Capital is flowing again — but to a narrower set of companies, evaluated on a stricter set of metrics, with a higher bar for governance. The CFO has become the operator who decides whether a Series B reaches a Series C, and more importantly to an IPO / public markets listing.

A repriced ecosystem

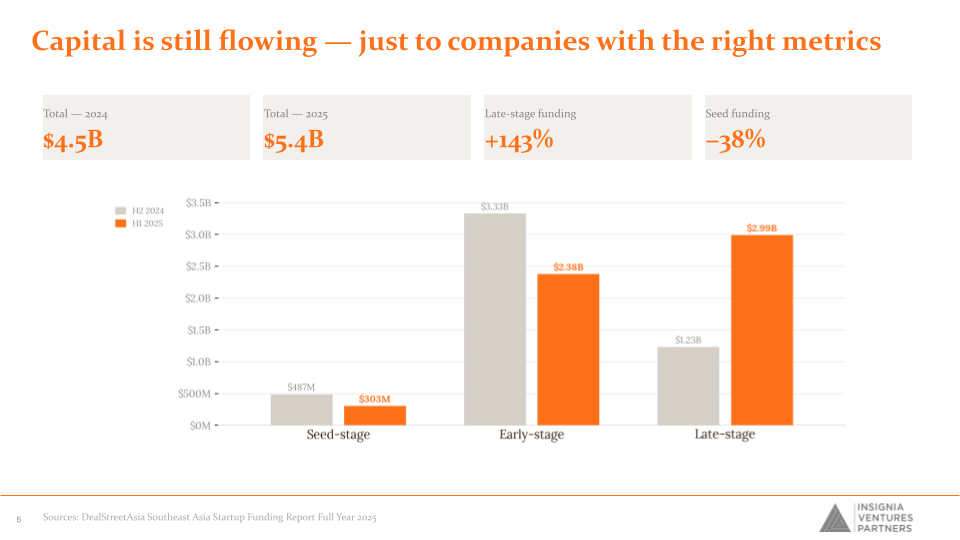

Southeast Asia’s private capital market has stabilised after three years of contraction, but the recovery is bifurcated. The region’s startups raised roughly USD 5.4 billion across 461 equity deals in 2025, up from approximately USD 4.5 billion the year before [1]. The headline number, however, masks a structural shift in where that capital actually went. Late-stage funding rebounded sharply — late-stage transaction volume more than doubled in the second half of 2025 versus the first half, and rose to four new unicorns in 2025 from a single one in 2024 [1]. Seed funding, by contrast, contracted again. The region’s largest deals concentrated at the top of the stack while the bottom of the funnel kept thinning.

The implication for founders and finance leaders is precise. Capital is available, but it is being underwritten differently. Investors are not asking whether a company is growing; they are asking whether it is growing efficiently, whether its revenue is durable, and whether the operator team can be trusted to report what is actually happening inside the business. That last test — once a footnote in diligence packs — has become a primary one.

Southeast Asia equity funding: 2024 vs 2025

Capital is flowing again — but to a narrower set of companies

Capital is here. It has just become far more selective — flowing to companies that have already proven their models, their metrics, and their governance. The CFO role carries a lot of weight in that environment. A strong CFO shapes how a company grows and shares the glory when it works; when the finance function has a gap, the consequences can be serious for the company and for the people involved. The opportunity is real and so is the responsibility.

What follows is a working framework for what “investable” now means in 2026 and how a CFO should operate to clear that bar.

