Most emerging-market B2C fintechs are not businesses yet. They are user acquisition campaigns waiting for someone else to monetize them.

For over a decade, the B2C fintech industry confused scale with viability. It onboarded billions of wallet customers, celebrated “users,” and produced almost no profit. As of 2026, more than three quarters of neobanks globally are still unprofitable. That is not a market-timing problem. It is a business model problem.

I have spent six years building a credit-led digital bank in the Philippines. The thesis I started with in 2020 has only become more obvious since. What has changed is that the rest of the industry has stopped arguing with it.

“For me, the most interesting business model is actually an asset-liability model. True monetization for a bank is through loans. And I think the emerging markets opportunity is very, very compelling.”— Greg Krasnov, On Call with Insignia, July 2020

Why now

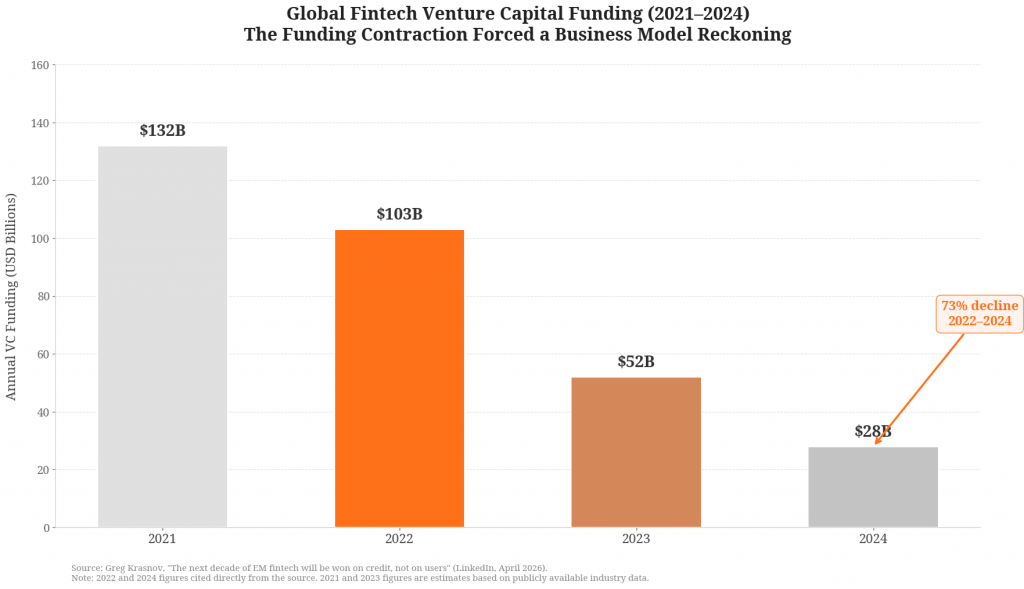

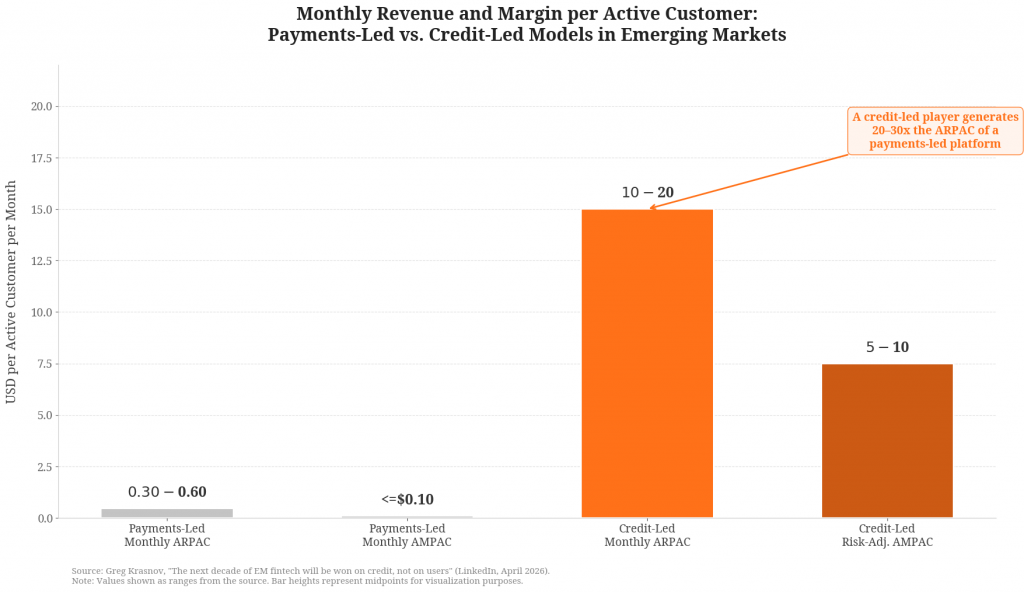

The 2022–2024 funding contraction did the work no investor memo could. Global fintech VC funding fell from $103B in 2022 to $28B in 2024 — a 73% collapse. Capital reallocated into a smaller number of larger checks, written into models that produce real net interest income rather than thin interchange. In that environment, the math became hard to ignore: payment-led platforms generate monthly ARPAC of $0.3-$0.6 and AMPAC of $0.1 or less on most lanes. At the same time, EM consumer lending yields typical ARPAC of $10-20, and if risk is managed well – $5-10 risk-adjusted AMPAC. You can scale a wallet to nine figures of users and still not earn enough per user to fund the cost of acquiring them. You cannot say the same about a loan book.

The validation is clear from the numbers of the players investors actually copy. Nubank’s FY2024 net income nearly doubled to $2B, driven by a lending portfolio that grew 110% YoY. Capitec posted a 29% ROE on unsecured retail credit. Revolut only turned profitable after diversifying away from pure payments toward premium subscriptions and interest income. The pattern is identical across geographies: payments are the door, credit is the house.

The clearest tell is the pivot. GCash, the dominant Philippine wallet at 94M users, took $393M from MUFG at a $5B valuation — and the rationale, written into the press release, was the “vast pool of untapped customers” outside traditional banking. That is not a payments thesis. That is a credit thesis bought by a Japanese megabank. Maya, the other large mobile wallet, posted its first full year of profitability only in 2025 after an explicit pivot into digital banking and credit. Grab Financial’s loans disbursed hit $3.2B in 2025, up 47% YoY. M-Pesa’s Fuliza overdraft now processes more lending volume than the original wallet processes payments.

