The race to build the trust layer for autonomous commerce is on. Southeast Asia, with its regulatory diversity, fraud exposure, and digital identity infrastructure, is uniquely positioned to lead it.

The rapid emergence of agentic commerce — where AI agents autonomously discover products, negotiate terms, and execute transactions — promises to unlock trillions in economic value [1]. However, the foundational layer of trust, distinguishing legitimate AI agents from malicious bots, remains the most critical and underdeveloped component of this stack. While global protocols establish technical interoperability between agents, the widespread adoption and scalability of agentic commerce hinge on robust Know Your Agent (KYA) frameworks.

This article argues that KYA, analogous to KYC for individuals, is not merely a regulatory necessity but a strategic imperative. For Southeast Asia — a region characterized by diverse regulatory landscapes and a high prevalence of digital fraud [2] — developing and implementing localized KYA solutions presents a significant investment opportunity and a crucial pathway to securing leadership in the autonomous future of commerce.

The Agentic Revolution: A Double-Edged Sword

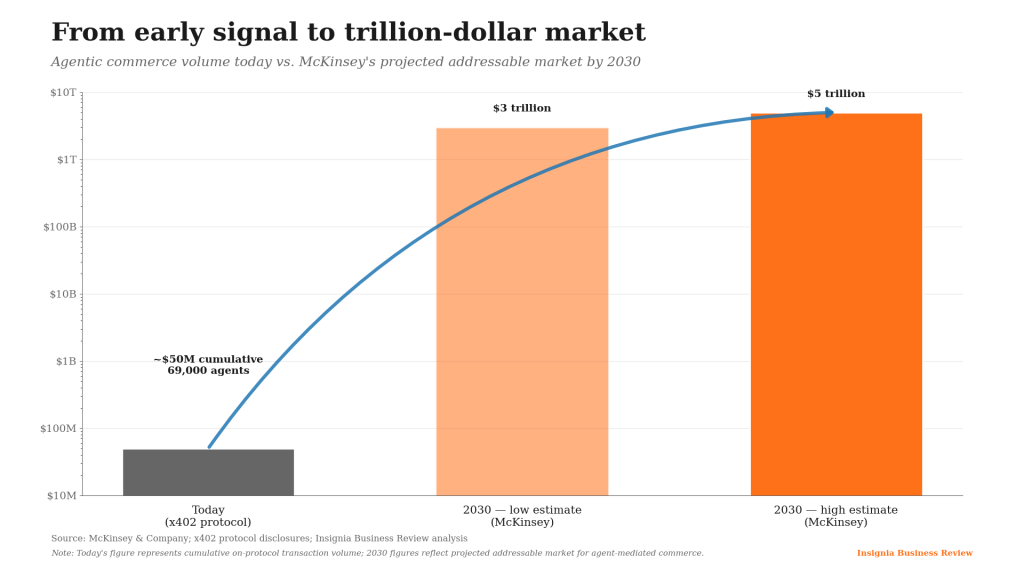

The vision of agentic commerce is compelling: AI agents discovering optimal products, negotiating prices, and executing payments on behalf of users, seamlessly and efficiently. As highlighted in our previous analysis on Insignia Business Review, protocols like x402 are already processing live transactions, signaling a tangible shift from theory to practice [3]. McKinsey’s projection of a $3–5 trillion agentic commerce market by 2030 underscores the immense economic potential [1].

However, this autonomy introduces a profound challenge: trust. In a world where transactions are increasingly automated, how do merchants, platforms, and even other agents verify the legitimacy and intent of their autonomous counterparts? The very efficiency that makes agentic commerce attractive also creates new vectors for fraud, manipulation, and illicit activity if not properly governed. The current state — roughly 69,000 agents processing approximately $50 million in cumulative transactions on x402 [3] — is an early, relatively low-risk environment. Scaling that volume to trillions demands a robust, verifiable trust layer.