The efficiency-era reset

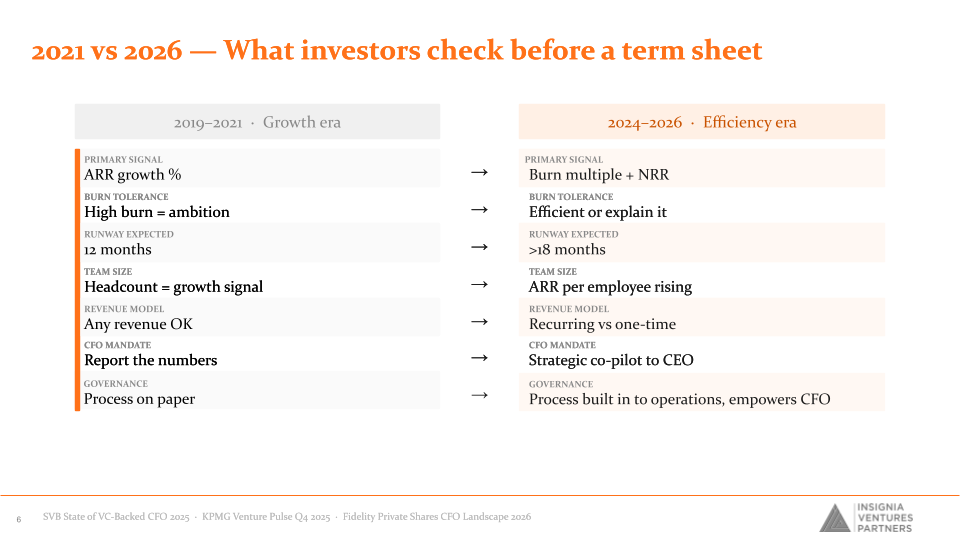

Between 2019 and 2021, growth was its own justification. ARR growth was the primary signal investors looked at, headcount was read as a proxy for ambition, twelve months of runway was a normal cadence between rounds, and the CFO mandate was largely to report numbers and close books. Recurring versus one-time revenue was a useful distinction, but not a deciding one. High burn was a sign that a company was investing into a market opening.

The 2024–2026 window has rewritten every line of that grid [2][3]. The primary signal is now the burn multiple, with a benchmark of 1.5x or lower at growth stage and net revenue retention layered on top. Burn tolerance has flipped — it is no longer a badge of ambition but a number that has to be defended in a memo. SVB’s most recent CFO research finds that companies are now expected to plan around 24 to 30 months of runway minimum, not 18, and that this longer cadence is being maintained even as profitability among VC-backed companies improved across sectors in 2025 [2]. Headcount is no longer a growth indicator on its own; investors look for ARR per employee to be rising. Recurring revenue is now the only revenue model that gets full credit. And the CFO is no longer the scorekeeper; they are expected to function as a strategic co-pilot to the CEO — owning capital efficiency, scenario planning, and the diligence narrative.

There is one more line on the grid that did not exist in this form five years ago: governance. In the growth era, governance was a process on paper — a board calendar, an audit committee charter, a delegation-of-authority matrix filed in a data room. In the efficiency era, governance has to be built into the operating cadence of the company, with the CFO empowered to act independently on it.

What investors check before a term sheet

Same line items, different bar — the 2024–2026 efficiency reset

The Trust Tax

The reason that governance line exists — and the reason it now sits next to burn multiple in the term-sheet checklist — is a sequence of governance failures across the region’s recent vintages that has repriced the ecosystem. The pattern is consistent enough that it is now diligenced as a category, not as one-off cases:

- A post-Series D company where a whistleblower-triggered audit found revenue had been fabricated; the founder was jailed.

- A post-Series B fintech where misuse of funds linked to bad debt led to the ex-CEO being detained and assets seized.

- A post-Series D platform where falsified invoices led to charges against the ex-CEO.

- A post-IPO company where a reporting gap and an audit delay led to trading being suspended.

- A first-day IPO that proceeded after coming in undersubscribed, then failed on listing day and was withdrawn.

