these marketplaces, such as logistics, continue to attract funding in the region. The logistics sector saw a strong increase in funding–almost double–from 2020 to the first half of 2021. Among these is Indonesia’s logistics tech company Shipper that just secured $63M in a Series B round earlier this year.

In fintech, payments and lending continue to receive the majority of investors’ funds from late 2019. However, in the first half of 2021 we see a new category in fintech that began to emerge. Deals received by investment platforms saw a 400% increase from the same period in 2020 to 2021, mainly driven by large deals, among them Ajaib’s series A and unicorn round this year. Apart from the consumer-facing apps, moving forward, we expect to see more funding going towards enablers working behind the scene such as regtech to improve security and trust in financial services as well as fintech infrastructure platforms that enable more online platforms to offer financial services and access financial data through APIs.

Ecommerce and fintech have always been the main character of Southeast Asia’s startup landscape, but this year we saw two verticals stealing the spotlight: healthtech and edtech. In healthtech alone, the funding received in the first half of 2021 already surpassed those made in the whole year of 2020. Customers’ increased spending in health and more trust in digital platforms (largely forced by the pandemic) helped to boost the adoption of health tech platforms in the region. Investors’ confidence in health tech is evident, and Insignia is no exception with three healthcare investments made just this year across different subsectors: mental health with Intellect, femhealth with Ease, and Vietnamese healthcare with Medici.

In the first half of 2021, the edtech sector also saw a slight increase in funding compared to the second half of the previous year. The pandemic highlighted the problem of unequal access to education in the region, but also accelerated the adoption of digital technology in education. Currently, most edtech deals are still in early stages, with early stage deal count representing 83% of total deals.