From early signal to trillion-dollar market

Agentic commerce volume today vs. McKinsey’s projected addressable market by 2030

Source: McKinsey & Company; x402 protocol disclosures; Insignia Business Review analysis

The Trust Bottleneck: From Human Identity to Agent Identity

In traditional commerce, Know Your Customer (KYC) and Anti-Money Laundering (AML) frameworks are cornerstones of financial integrity. They establish the identity of individuals and entities, mitigating risks of fraud, terrorism financing, and other illicit activities [4]. For agentic commerce to scale, an equivalent — yet structurally more complex — framework is indispensable: Know Your Agent (KYA).

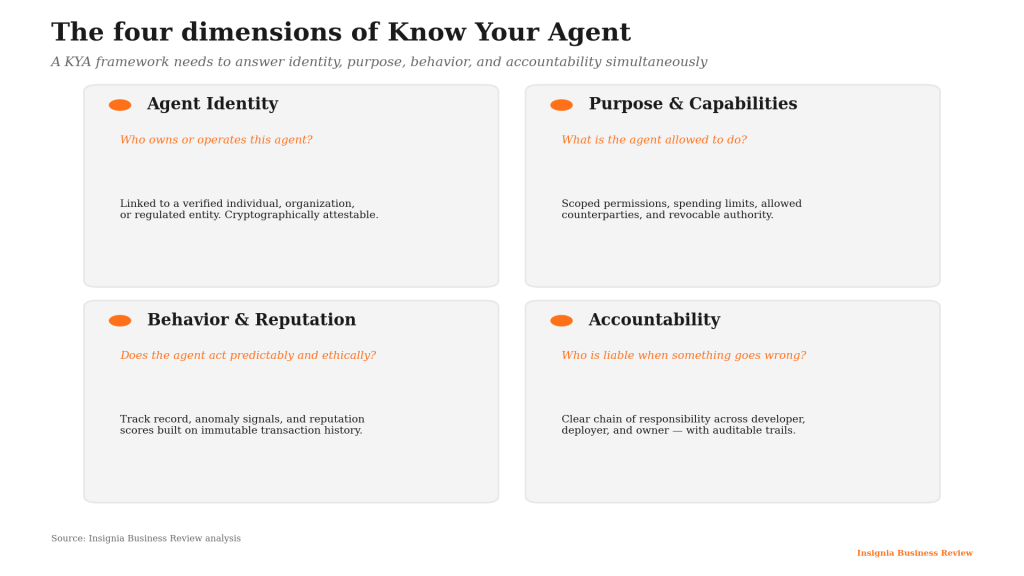

KYA goes beyond merely identifying the human or organization behind an agent. It seeks to answer four distinct questions:

- Agent Identity. Who owns or operates this agent? Is it linked to a verified individual or entity?

- Agent Purpose & Capabilities. What is the agent designed to do? What permissions and spending limits has it been granted?

- Agent Behavior & Reputation. Does the agent act predictably and ethically? Has it been involved in suspicious activity?

- Agent Accountability. Who is responsible if an agent makes an error, breaches a contract, or commits fraud?

This multi-faceted identity challenge is the real bottleneck preventing widespread adoption. Without KYA, merchants face unacceptable counterparty risk, regulators lack oversight, and consumers remain exposed to a class of fraud they cannot easily diagnose or contest.

The four dimensions of Know Your Agent

A KYA framework needs to answer identity, purpose, behavior, and accountability simultaneously