The cases differ in stage and detail, but the operator-level failure mode is similar — a finance function that was not independent enough, not well-informed enough, or not resourced enough to push back against management before the disclosure event arrived. When governance breaks down in a handful of companies, the ecosystem pays. Due diligence gets heavier, fundraising becomes more challenging, and the cost of capital re-prices upward across deals that have nothing to do with the original failures. A strong, empowered CFO is one of the best defences against that drift. The aggregate effect is what some analysts have begun calling a “trust tax.” Indonesia, which had been the single largest pool of risk capital in the region, attracted less than USD 80 million in private funding in the first half of 2025, compared with roughly USD 200 million a year earlier — a pullback that the regional e-Conomy report attributed in part to the chilling effect of these failures on investor appetite [4][5]. Capital is not absent from the market; it has simply repriced the risk of being wrong about who is running the company.

A useful framing is that metrics are not everything. A company that hits every quartile benchmark on burn multiple, NRR and Rule of 40 can still be uninvestable if a single CFO-controlled process — bank reconciliation, related-party disclosure, revenue recognition — is not strong enough to survive a confirmatory audit. The role of a strong, independent, and well-informed CFO has become a structural prerequisite for scaling, not an organisational nicety.

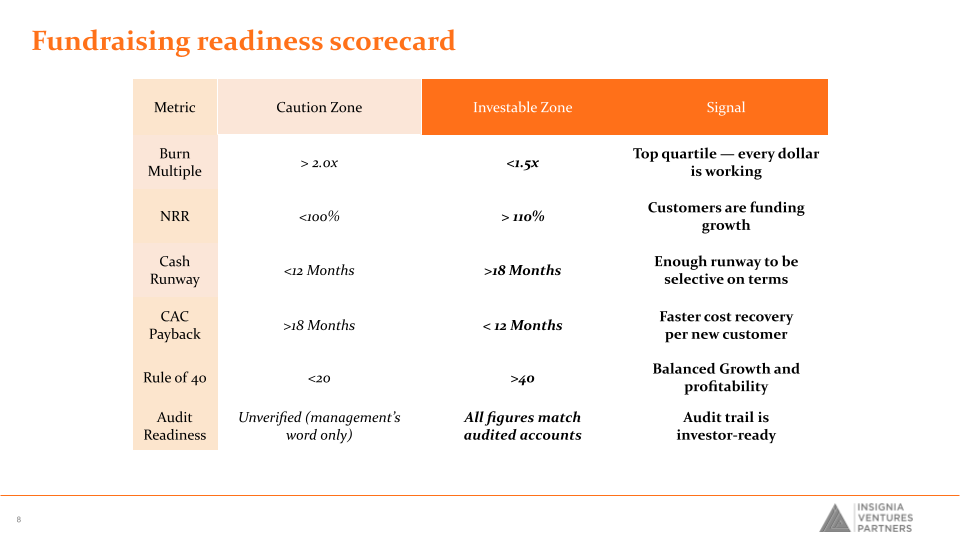

The fundraising readiness scorecard

The practical translation of the efficiency-era reset is a set of zones investors now apply, often before the first call with management. Each zone has a caution range and an investable range, and the gap between them is what determines whether a deal moves into a process at all.

Fundraising readiness scorecard

The zones investors apply before a term sheet — every line is a CFO-owned process

Two of these rows deserve specific framing because they are easy to underestimate. NRR is what tells investors whether a business has real product-market fit: above 100%, existing customers are funding growth; below 100%, the business is losing ground before acquiring new customers. Cash runway used to feel comfortable at twelve months; today the bar is higher, and investors no longer rely on management accounts — they verify the figure against audited statements.

The audit readiness row matters most for founders. The other rows are operational; this one is structural. A growth-stage company that cannot reconcile its management figures to audited accounts has effectively chosen to delay every future round, because every future round will need to underwrite that gap before pricing the equity. In the post-2025 environment, that gap has stopped being financed.