When the payment-led incumbents are starting to deploy your model, that is not competition. It is confirmation. They are still payments-led, so lending will help them but continue to handicap them with low ARPAC, low loan-deposit ratio, problematic credit risk, and structurally low LTV/CAC.

“Back then, the market was valuing neobanks as a price to user. And I’m a bit of an old-school guy, right? So I believe that a bank should be profitable and the bank should be selling profitable products as a starting point, and you don’t scale it out until you’ve achieved that… a business is there for profit, not for massive market share capture as the main assumption.”— Greg Krasnov, On Call with Insignia, September 2023

Why credit-led

The structural argument has three legs.

First, the underbanked are a credit problem, not a payments problem. Roughly 290M adults in Southeast Asia are unbanked. The personal-loan funding gap in the region is estimated at $100B+; the SME gap, $300B+. Onboarding solves visibility. It does not solve the cash-flow problem in a household that has never had access to a bank loan or credit card. For the payments-led players, this results in an LTV/CAC issue. Acquiring a customer for payments in an EM does not make that customer credit-ready – the resultant low conversion into credit hits unit CAC hard on implied “monetizable” credit client. And makes the payments-led model impossible to sustain on its own in an EM.

“In a country the size of the Philippines, with 110 million-plus population, only to have like a couple of million records in the credit bureau. It’s ridiculous. To us that represents this tremendous opportunity for people who haven’t borrowed before or are new to credit, and who are completely ignored by banks today.”— Greg Krasnov, On Call with Insignia, March 2022

Second, interchange economics cannot fund credit risk for thin-file borrowers. Cost of risk in unsecured EM consumer lending typically runs 10%+. Interchange of 0.5–2% — already compressed further by regulatory pressure and dominance of QR payments instead of “juicy” card payments — cannot pay for credit losses, underwriting infrastructure, and the capital cost of a loan book. A payment-led player needs ten to twenty times the transaction volume to match the unit revenue of a single consumer loan at 25–40% APR. Most never get there.