Source: Insignia Business Review analysis

Building the KYA Stack: Components of a Trusted Agentic Ecosystem

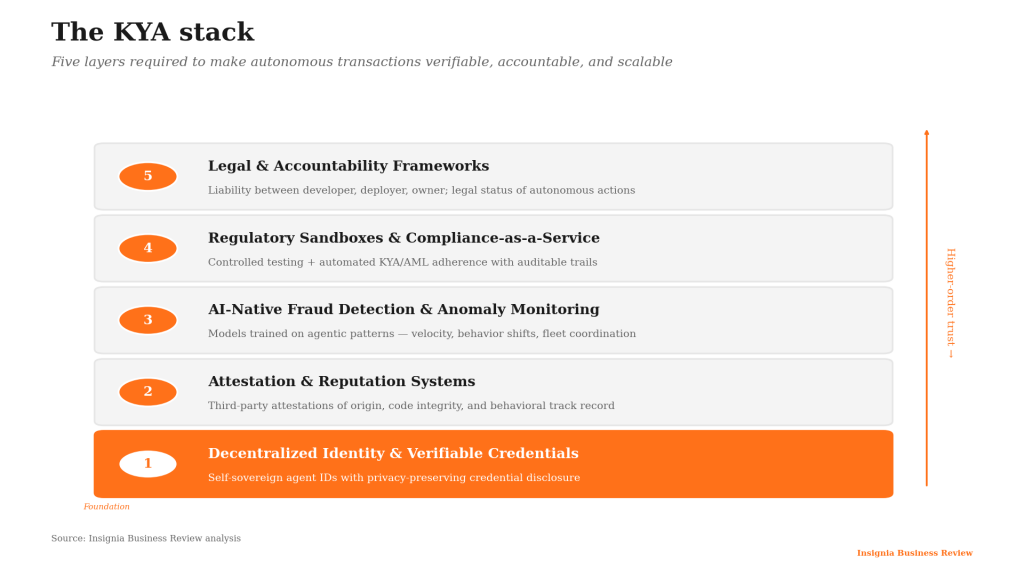

Comprehensive KYA frameworks will require innovation across several layers, none of which exist in production-ready form today.

- Decentralized Identity (DID) and Verifiable Credentials. Leveraging cryptographic identity standards, DIDs can give agents self-sovereign, verifiable identities [5]. This allows an agent to present credentials — for example, “authorized to purchase up to $X” or “verified by Organization Y” — without revealing unnecessary underlying data. This is critical for both privacy and operational efficiency.

- Attestation and Reputation Systems. Trusted third parties — model providers, compliance auditors, and industry consortiums — can attest to an agent’s origin, code integrity, or adherence to ethical guidelines. Reputation systems, built on immutable transaction histories and feedback loops, can then provide a dynamic trust score for agents, similar to seller ratings on e-commerce platforms but designed for machine-to-machine context.

- AI-Native Fraud Detection and Anomaly Monitoring. Traditional fraud detection systems are designed for human behavior. KYA requires AI models specifically trained to identify anomalous patterns in agentic interactions — unusual transaction velocity, sudden behavior shifts, attempts to circumvent established protocols, or coordinated activity across agent fleets.

- Regulatory Sandboxes and Compliance-as-a-Service. Regulators need controlled environments to test KYA solutions in real-world conditions. In parallel, a new class of companies will emerge offering compliance-as-a-service for agents — automating adherence to evolving KYA/AML regulations and producing auditable trails for every autonomous decision.

- Legal and Accountability Frameworks. Defining legal liability for agent actions is paramount. This involves establishing clear lines of responsibility between an agent’s developer, deployer, and owner — and potentially new legal constructs for autonomous agents themselves [6].

The KYA stack

Five layers required to make autonomous transactions verifiable, accountable, and scalable

Source: Insignia Business Review analysis

Southeast Asia’s Unique Position: The KYA Opportunity

Southeast Asia, with its diverse regulatory landscapes, rapidly digitizing economies, and significant exposure to digital fraud, is uniquely positioned to lead in KYA innovation.

The problem: fragmented trust, high fraud risk

The region presents three structural challenges that any agentic infrastructure must contend with.

The first is a regulatory patchwork. Each Southeast Asian country runs its own data privacy laws, financial regulations, and digital identity schemes — Singapore’s Singpass, Indonesia’s NIK, Malaysia’s MyKad, the Philippines’ PhilSys, and others [7]. A unified KYA approach must be adaptable to these variances rather than imposed on top of them.