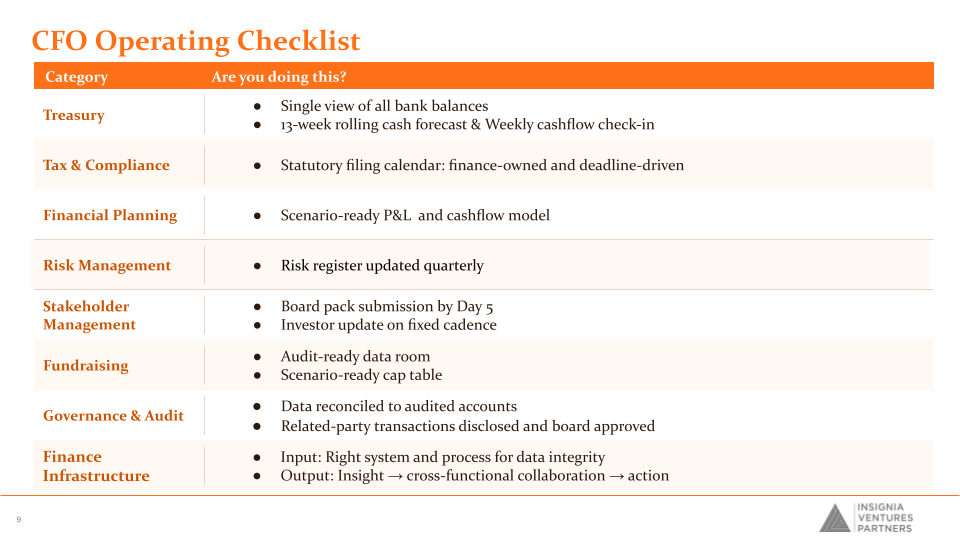

The CFO operating discipline

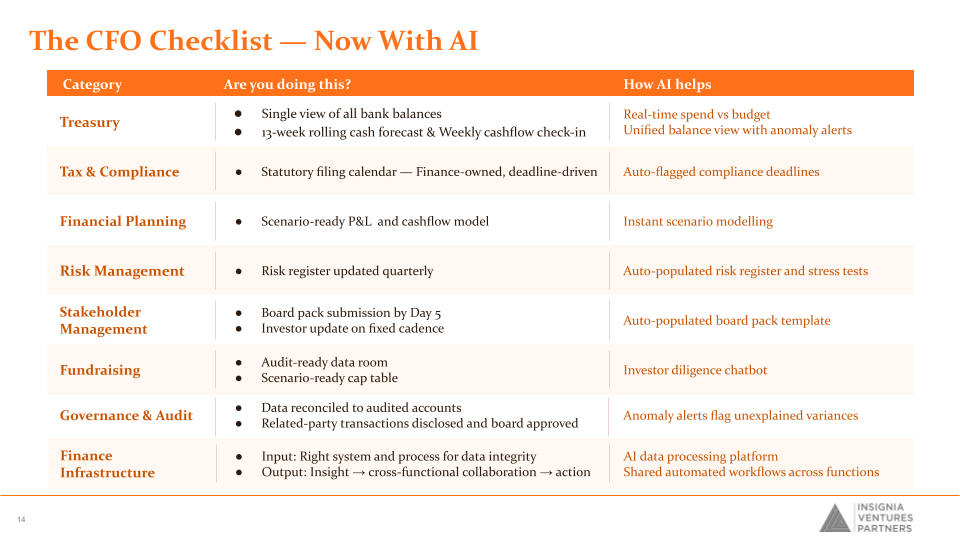

The scorecard tells a CFO what investors will measure. The operating discipline is what produces those numbers without heroics in the weeks before a fundraise. The minimum viable list, drawn from the practices that recur across CFOs in efficient companies, sits across eight categories:

- Treasury. Cash is always the first thing to check. A signed term sheet is promising, but it is not cash yet. A single, real-time view of bank balances across all entities and currencies; a thirteen-week rolling cash forecast updated weekly, not monthly; a real-time read on spend versus budget; and a regular check-in with the founders so the finance and operating sides of the house stay on the same page.

- Tax and compliance. A statutory filing calendar the finance function owns and runs against, with deadlines that do not slip into legal or operations.