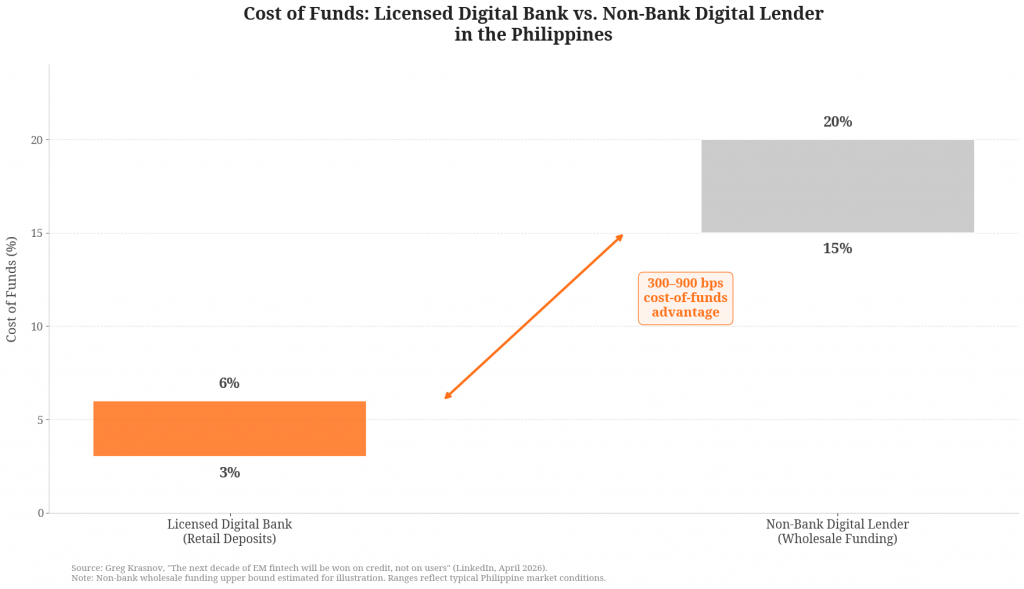

Third, the funding source determines the floor. Non-bank digital lenders fund themselves wholesale at 15%+ in the Philippines. A licensed digital bank funds itself through retail deposits at 3–6%. That is a 300–900 bps cost-of-funds advantage, compounding every quarter. It is the difference between a business that scales profitably and one that scales until the wholesale window closes.

“If you want to scale your balance sheet into the billions of dollars — which is what the Philippines needs — you need deposits. And the only way to take deposits is to have a banking license. That’s what led me to approach the central bank and say, ‘Guys, can you give me a license to both collect deposits digitally and lend digitally?’ Because it’s only by connecting those two that we can truly build proper credit access in this country.”— Greg Krasnov, Against All Odds, March 2025

Capitec, KreditBee, Creditas, and Nubank are not exceptions to a pattern. They are THE pattern. Each began with credit at the core, used scale to bring deposit costs down, and built the rest of the bank around the loan book — never the other way around.

Why Southeast Asia, and the Philippines specifically

The Philippines is the cleanest expression of the thesis anywhere in Asia.

Total household debt sits at roughly 13% of GDP — the lowest in ASEAN, against 88% in Thailand and 84% in Malaysia. Consumer lending is growing above 21% YoY off that base. Roughly 44% of Filipinos remain unbanked or underserved. Mobile penetration is near saturation. The forward growth runway is not a quarter or a year. It is a decade of compounding credit penetration from a near-zero base, in a market that already has the digital infrastructure to absorb it. And it represents over $50B of dormant annual revenue TAM on the “blue ocean” mass-market clients currently ignored by traditional bank lenders.

“I think the Philippines is at a real inflection point in terms of middle-class development. And it’s a very exciting time to be here. This is actually why we’re here, because one of the key things about the development of the middle class is you get this kind of explosion of consumer lending, which hasn’t happened in the Philippines yet. We’re at the very beginning of this.”— Greg Krasnov, On Call with Insignia, November 2025

The regulatory architecture is the second piece, and it is not incidental. BSP Circular 1105 created digital banks as a distinct license class in late 2020, capped initial licenses at six, and held a moratorium on new entrants until January 2025. Even now, only four additional licenses are available, and the BSP has signalled it will be selective. The license is not a checkbox — it is what gives a credit-led player access to retail deposit funding rather than wholesale capital. And with the bank deposit market of $300B+ sitting in the traditional banks at 0.5-1.0% interest rate – the scalability and low cost of deposit-driven funding is what will separate long-term winners from losers in this market.

The third piece is capital flow. Japanese institutions — e.g. MUFG investment into GCash and Home Credit, Mizuho investment in Tonik, Tokyo Stock Exchange opening an Asia Startup Hub that includes Tonik as the first Philippine company — are systematically allocating into SEA financial inclusion. The reason is not sentimental. Japan has excess capital, low domestic yields, and an aging demographic. SEA has the credit gap Japan no longer has at home.

The Philippines, in other words, has the lowest credit base, the strongest license moat, and the most receptive strategic capital pool in the region. That is a rare configuration.

Why Tonik

I will be brief here, because the thesis should do most of the work.

The winners of the credit-led EM digital bank model need to deliver two main “unlocks.” First – profitable lending. Credit risk in the EM “blue ocean” mass market is very very high. Learning how to manage it to deliver a positive RAROC takes lots of learning, expertise, and time. Secondly – scalability of funding base = deposit market access through a digital bank license.