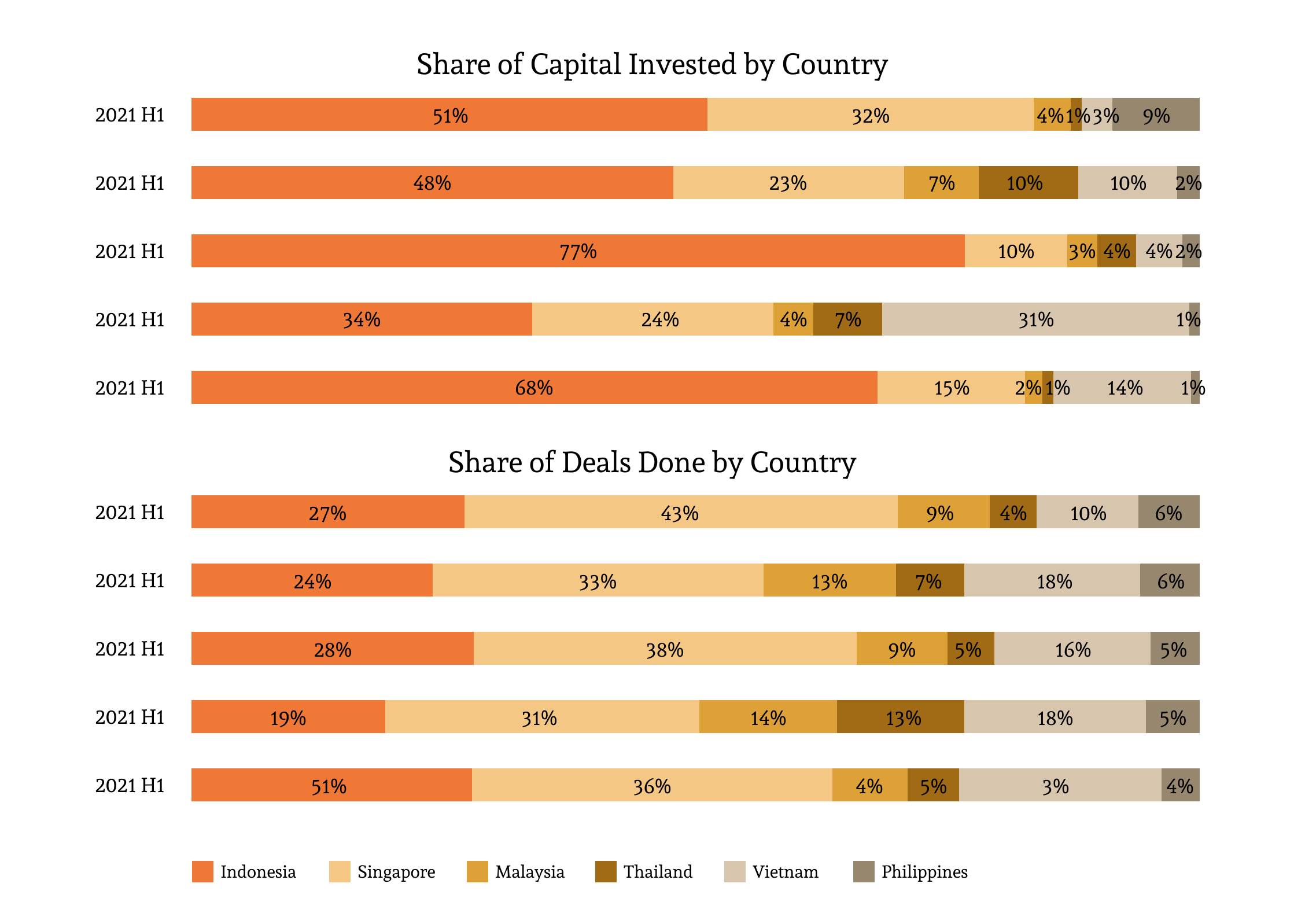

The Philippines breaks its “curse”

Exhibit 4: While Indonesia and Singapore remain the top 2 countries receiving a significant flow of capital, the Philippines began to catch up in 2021. Taken from Cento Ventures.

It’s no news that Singapore and Indonesia are hotspots for startups, and naturally these two countries will represent the majority share of capital invested and highest number of deals done in Southeast Asia. Interestingly, in 2021, we saw Philippines gaining quite significantly in terms of share of capital invested by country, while Thailand and Vietnam’s share went down from the previous years.

The Philippines startup ecosystem is rapidly growing with stronger government support, especially in high-growth services, such as AI, Big Data, and fintech. After introducing the Innovative Startup Act early this year to boost the country’s entrepreneurship ecosystem, the government followed up with launching a National AI Roadmap, making the Philippines one of the first 50 countries in the world to have a national strategy and policy on AI. With over 700 startups operating in the country as of 2021, the Philippine startup ecosystem has seen a 29% compound annual growth rate in the last four years.

Before 2021, the highest funding stage a Philippine startup has ever reached was a Series A. However, this “curse” has been broken thanks to Kumu’s series B and C funding rounds as well as Great Deals and GrowSari’s series B.