- Financial planning. A scenario-ready P&L and cashflow model that can answer a board question — “what happens to our burn multiple if we slow Singapore hiring by a quarter and accelerate Vietnam by one?” — within an hour, not a week.

- Risk management. A quarterly-updated risk register, owned by the CFO, with clear thresholds for board escalation.

- Stakeholder management. A board pack delivered by Day 5 of each month, and an investor update on a fixed cadence rather than only when there is good news.

- Fundraising. An audit-ready data room kept warm year-round, and a scenario-ready cap table that can model what each next round does to founder ownership and option pool depth.

- Governance and audit. The row with the highest marginal value today. Data reconciled to audited accounts is the floor; the ceiling is a related-party disclosure regime that catches every transaction, with explicit board approval before settlement, not after.

- Finance infrastructure. The right systems and processes for data integrity at the input layer, and cross-functional workflows at the output layer that turn finance data into decisions made elsewhere in the business.

The list is unglamorous on purpose. Investors who have lived through the past two years are drawn to companies whose CFOs run an unglamorous list well.

Treasury foundations: the layer below the scorecard

Behind the scorecard sits a treasury function that most growth-stage companies in the region have under-invested in. Treasury maturity is best read as a ladder — basic, intermediate, and strategic — and not every company needs to reach the top rung. Where a finance team sits on the ladder should reflect the aspiration of the business and the complexity of its cash, not a generic best-practice template.

The early-stage practices that compound into runway and resilience are a short list:

- Cash management. Define core and non-core banking relationships deliberately, and maintain a current view of both actual and forecast cash positions.

- Working capital. Set payment terms with the same intentionality used for product pricing, and track daily collections and disbursements.

- Inflation. With inflation still sticky in several of the region’s largest economies, put cash surplus into yield-bearing instruments at whatever risk band the business can tolerate, and write price-variation clauses into long-tenor contracts.

- Automation. Bank account reporting connected to a single ledger view, and a payment workflow that is digital end-to-end.

- Foreign exchange. A particular concern for any SaaS or fintech business with revenue and costs in different currencies — identify exposures explicitly and use natural hedging strategies before reaching for derivatives.

- Framework. A written treasury policy and a target operating model that decide which decisions are made centrally and which are pushed into entities.

For multi-entity, multi-country businesses — which describes most growth-stage companies in Southeast Asia — the next layer up is cash concentration. Three structures sit at the centre of the toolkit:

- Physical pooling. Funds are physically swept into a central account, giving the CFO a single liquidity view and reducing the number of operational accounts that need separate funding decisions.

- Single-currency notional pooling. Offsets debit and credit balances domestically without co-mingling funds — useful for entities that need to keep statutory separation.

- Multi-currency notional pooling. Extends the same logic across currencies, partially offsetting balances without forcing FX conversion.

The features that matter operationally are zero or target balancing, automated two-way sweeps, multi-entity and multi-currency pooling, and customised sweep frequencies for entities with different cash cycles.

Above pooling sits investable cash segmentation. Cash that a company holds is rarely a single object; it is a portfolio of tranches with different liquidity needs:

- Operating cash. Funds the next thirty days. Has to be liquid and safe at almost any yield cost.

- Reserve cash. Funds the next six months. Can carry a longer tenor and a slightly higher yield.

- Strategic cash. Held for a defined purpose — a planned acquisition, a regulatory deposit, a distribution to a parent. Can be invested against that horizon.

Treating all cash as a single pool earns the lowest yield on the largest balance and is one of the most common foregone-return decisions on a growth-stage balance sheet.

The discipline that ties all of this together is a treasury policy with explicit governance. The board approves the policy and any material changes; a treasury committee, typically chaired by the CFO and including the treasurer and senior finance executives, oversees implementation and decides on significant treasury matters; the treasury department executes daily; internal audit reviews compliance on a fixed cadence. A clear delegation of authority, set out in a treasury policy and reviewed at least annually, is the difference between a company that survives a treasurer’s departure or a banking outage and one that does not.