“We went quite quickly to introduce the products to the market, but then to operate at unit profitability on unsecured consumer loans, it takes time. Because basically, you need to train your credit system. And you need data; you need performance data in order to train that.”— Greg Krasnov, On Call with Insignia, September 2023

Tonik is the only digital bank in the Philippines built credit-first from day one, i.e. focused on delivering these two “unlocks.” We hold the first BSP digital banking license. The credit portfolio is now over $100M with a 27% RAROC, an 88% loan-to-deposit ratio, and 2.3x year-on-year loan growth. ARR is at $60M+. We turned contribution-margin positive in Q1 2025 and cash flow breakeven in Q1 2026, among the fastest breakeven curve of any non-ecosystem captive digital bank worldwide. And most importantly – we are the only player cleanly positioned with BOTH unlocks into the $50B dormant TAM.

Our backers — Insignia, Mizuho, Peak XV, Point72 — share a single thesis with us: that the right place to build a durable EM fintech is where credit penetration is lowest, regulatory protection is highest, and the funding base is local and deposit-based.

We were never designed to be the largest digital bank in the Philippines. We were designed to be the most capital-efficient one.

Closing thesis

The next decade of emerging-market fintech will not be won by the platforms with the most users. It will be won by the ones that can underwrite them. Payments were the entry strategy of the last cycle. Credit is the business model of this one. Everything else — wallets, super-apps, ecosystems — is a customer acquisition layer in search of a P&L.

That is the argument. I would rather be wrong about it in public than vaguely right about it in private.

References

Krasnov, Greg. “The next decade of EM fintech will be won on credit, not on users.” LinkedIn. 04/27/2026. https://www.linkedin.com/pulse/next-decade-em-fintech-won-credit-users-greg-krasnov-ixsrc/

On Call with Insignia. “Building Southeast Asia’s first digital-only bank in the Philippines with Tonik CEO and Founder Greg Krasnov”. Insignia Business Review. 07/16/2020. https://review.insignia.vc/2020/07/16/building-southeast-asias-first-digital-only-bank-in-the-philippines-with-tonik-ceo-and-founder-greg-krasnov/

On Call with Insignia. “Tonik CEO Greg Krasnov shares the 6Ps of neobanks and leading the Philippines’ consumer banking revolution”. Insignia Business Review. 03/14/2022. https://review.insignia.vc/2022/03/14/season-4-episode-4-tonik-ceo-founder-greg-krasnov-6ps-of-neobanks-leading-philippines-consumer-banking-revolution/

On Call with Insignia. “Call 139: How this Philippine digital bank views growth, from loans to AI with Tonik CEO Greg Krasnov”. Insignia Business Review. 09/26/2023. https://review.insignia.vc/2023/09/26/season-5-episode-28-call-139-tonik-digital-bank-philippines-greg-krasnov/

On Call with Insignia. “Call 140: How to unlock the ‘holy grail’ of Philippine digital banking with Tonik CEO Greg Krasnov”. Insignia Business Review. 09/26/2023. https://review.insignia.vc/2023/09/26/season-5-episode-29-call-140-tonik-digital-bank-philippines-greg-krasnov/

Joquino, Paulo. “The Banker who brought Digital Banking to the Philippines | Against All Odds with Tonik CEO and Founder”. Insignia Business Review. 03/10/2025. https://review.insignia.vc/2025/03/10/banker-tonik-greg-krasnov/

On Call with Insignia. “Tonik CEO and founder Greg Krasnov gets the tea on Japan IPOs from Tokyo Stock Exchange APAC Deputy Head Beomsu Son”. Insignia Business Review. 11/11/2025. https://review.insignia.vc/2025/11/11/tonik-tse/

As the Founder of Tonik (www.tonikbank.com), the first neobank in the Philippines, I'm committed to building a trustworthy and simple banking experience to drive financial inclusion in the Philippines, where the majority of the population remains without bank accounts and without access to formal credit. I am a serial entrepreneur, having previously launched and led/co-led fintech companies FORUM, Credolab, FLOW, AsiaKredit, and Platinum Bank. Ever since starting my first business at 17, I've been passionate about entrepreneurship and problem-solving.

I appreciate that in life one needs to have balance. During a two-year sabbatical, I skippered my sailboat SV Blues across Asia. I'm also a musician (check me out on Spotify). And as a resident of eight countries across three continents, and a founder of YPO's Kyiv Chapter I've gained a unique understanding of diverse cultures and perspectives.

Throughout my career, I've received many accolades that I'm proud of, but what truly matters to me at this stage is the impact I make on people's lives through my managerial and creative problem solving skills. I'm a "what you see is what you get" kind of guy who values honesty and open communication. I believe in fostering genuine connections and staying true to my principles, both personally and professionally.