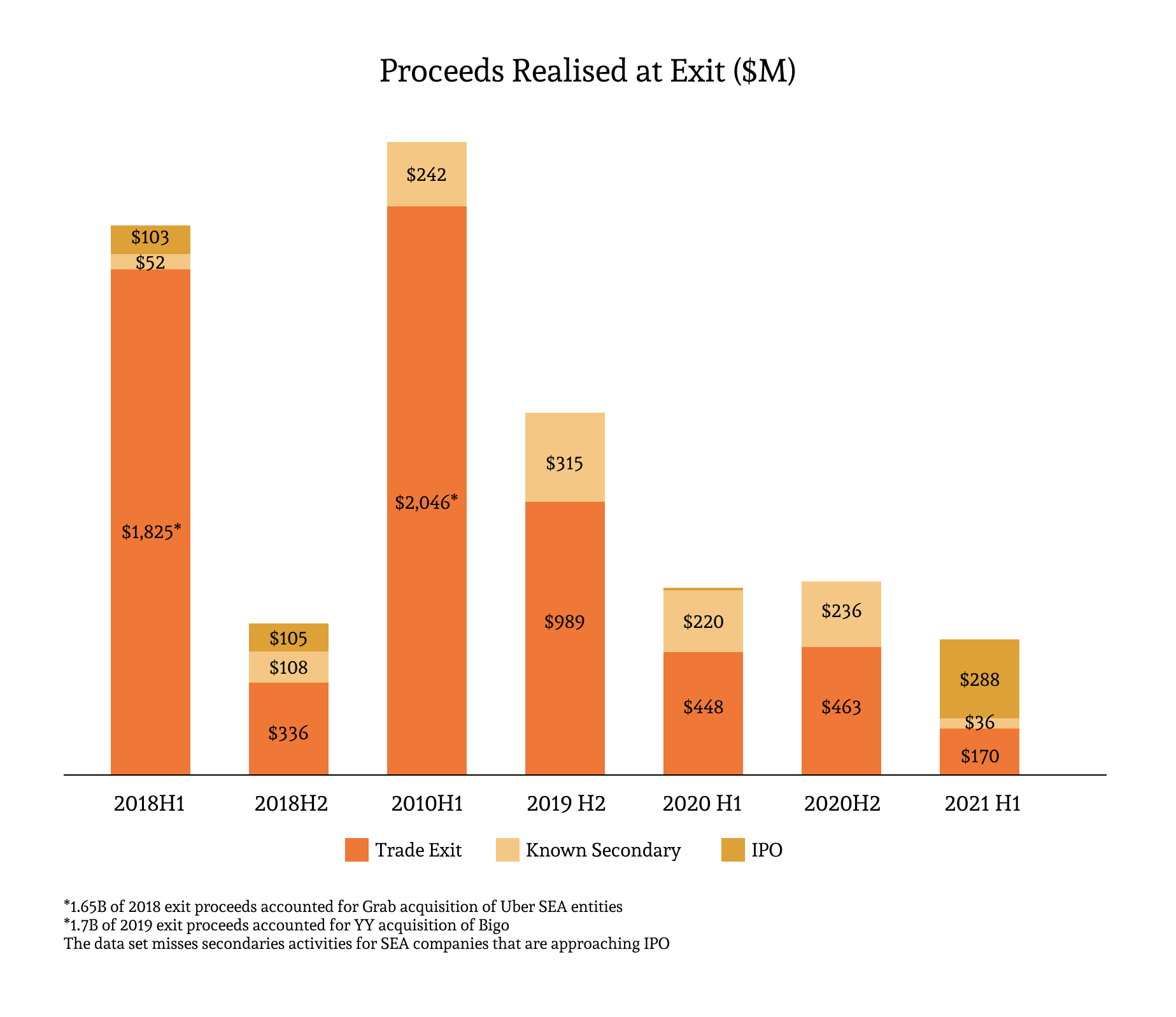

Going public takes time, but is it the best option for liquidity exposure?

Exhibit 5: Proceeds from IPO exceeded trade exit and secondary sales in H1 2021. Taken from Cento Ventures.

In 2021, proceeds from exit through initial public offerings exceeded those from trade exits or secondary sales for the first time. One of the notable exits this year is Bukalapak as they became the first Indonesian listed tech unicorn with a valuation of $7.5B USD.

In the following year, more than 15 startups in Southeast Asia are looking to go public, with many targeting to list in the US, following the success of Sea Group’s NYSE listing. Although many are considering to list through a regular IPO, several leading tech startups such as Traveloka and GoTo–an entity formed from the merger of Gojek and Tokopedia–have publicly announced plans to list via a SPAC. This development over the past two years stands in contrast to 2018 where the discussions and headlines revolved around staying private for as long as possible.

That said, this generation of public market entries may be succeeded by a potential resumption of the “drought” in these types of exits given the time it takes to takes to get a startup from zero to public market ready, though this time around it may be a lot shorter with valuation markups, more mature founders learning from earlier players, and more incentives and avenues for younger companies to seek liquidity in the public markets. It is also worth noting that not all tech companies that look to go public may depend as much on venture-backing and take a route similar to that of Sea Group, raising from family offices and private equity, getting into profitability and going public early.

Two other global tailwinds potentially impacting this trend moving forward in the next decade are (1) the rising adoption of increased liquidity exposure for investors through token investing or crypto funds, and the (2) emergence of open-ended funds for venture capital, both of which will impact the way early-stage startup investors view exits. Though the impact of these tailwinds on this graph in particular may be marginal at best in Southeast Asia, given how much of a spotlight the region is taking up globally at least over the past year, changes made by global investors will impact the region more than before.

And when seasons change, will you stand by SEA?

It’s clear from all the graphs we’ve gone through that 2021 has been a landmark year for Southeast Asia’s startup and venture capital ecosystem. But a less obvious commonality is that fluctuations are very much present in spite of the overall positive trends. This points to the bigger reality that markets ultimately move in cycles. What’s more is that many of the trends in Southeast Asia’s investment landscape are built on investments made rather than actual returns, so there is still a lot of growth that has yet to truly prove itself to be valuable for the region’s venture capital industry. The question for the many founders and investors is how to endure and thrive with the changes in seasons as the region matures and competition thickens. Rather than being complacent with the momentum, now is the time to build strong foundations and fundamentals, whether that means implementing sustainable business models or thinking about long-term differentiation as investors beyond the term sheet valuations.

If you’re looking to understand the foundations and fundamentals of what it takes to thrive in or tap into Southeast Asia’s venture capital ecosystem, be it as a founder, operator, angel investor, or aspiring VC professional, Insignia Academy is now open for applications to its 3rd Cohort this coming March!