Non-dilutive capital as a runway tool

The same efficiency-era logic that has tightened the equity bar has opened a parallel market for non-dilutive capital that growth-stage CFOs in the region historically did not access. Innovation banking — the credit category built specifically for venture-backed and growth-stage companies — has become a meaningful supplement to equity for companies whose metrics are good enough to support debt but who do not want to mark up or down at the wrong moment in the cycle.

The use cases vary by stage:

- Working capital and burn preservation. At earlier stages, uncommitted or short-term senior facilities can optimize working capital and preserve cash burn.

- Runway extension. Committed senior facilities can extend the runway between rounds without dilution.

- Asset-backed lending. For asset-intensive businesses — fintechs running receivables books, marketplace businesses with cashflow-generative inventory — platform lending against those assets is structurally available where corporate-style lending is not.

- Cashflow / EBITDA-based credit. For more mature companies, committed facilities sized against company cashflow or EBITDA can fund acquisitions or capex on terms more attractive than equity at most points in the cycle.

- Re-capitalisation. For companies sitting on capital-structure complexity — maturing convertible notes, layered preferred stacks, awkwardly priced bridges — re-capitalisation lending can simplify the cap table ahead of a next round or an exit process.

Three recurring features of the credit available in the region in 2026 are worth knowing:

- Local-currency capacity. USD financing is not always the right answer; the local-currency capacity of regional banks lets a company avoid the asset-liability currency mismatch that has historically been a hidden cost on debt for emerging-market businesses.

- Distribution mechanics. Funded loan syndication, club structures, and unfunded distribution via non-payment insurance let banks underwrite larger tickets earlier in a company’s life by sharing risk with insurers and other financial institutions.

- Risk-transfer structures. On-balance-sheet versus risk-transfer structures matter for companies whose lenders or regulators care about leverage or capital adequacy ratios; financing assets off balance sheet through risk-transfer structures has become a real tool for fintechs in particular.

Innovation banking lenders active in the region have collectively deployed multi-billion-dollar credit books across Southeast Asia in recent years, with individual tickets typically ranging from the single-digit to high-double-digit millions of US dollars and covering companies from Series A through listed.

For a CFO, the relevant question is not whether to take on debt; it is whether the company’s metrics support debt cleanly, whether the structure preserves rather than constrains operational flexibility, and whether the resulting weighted-average cost of capital is lower than the marked or unmarked equity alternative. In a market where seed has compressed and late-stage has become more selective, the answer to those questions is increasingly yes.

AI as the capacity multiplier

The reason any of this is now operationally feasible inside a growth-stage finance team — which is rarely staffed for it — is that the unit cost of finance work has fallen. Automation, alongside liquidity and fundraising, is one of the questions most consistently on the post-Series A CFO’s mind in 2026.

Most finance leaders have lived a version of the same story. Excel has been the working surface of finance since auditor days — to the point where many CFOs will admit to dreaming about a model and opening a laptop in the middle of the night to update it. The pain point is rarely the model itself. It is the gap between the model and the moment of decision. An investor asks during a live presentation what happens if a key assumption changes. The answer is in the model. The model was not built for live presentation. The CFO promises to come back later. The “what if” was reasonable; the data was there; the tool was not. AI is the layer that closes that gap. It is not there to replace the CFO; it is there to free up time, so the answer arrives instantly rather than the day after.

The shift is concrete. Board pack preparation, which used to consume the days that should have gone into board pack interpretation, is now an exercise in AI-assisted data assembly with the analytical time spent on the narrative the numbers tell. Sensitivity models that previously required a financial-modelling specialist and a week of work can now be generated in minutes from a structured prompt — a role definition (expert SaaS CFO), a task (build sensitivity), the right inputs (MRR, cash, OpEx, scenario logic), the right outputs (Rule of 40, burn, breakeven point), and a format constraint (interactive, offline, no data risk).