The second is digital fraud prevalence. The region continues to face persistent challenges with online scams, account takeovers, and synthetic identity fraud, making merchants and consumers inherently cautious about delegating spending decisions to autonomous software [2]. A robust KYA system can be a powerful antidote — but only if it is calibrated to local fraud typologies.

The third is SME adoption. Small and medium-sized enterprises form the backbone of Southeast Asian economies and account for a disproportionate share of new digital commerce volume. Most lack sophisticated fraud-detection tooling. KYA solutions that are accessible, low-friction, and easy to implement for SMEs will be the deciding factor in mass adoption.

The opportunity: building localized KYA solutions

Each of these challenges maps to a category of company that can be built now.

- Leveraging national digital identity. Builders can integrate KYA solutions with existing national digital identity frameworks, providing a strong, government-backed foundation for agent verification.

- Regional compliance hubs. Singapore’s progressive regulatory environment, including the MAS approach to digital assets and tokenization, makes it a natural home for developing and piloting KYA standards that can then be adapted across the region [8].

- Localized AI fraud detection. Companies specializing in machine learning can develop KYA-specific fraud detection models tuned to the unique patterns and languages of fraud prevalent in different Southeast Asian markets.

- Cross-border KYA interoperability. As agentic commerce inevitably crosses borders, the need for KYA solutions that interoperate across national regulatory environments will be paramount. This is simultaneously the largest technical challenge and the largest commercial opportunity for regional infrastructure leaders.

For investors, exposure to companies building KYA infrastructure, identity verification for AI, and specialized fraud prevention for autonomous transactions within Southeast Asia represents a strategic position in the foundational technologies that will underpin the projected $3–5 trillion agentic economy.

Southeast Asia’s KYA opportunity surface

Where regulatory diversity, digital identity infrastructure, and fraud exposure intersect

Source: Insignia Business Review analysis; national digital identity programs

Conclusion: Securing the Autonomous Future

The promise of agentic commerce is immense, but its realization hinges on solving the fundamental problem of trust. Know Your Agent is not a peripheral concern; it is the central pillar upon which a secure, scalable, and compliant agentic economy will be built.

For Southeast Asia, the unique confluence of regulatory diversity, digital fraud exposure, and a vibrant tech ecosystem creates an unparalleled opportunity to innovate in this space. The builders who successfully develop and deploy robust KYA frameworks tailored to the region’s specific needs will not only mitigate risk — they will unlock unprecedented levels of confidence and participation in the agentic future.

This is where the smart capital will flow, enabling the region to transition from merely participating in global agentic commerce to actively defining its trusted and secure evolution. The race to build the KYA layer is on, and Southeast Asia is uniquely positioned to lead.

References

[1] McKinsey & Company. The economic potential of generative AI and autonomous agents — estimates of a $3–5 trillion agentic commerce market by 2030. https://www.mckinsey.com/

[2] Global Anti-Scam Alliance and regional cybersecurity reports on digital fraud prevalence in Southeast Asia. https://www.gasa.org/

[3] x402 protocol activity disclosures and ecosystem updates; companion analysis on agentic payment rails. https://review.insignia.vc/

[4] Financial Action Task Force (FATF). Guidance on Customer Due Diligence (KYC) and Anti-Money Laundering (AML). https://www.fatf-gafi.org/

[5] World Wide Web Consortium (W3C). Decentralized Identifiers (DIDs) v1.0. https://www.w3.org/TR/did-core/

[6] European Commission and OECD working papers on AI liability and accountability frameworks. https://digital-strategy.ec.europa.eu/

[7] National digital identity programs across Southeast Asia: Singpass (Singapore), NIK / Dukcapil (Indonesia), MyKad / MyDigital ID (Malaysia), PhilSys (Philippines), ThaID (Thailand), VNeID (Vietnam).

[8] Monetary Authority of Singapore (MAS). Project Guardian and digital asset regulatory framework. https://www.mas.gov.sg/