Transaction-level data that used to sit in a warehouse waiting for someone to ask the right question can now be queried in natural language to surface variances, anomalies, and revisit-strategy signals before they show up as quarterly surprises. A cohort analysis on roughly 100,000 sales records — once a multi-day exercise in cleaning and pivoting — can now be converted in minutes into a customer-retention pattern colour-coded green for healthy, yellow for borderline, and orange for action. The output is not the deliverable; the decision is. The pattern can reshape sales strategy; a cash-flow signal can change the expansion plan for next quarter. Connecting the numbers to the decisions is where the CFO makes the difference.

The implication for the operating checklist is that every category gets an AI-assisted layer:

- Treasury. Unified balance view with anomaly alerts. A client payment that is slower than usual gets flagged early, before it affects the runway.

- Tax and compliance. Auto-flagged statutory deadlines.

- Financial planning. Instant scenario modelling — interactive and live, not pre-cooked.

- Risk management. Auto-populated risk register and stress tests.

- Stakeholder management. Board pack templates auto-populated; the CFO verifies, layers in interpretation, and arrives at the meeting ready for the real conversation.

- Fundraising. Investor-diligence chatbot trained on the company’s data room.

- Governance and audit. Anomaly alerts that flag unexplained variances early enough to remedy before they become disclosures.

- Finance infrastructure. Shared automated workflows across functions.

The categories on the checklist do not change. Automation reduces the workload so the CFO can focus on the business. None of this replaces the CFO’s judgment; all of it raises the ceiling on how many companies a single CFO can reasonably co-pilot.

What to do about it

The 2026 fundraising bar is not the 2021 bar with a higher denominator. It is a different bar — efficiency-led, governance-anchored, and audit-tested — and the operator who clears it is, in most companies that have raised in the past twelve months, the CFO. The work is to translate that bar into the eight operating categories above, to build the treasury function that supports the metrics rather than constrains them, to underwrite the company’s own capital plan with both equity and non-dilutive options, and to use AI where it raises capacity rather than as a substitute for judgment.

The CFO mandate has expanded. The core finance functions still matter, but the job now goes beyond the numbers; the CFO is the founder’s co-pilot, connecting the financial picture to every business unit. A strong CFO turns a good company into a great one — and is, increasingly, the operator who decides whether the company is investable when an investor finally calls.

References

- DealStreetAsia. *Southeast Asia Startup Funding Report: Full Year 2025*. Published 4 February 2026. https://www.dealstreetasia.com/reports/southeast-asia-startup-funding-report-2025

- Silicon Valley Bank. *State of the VC-Backed CFO 2025*. Published April 2025. https://www.svb.com/trends-insights/reports/state-of-the-vc-backed-cfo-2025/

- KPMG. *Venture Pulse Q4 2025: Global analysis of venture funding*. Published 21 January 2026. https://kpmg.com/us/en/articles/2026/venture-pulse-q4-2025.html

- Asia News Network. “Indonesia’s start-up scandals in 2025 force investors to raise the bar, change playbooks.” Published 14 August 2025. https://asianews.network/indonesias-start-up-scandals-in-2025-force-investors-to-raise-the-bar-change-playbooks/

- Google, Temasek and Bain & Company. *e-Conomy SEA 2025*. Published 4 November 2025. https://services.google.com/fh/files/misc/e_conomy_sea_2025_report.pdf

Paulo Joquiño is a writer and content producer for tech companies, and co-author of the book Navigating ASEANnovation. He is currently Editor of Insignia Business Review, the official publication of Insignia Ventures Partners, and senior content strategist for the venture capital firm, where he started right after graduation. As a university student, he took up multiple work opportunities in content and marketing for startups in Asia. These included interning as an associate at G3 Partners, a Seoul-based marketing agency for tech startups, running tech community engagements at coworking space and business community, ASPACE Philippines, and interning at workspace marketplace FlySpaces. He graduated with a BS Management Engineering at Ateneo de Manila University in 2019.